A Look at Trends in Parks & Recreation

The outlook among parks respondents has gotten increasingly more positive over the past several years, and 2016 is no exception. Revenues are stabilizing or increasing for the vast majority, the percentage planning new construction is growing, and people are using park-run facilities in growing numbers.

Local and regional park agencies have a tremendous economic impact. The National Recreation and Park Association's study in "The Economic Impact of Local Parks" quantifies that impact, stating that park agencies generated nearly $140 billion in economic activity and supported almost 1 million jobs in 2013 through operations and capital spending. And, of course, parks not only contribute to the economic well-being of their communities and the country, they also provide a host of other benefits: raising property values, improving quality of life and health, environmental conservation.

In this section, we'll take a look at the trends in parks and recreation. Respondents from this type of organization made up 41.9 percent of the survey population.

As is the case with the general survey population, the largest percentage of parks respondents (28.9 percent) were from the Midwest. Around a quarter (25.4 percent) were from the West. The South Atlantic was home to 17.7 percent of these respondents, while 16.7 percent were from the Northeast. The smallest number of U.S. parks respondents were from the South Central region, home to 10.9 percent. Just 0.3 percent were located outside of the United States.

Nearly half (49.8 percent) of parks respondents were from suburban communities, making them more likely than non-parks respondents to be from the suburbs. Just 41.9 percent of non-parks respondents were from suburban communities. Parks respondents were also slightly more likely than non-parks respondents to be from urban areas, with 21.6 percent of parks respondents reporting from urban communities, compared with 20.7 percent of non-parks respondents. In contrast, less than three in 10 (28.6 percent) parks respondents were from rural communities, compared with 37.3 percent of non-parks respondents.

Parks respondents served a larger population than any other type of respondent, reporting an average of 105,300. Parks respondents were almost twice as likely as non-park respondents to serve populations of 100,000 or more, with 24 percent of parks reporting a population of at least 100,000, while just 12.4 percent of non-parks respondents served a population of this size. Conversely, just 31.1 percent of parks respondents said they serve a population of less than 20,000, compared with 57.9 percent of non-parks respondents.

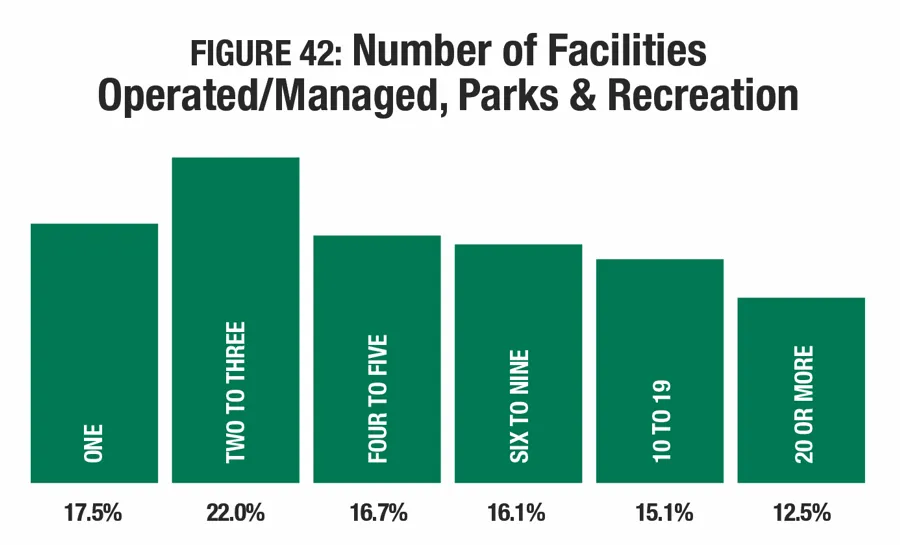

On average, parks respondents said they manage 10.3 facilities, a number that has been very steady over time. More than a quarter (27.6 percent) of parks respondents said they manage 10 or more facilities. (See Figure 42.) This compares with just 10 percent of non-parks respondents. Conversely, parks respondents were far less likely than others to manage just a single facility. Some 17.5 percent of parks respondents said they manage just one facility, compared with 49.3 percent of non-parks respondents.

