A Look at Trends in Colleges & Universities

Over the past decade, there has been much discussion over the runaway costs of attending college. What many don't realize, though, is that some of that rapidly rising cost is due to the fact that states dramatically cut their financial support for public colleges at the onset of the recession, and very few have restored funding. In fact, according to the Center on Budget and Policy Priorities, 46 states were still spending less per student in the 2015-16 school year than they did before the recession. The average state is spending 18 percent less per student than before the recession. Colleges and universities have been forced to adapt to these changes in financial support, increasing tuition, cutting faculty, reducing course offerings and eliminating some services.

This state of affairs continues to be reflected in the results of the Industry Report survey, where college and university respondents, who made up 11.2 percent of survey respondents in 2017, continue to struggle with revenue vs. costs.

As usual, the largest number of college respondents, 29 percent, were located in the Midwest. The next largest group, at 20.1 percent, were from the South Atlantic region. They were followed by the Northeast and South Central states—each region was home to 19.6 percent of college and university respondents. The smallest number of college respondents were found in the West, with 10.3 percent. Another 1.4 percent of college respondents were located outside of the United States.

The largest percentage of college respondents in 2017 were from urban communities. Some 37.6 percent of college respondents said they were from urban areas. The remainder of college respondents were split fairly evenly among rural and suburban communities. Some 31.9 percent of college respondents were located in the suburbs, while 30.5 percent were found in rural communities.

On average, college respondents said they serve a population of 35,700 people, up from 33,100 in 2016. College respondents were much more likely to report that they had a population of 20,000 or less than non-college respondents. Nearly three-quarters (72.1 percent) of college respondents said their population was 20,000 or less, compared to 43.9 percent of non-college respondents. Conversely, just 6 percent of college respondents said they reached an audience of 100,000 or more, while 24.3 percent of non-college respondents served a population of at least 100,000.

A majority of college respondents said they were from public colleges and universities. Some 64.4 percent of these respondents said they were with public organizations. Another 31.5 percent were with private nonprofits, while 4.2 percent said they were with private, for-profit organizations.

Respondents from colleges and universities managed an average of 4.9 facilities. They were more likely than non-college respondents to report that they managed between one and three facilities. Seven out of 10 (70 percent) college respondents said they manage between one and three facilities, compared with 58 percent of non-college respondents. Likewise, while 19.3 percent of non-college respondents said they manage 10 or more facilities, only 8.9 percent of college respondents said they manage 10 or more.

College respondents were much less likely than non-college respondents to report that they had formed partnerships with other organizations, though a majority had done so. Some 79.6 percent of college respondents said they had partnered with other organizations, compared with 87.8 percent of non-college respondents. The most common partnerships for college respondents were formed with other colleges and universities. In fact, 57.8 percent of college respondents said they had partnered with other colleges and universities, compared with 31.6 percent of non-college respondents. The other most common partners for college respondents include: local schools (38.4 percent of college respondents had partnered with them), state government (28.9 percent), local government (26.5 percent) and nonprofit organizations (25.6 percent).

