The 2021 Aquatic Trends Report

- General Facility Information

- Budget Issues

- Water & Resource Management

- Outfitting Aquatics

- Programming

- Safe in the Water

- Tracking Usage of the MAHC

- Industry-Wide Challenges

- The Pandemic Effect

It is safe to assume that not a single stakeholder in the aquatics industry—from pool owners and operators to lifeguards and other staff members to the public who eagerly show up to learn to swim, exercise and just generally enjoy the water—avoided feeling some impact from the ongoing closures and changes to business caused by the COVID-19 pandemic. Facilities across the country were forced to close for at least some period of time, and the patchwork of reopenings based on different guidelines in every state means some facilities were able to open and get business rolling again, though often at reduced capacity, while others remain closed, waiting for a go-ahead and hoping for calmer waters in 2021.

The aquatic industry is never without its challenges, from relatively high operating costs to ongoing staffing concerns, equipment and facility maintenance issues and beyond. But the coronavirus pandemic delivered a perfect storm that affected every area of operations.

Welcome to our annual Aquatic Trends Report. In these pages, we hope to provide a big-picture view of the broad issues and trends that affect aquatic facilities every year, while also digging into some of the specific effects of social distancing measures, government-required closures and more.

Survey Methodology

||||||||||||||||||||||||||||||||||||||||||||||||||||||||

This report is based on a survey conducted for Recreation Management by Signet Research Inc., an independent research company. An e-mail was broadcast and respondents were invited to participate. From the launch of the survey on Oct. 13, 2020, to the closing of the survey on Nov. 2, 2020, 646 completed surveys were received from respondents with aquatic facilities (out of 890 total returns). The findings of this survey may be accepted as accurate, at a 95% confidence level, within a sampling tolerance of approximately +/- 3.9 percent.

To begin, let's get a quick overview of our 646 respondents whose facilities include aquatic elements—from hot tubs, splash play and swimming pools to full-blown aquatic parks and waterparks.