Parks respondents were much more likely than non-parks respondents to serve an all-ages audience or an audience of children ages 4 to 12. While 55.7 percent of parks respondents said they primarily serve all ages, just 30.7 percent of non-parks respondents serve an all-ages audience. And, while 26.1 percent of parks respondents said their primary audience is made up of children between 4 and 12 years old, just 12.8 percent of non-parks respondents serve 4-to-12-year-olds as their primary audience.

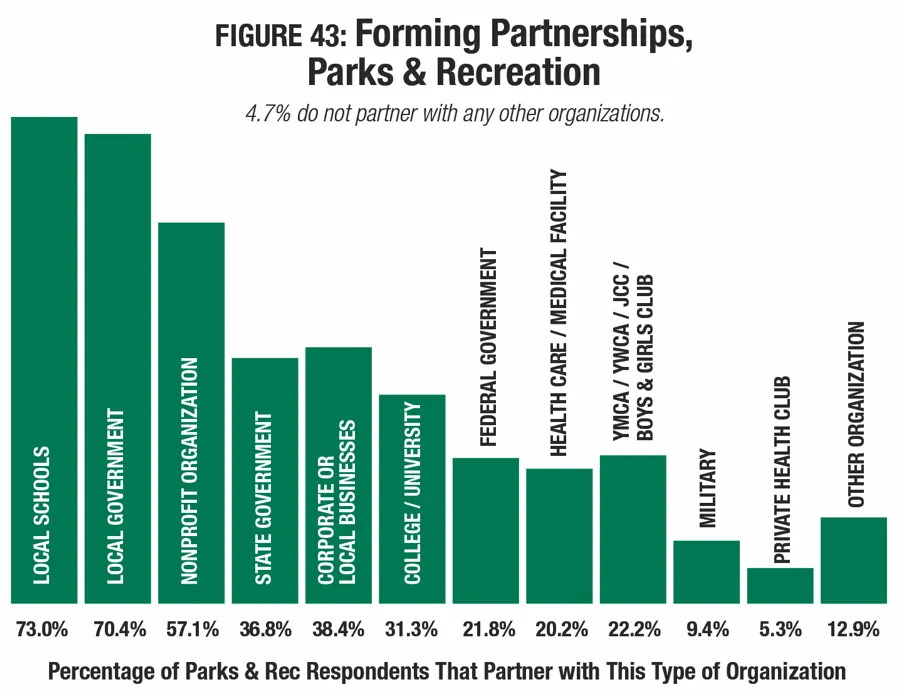

The vast majority of parks respondents (95.3 percent) said that they formed partnerships with outside organizations. This compares with 81.4 percent of non-parks respondents. The most common partners for parks were local schools (73 percent of parks respondents partner with them); local government (70.4 percent); nonprofit organizations (57.1 percent); corporate or local businesses (38.4 percent); and state government (36.8 percent). (See figure 43.)