Revenues & Expenditures

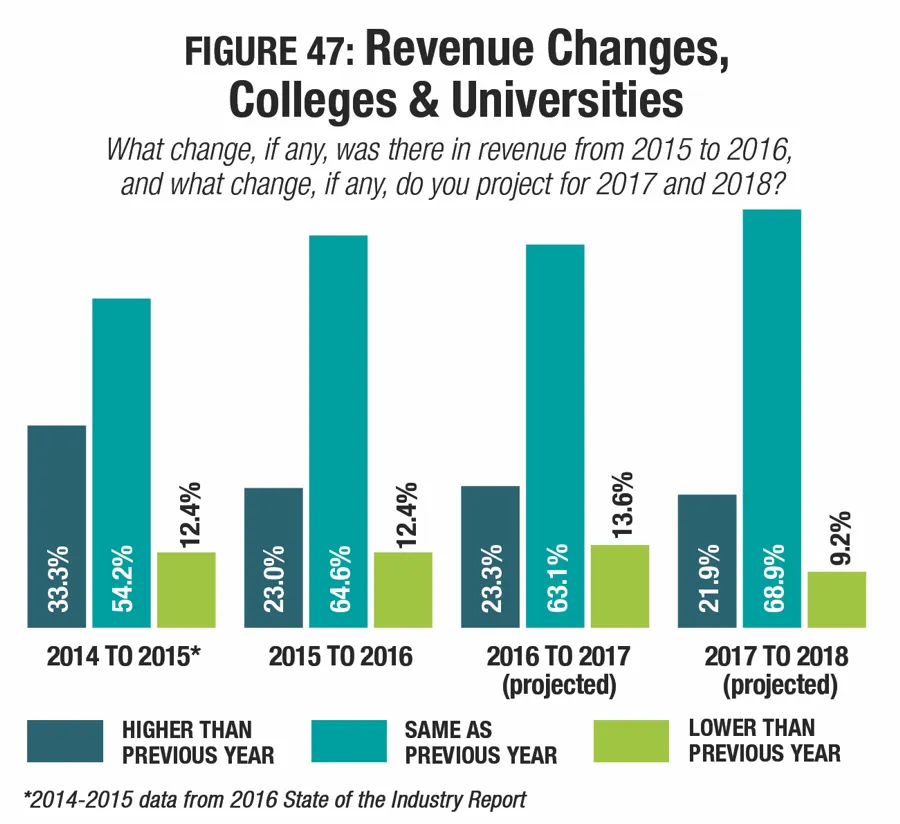

As mentioned previously, college and university respondents continue to struggle financially. While most respondents are increasingly likely to report that their revenues are growing year-over-year, the percentage of college respondents reporting increasing revenues has fallen significantly. While one-third (33.3 percent) of college respondents said revenues grew from 2014 to 2015, only 23 percent said revenues had increased from 2015 to 2016. Another 12.4 percent said revenues had fallen. (See Figure 47.)

Looking forward, the percentage of college respondents who expect revenues to increase holds fairly steady, with 23.3 percent expecting revenues to grow in 2017 and 21.9 percent expecting growth in 2018. At the same time, the number expecting revenues to decrease grows to 13.6 percent for 2017 before falling to 9.2 percent for 2018.

After reporting decreases to operating expenses for 2014 and 2015, college respondents saw a slight increase in operating expenditures this year. College respondents' average operating cost grew 6.4 percent from 2015 to 2016, from $1,790,000 to $1,905,000. This growth rate was much slower than the average growth reported for all respondents between 2015 and 2016, of 17.5 percent.

Looking forward, college respondents are expecting their operating costs to grow at about double the rate of the general survey population. While all respondents projected a 3.5 percent growth in operating costs between 2016 and 2018, college respondents projected that their average operating expenditure would grow 7.1 percent, to $2,040,000 in 2018.

On average, college respondents report that they recover 33.5 percent of their operating costs via revenue, down slightly from last year, when 35.5 percent of costs were recovered. More than half (50.2 percent) of college respondents said that they recover 30 percent or less of their operating costs via revenue. Another 6.8 percent recover between 31 percent and 50 percent of their operating costs. Some 7.8 percent said they earn back between 51 percent and 70 percent of their operating costs. And 14.6 percent of college respondents said they recover 71 percent or more of their operating costs via revenues.

College respondents were slightly less likely to report that they had taken action to reduce their operating expenditures, though a majority said they had done so. Some 80.5 percent of college respondents had taken such action, while 83.7 percent of non-college respondents had done so. The most common actions taken by college respondents include: improving energy efficiency (43.8 percent of college respondents had done so), reducing staff (36.7 percent), putting construction and renovation plans on hold (31 percent), increasing fees (27.6 percent) and reducing hours of operation (27.6 percent).

College respondents were more likely than their counterparts from other types of facilities to report that they had cut staff, cut programs or services, or reduced their hours in order to lower their operating costs. While 30.6 percent of non-college respondents said they had cut staff, 36.7 percent of college respondents had done so. More than one-quarter (25.7 percent) of college respondents said they had made program and service cuts, compared with 17.8 percent of non-college respondents. And while 27.6 percent of college respondents said they had reduced their hours of operation, only 15.3 percent of non-college respondents had done so.