Revenues & Expenditures

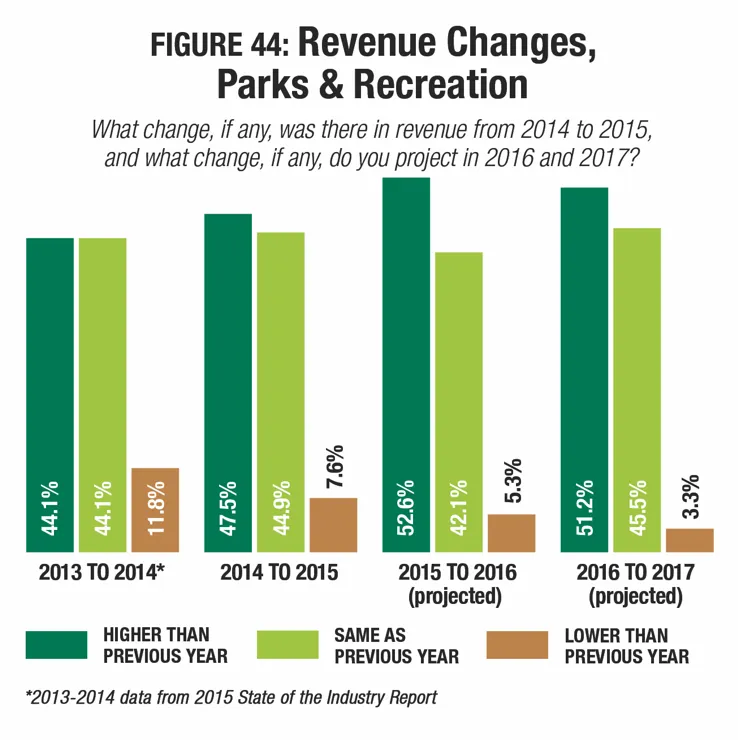

Revenues for parks respondents continue to grow more stable over time, with an increasing percentage reporting that their revenues are either increasing or remaining the same year over year. From 2013 to 2014, 44.1 percent of respondents said their revenues had increased, while 11.8 percent reported a decrease. From 2014 to 2015, the percentage reporting a decrease fell to 7.6 percent, while those reporting an increase rose to 47.5 percent. (See Figure 44.)

Looking forward, more than half of parks respondents are expecting revenues to increase in both 2016 (52.6 percent) and 2017 (51.2 percent). At the same time, the number expecting revenues to fall, drops to 5.3 percent in 2016 and 3.3 percent in 2017.

Parks respondents reported a slightly greater drop in their operating expenses from 2014 to 2015 than the average for all respondents. While the average operating expenditure for all respondents fell 2.6 percent in that time period, parks respondents reported a 3.9 percent decrease from $1,980,000 in 2014 to $1,903,000 in 2015.

However, looking forward, parks respondents projected a greater increase in their operating budgets from 2015 to 2017 than the average for all respondents. While the average operating expenditure for all respondents is projected to rise 5.8 percent from 2015 to 2017, parks respondents projected an 8 percent increase, to an average of $2,056,000 in fiscal 2017.

On average, parks respondents report that they recover 45.1 percent of their operating costs via revenue. This compares with 49.6 percent of operating costs recovered via revenue for all respondents. About one-third (33 percent) of parks respondents reported that they recover 30 percent or less of their operating costs via revenue. Another 21.1 percent said they earn back 31 to 50 percent of operating costs via revenue. Some 16.4 percent said they earned 51 to 70 percent of their costs via revenue, and 19.9 percent earned between 71 percent and 100 percent of their operating costs.

Respondents from parks were among the most likely to report that they had taken actions to reduce their expenditures. Some 86.3 percent of parks respondents had done so, compared with 81.5 percent of non-parks respondents. The most common actions parks respondents had taken to reduce their operating costs were: increasing energy efficiency (53.7 percent of parks respondents had done so); increasing fees (52.8 percent); putting construction or renovation plans on hold (33.8 percent); reduced staffing levels (29.4 percent); and reduced hours of operation (21.5 percent).

A Splashin' Good Time

Splash play has been at or near the top of the list of the most commonly planned features at parks respondents' facilities for many years running. This year, the percentage of parks respondents who are planning to add splash play increased slightly, from 27.6 percent in 2015 to 31.1 percent in 2016.

Manufacturers of splash play products continue to innovate, studying the use of their existing products installed in the field to help develop their understanding of how people love to play and interact in water, in addition to finding ways to make splash play even more environmentally friendly.