College Facilities

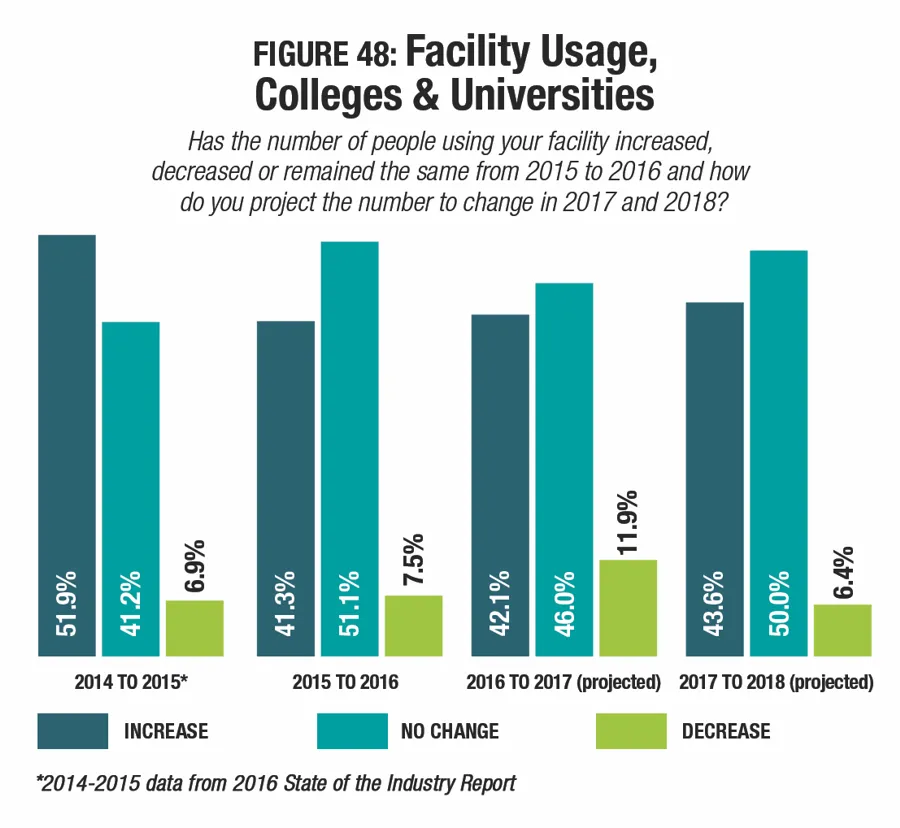

The percentage of college respondents reporting an increase in the number of people using their facilities fell from 2015 to 2016, with 51.9 percent reporting an increase and 41.3 percent reporting an increase in 2016. At the same time, the percentage of college respondents who saw usage drop grew from 6.9 percent to 7.5 percent. (See Figure 48.)

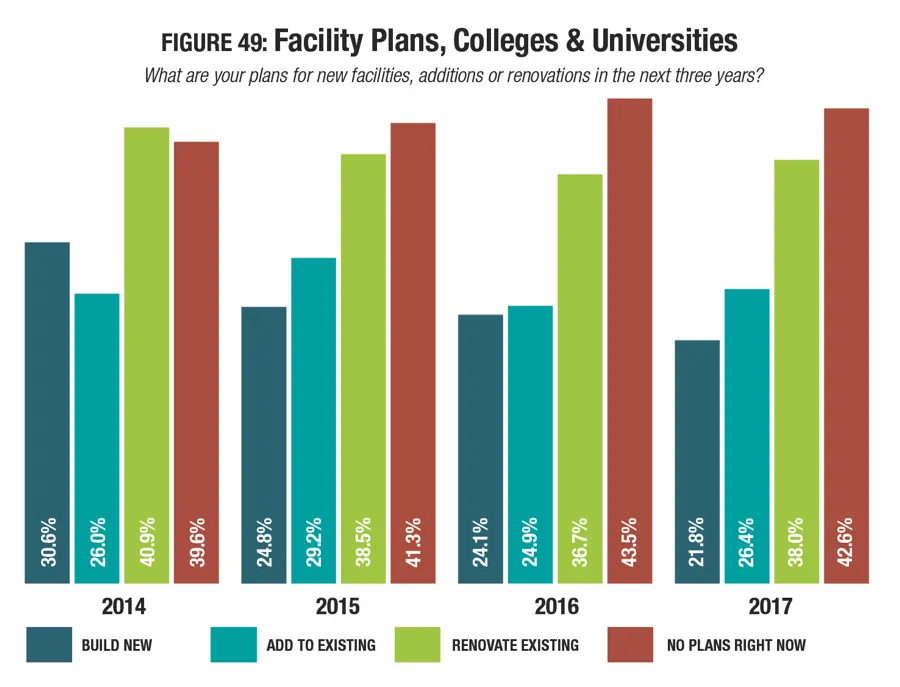

While construction plans are being made by an increasing number of respondents from most types of facilities, college respondents have seen those numbers remain fairly steady over the past five years. In fact, while 59.2 percent of college respondents in 2013 said they had plans for construction, in 2017, that number fell to 57.4 percent. This compares with 69.9 percent of non-college respondents who have construction plans.

Slightly fewer college respondents in 2017 said they are planning new construction compared with 2016. Some 21.8 percent of college respondents in 2017 said they would be building new facilities. Another 26.4 percent reported that they plan to make additions to their existing facilities, and 38 percent are planning renovations. (See Figure 49.)

Though they are less likely than others to be planning construction, college respondents remain the biggest spenders when it comes to construction plans. College respondents with construction plans reported that they would spend, on average, 81.1 percent more than the average for all respondents--$7,786,000 vs. $4,299,000. In addition, college respondents' construction budgets grew more quickly than the average for all respondents between 2016 and 2017. While for all respondents, construction budgets grew 22.2 percent in that time frame, college respondents' construction budgets grew 29 percent, from $6,037,000 in 2016 to $7,786,000.

There was very little change in the past year in the various features most commonly found among college respondents' facilities. The 10 features that are currently most common include: fitness centers, indoor courts for sports like basketball and volleyball, locker rooms, exercise studio rooms, bleachers and seating, classrooms and meeting rooms, Wi-Fi services, outdoor courts for sports like basketball and tennis, natural turf sports fields and indoor tracks.

College respondents were less likely than non-college respondents to report that they had plans to add features at their facilities over the next three years. While 42.8 percent of non-college respondents had such plans, just 32.4 percent of college respondents said they would be adding features. This is down from 2016, when 36.3 percent of college respondents were planning to add features.

The most commonly planned features for college respondents in 2017 include:

- Synthetic turf sports fields (planned by 28.6 percent of those who intend to add features at their facilities)

- Locker rooms (22.9 percent)

- Climbing walls (22.9 percent)

- Fitness trails and outdoor fitness equipment (21.4 percent)

- Fitness centers (18.6 percent)

- Bleachers and seating (17.1 percent)

- Classrooms and meeting rooms (17.1 percent)

- Exercise studios (14.3 percent)

- Disc golf courses (11.4 percent)

- Park restroom structures (11.4 percent)

Synthetic turf sports fields continue to hold the top position, though the percentage of college respondents who plan to add them fell from 33.7 percent in 2016.

There were increases in the percentage of college respondents planning to add: locker rooms (up from 22.1 percent), and fitness trails and outdoor fitness equipment (up 16.3 percent). Commonly planned features in 2017 that did not appear on this list last year include climbing walls, classrooms and meeting rooms, disc golf courses, and park restroom structures. They replace outdoor courts, Wi-Fi services, concessions and indoor tracks.

Turf Choices

Synthetic turf sports fields has been the most commonly planned feature addition at colleges and universities since 2011. Schools and school districts also commonly plan to add synthetic turf.

In 2016, 28.6 percent of college respondents said they have plans to add synthetic turf, down slightly from 2016, when 33.7 percent had such plans.

Among school respondents, 34 percent of those with plans to make additions at their facilities said they would be adding synthetic turf sports fields, representing almost no change from 2016, when 33.9 percent of school respondents said they had such plans.

Programming

Some 96.2 percent of college respondents said they provide programming of some kind at their facilities. This compares with 97.1 percent of non-college respondents. Fitness programs continue to be the most commonly offered program among college respondents. Some 83 percent of college respondents said they provide fitness programs, down slightly from 83.5 percent in 2016.

Other programs commonly provided by college respondents include: mind-body balance programs such as yoga and tai chi (67.5 percent), educational programs (57.5 percent), personal training (54.2 percent), adult sports teams (53.8 percent), sport tournaments and races (52.8 percent), individual sports activities such as running clubs or swim clubs (46.2 percent), day camps and summer camps (42.9 percent), swimming programs (42.9 percent), and aquatic exercise programs (36.8 percent).

Program offerings that were provided by more college respondents in 2017 than in 2016 include: mind-body balance programs (up from 66.2 percent), personal training (up from 52.7 percent), sports tournaments and races (up from 51.9 percent), and day camps and summer camps (up from 41.8 percent).

College respondents were less likely than non-college respondents to report that they had plans to add programs at their facilities. While 33.1 percent of non-college respondents had such plans, just 25.9 percent of college respondents were planning to add programs. This is a slight increase from 2016, when 24.9 percent had such plans.

The top 10 planned programs for college and university respondents include:

- Mind-body balance programs such as yoga and tai chi (up from No. 2)

- Day camps and summer camps (up from No. 9)

- Sport tournaments and races (up from No. 7)

- Fitness programs (down from No. 1)

- Personal training (down from No. 4)

- Nutrition and diet counseling (did not appear in 2016)

- Programs for active older adults (did not appear in 2016)

- Aquatic exercise programs (down from No. 5)

- Individual sports activities (up from No. 10)

- Sport training (did not appear in 2016)

New to the list in 2016 are nutrition and diet counseling, programs for active older adults, and sport training. These programs replace swimming programs, educational programs, and adult sports teams.