Park Facilities

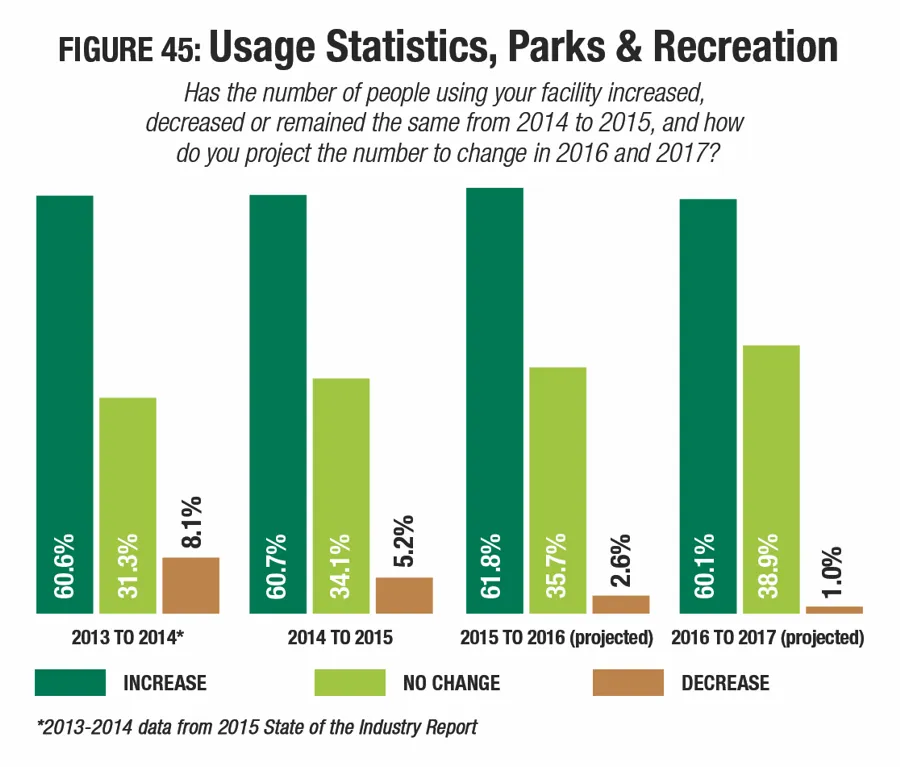

The number of parks respondents who reported an increase in usage at their facilities remained steady from 2014 to 2015. In last year's report, 60.6 percent of parks respondents said the number of people using their facilities had increased from 2013 to 2014. This year, 60.7 percent of parks respondents said usage at their facilities had increased from 2014 to 2015. At the same time, the number of parks respondents who reported decreases in usage fell from 8.1 percent reporting a decrease from 2013 to 2014, to 5.2 percent reporting a decrease from 2014 to 2015. (See Figure 45.)

Looking forward, the number of parks respondents who expect to see further increases in the number of people using their facilities holds fairly steady, with 61.8 percent projecting an increase in 2016, and 60.1 percent expecting an increase in 2017. At the same time, the number expecting a decrease drops to 2.6 percent projecting a decrease in 2016 and 1 percent projecting a decrease in 2017.

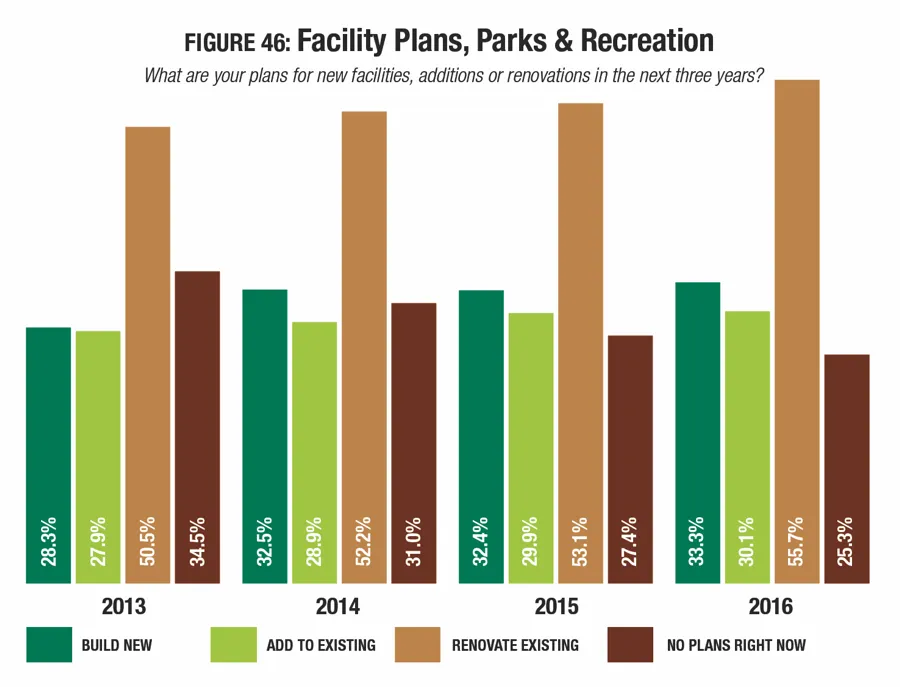

The number of parks respondents who have plans for construction over the next three years has been increasing steadily since 2012, when 64.8 percent had such plans. In 2016, 74.7 percent of parks respondents had plans for construction, up from 72.6 percent last year. One-third (33.3 percent) are planning to build new facilities, while another three in 10 (30.1 percent) said they plan to make additions to their existing facilities. More than half (55.7 percent) said they have plans to make renovations to their existing facilities in the next three years. (See Figure 46.)

Parks respondents were much more likely to be planning construction than non-parks respondents. While 74.7 percent of parks respondents in 2016 have construction plans, 60.5 percent of non-parks respondents had such plans.

While the average budget for construction for all respondents fell by 12.5 percent from 2015 to 2016, parks respondents reported a much smaller decrease to their budget for construction, with a 1 percent drop from $3,880,000 in 2015 to $3,842,000 in 2016. Parks respondents plan to spend 9.2 percent more than the average for all respondents.

There was no change to the features most commonly found at park respondents' facilities from 2015 to 2016. The 10 most common features include: playgrounds; park shelters such as gazebos and picnic shelters; park restroom structures; walking and hiking trails; open spaces such as gardens and natural areas; outdoor courts for sports like basketball and tennis; bleachers and seating; natural turf sports fields; concessions; and classrooms and meeting rooms.

Parks respondents are much more likely than non-parks respondents to report that they have plans to add features at their facilities over the next three years. More than half (53.8 percent) of parks respondents said they have plans to add features, whereas 34.8 percent of non-parks respondents have such plans.

The most commonly planned additions for parks respondents include:

- Splash play areas (planned by 31.1 percent of parks respondents who will be adding features)

- Fitness trails or outdoor fitness equipment (20.8 percent)

- Playgrounds (20.4 percent)

- Park structures (19.5 percent)

- Dog parks (18.3 percent)

- Hiking and walking trails (16.8 percent)

- Bike trails (15.8 percent)

- Park restroom structures (15.3 percent)

- Synthetic turf sports fields (13.7 percent)

- Wi-Fi services (12.8 percent)

Features that were planned by more respondents in 2016 than in 2015 include: splash play areas (up from 27.6 percent); and park structures (up from 17.7 percent).

In the Garden

This is the first year that the survey included community gardens as a choice among features included in respondents' facilities. Parks respondents were the most likely to have community gardens, with 32.9 percent reporting that their facilities currently include community gardens.

Community gardens were also one of the more commonly planned additions for parks respondents, with 12.4 percent reporting they had plans to add community gardens over the next three years.

Programming

Parks respondents were more likely than non-parks respondents to report that they offered programming at their facilities. While 97.6 percent of parks respondents provide programs, 95 percent of non-parks respondents do so.

The most common programs found in parks and recreation respondents' lineup include: holiday events and other special events (80.5 percent); youth sports teams (69.3 percent); day camps and summer camps (66.3 percent); adult sports teams (60.7 percent); educational programs (60.4 percent); arts and crafts (60 percent); active older adult programming (58 percent); fitness programs (55.4 percent); swimming programs (53.2 percent); and mind-body balance programs like yoga (53.1 percent).

There were increases in the number of parks respondents providing holidays and special events, youth sports teams, active older adult programs, and fitness programs. Swimming and mind-body balance did not appear in the top 10 programs for parks respondents in 2015. They replaced sports tournaments and races, and sport-specific training.

Parks respondents were far more likely than non-parks respondents to report that they had plans to add programs at their facilities over the next three years. Some 38.2 percent of parks respondents said they had such plans, compared with 25.8 percent of non-parks respondents.

The most commonly planned programs in 2016 include:

- Teen programming (up from No. 6 in 2015)

- Educational programs (up from No. 4)

- Environmental education programs (down from No. 1)

- Fitness programs (down from No. 3)

- Arts and crafts (did not appear in top 10 for 2015)

- Programs for active older adults (down from No. 5)

- Mind-body balance programs such as yoga and tai chi (down from No. 2)

- Holidays and other special events (down from No. 7)

- Special needs programs (did not appear in 2015)

- Performing arts (did not appear in 2015)