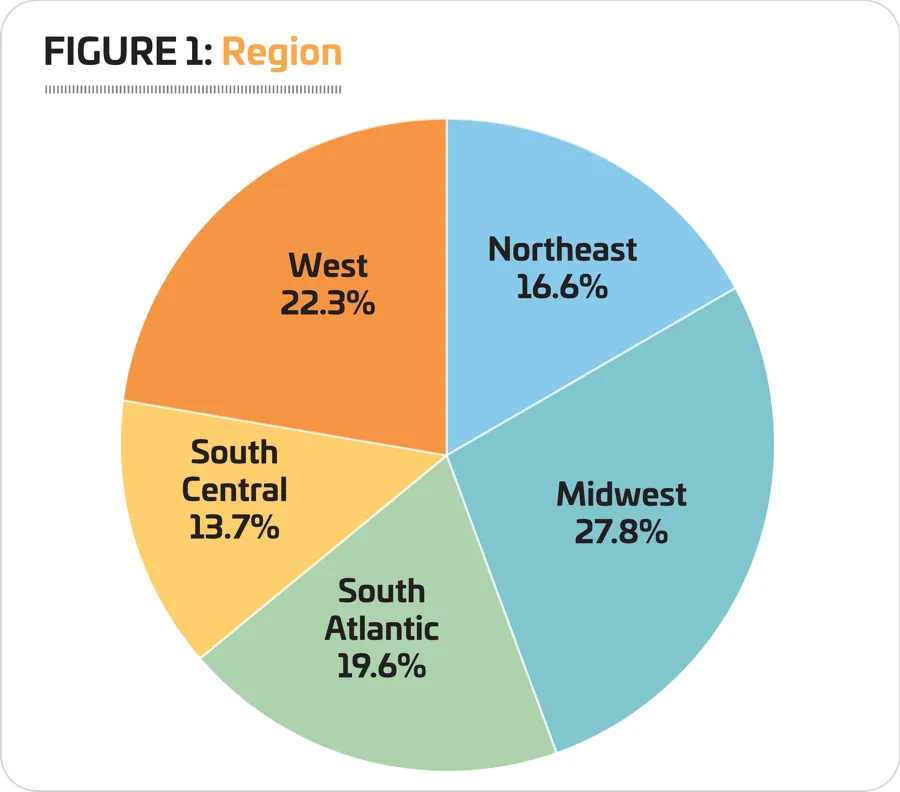

Respondents to the survey were widely dispersed across the United States, with the largest number located in the Midwest. Some 27.8% of respondents said they were from Illinois, Indiana, Iowa, Kansas, Michigan, Minnesota, Missouri, Nebraska, North Dakota, Ohio, South Dakota or Wisconsin. (See Figure 1.)

The next largest region was the West, with 22.3%. This includes Alaska, Arizona, California, Colorado, Hawaii, Idaho, Montana, Nevada, New Mexico, Oregon, Utah, Washington and Wyoming.

The South Atlantic region was home to 19.6% of survey respondents. This includes Delaware, Florida, Georgia, Maryland, North Carolina, South Carolina, Virginia, Washington, D.C., and West Virginia.

Some 16.6% of survey respondents said they were from the Northeastern states. This includes Connecticut, Maine, Massachusetts, New Hampshire, New Jersey, New York, Pennsylvania, Rhode Island and Vermont.

The South Central region was represented by 13.7% of respondents. This region includes Alabama, Arkansas, Kentucky, Louisiana, Mississippi, Oklahoma, Tennessee and Texas.

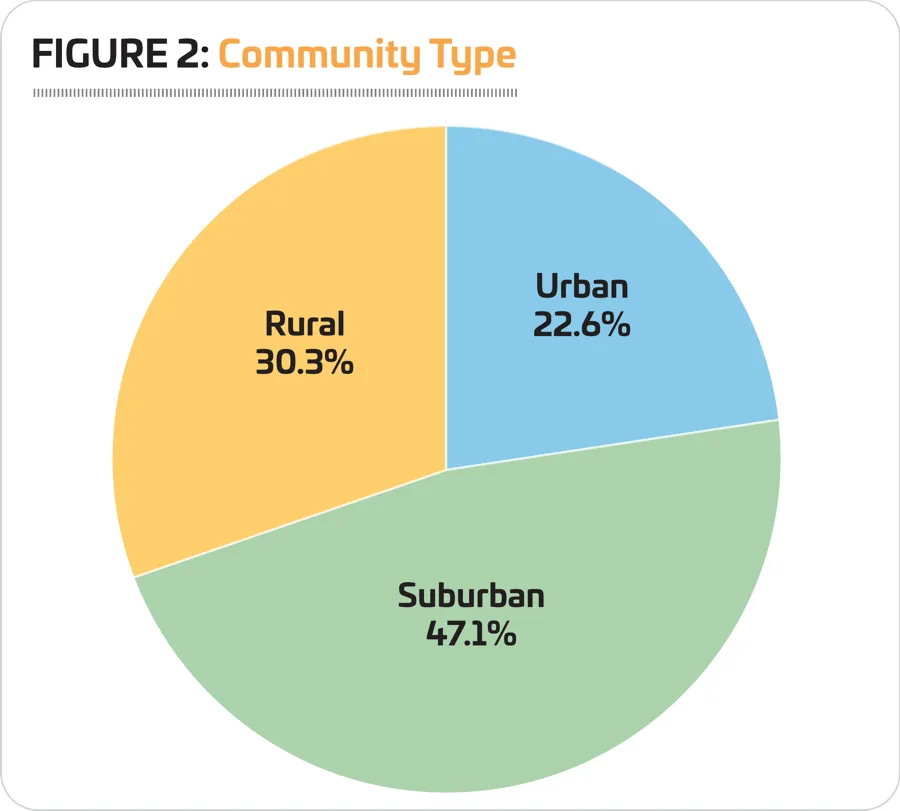

We also asked respondents to indicate the type of community they serve. Nearly half (47.1%) said they represented suburban communities. Smaller numbers were from rural areas (30.3%) and urban communities (22.6%). (See Figure 2.)

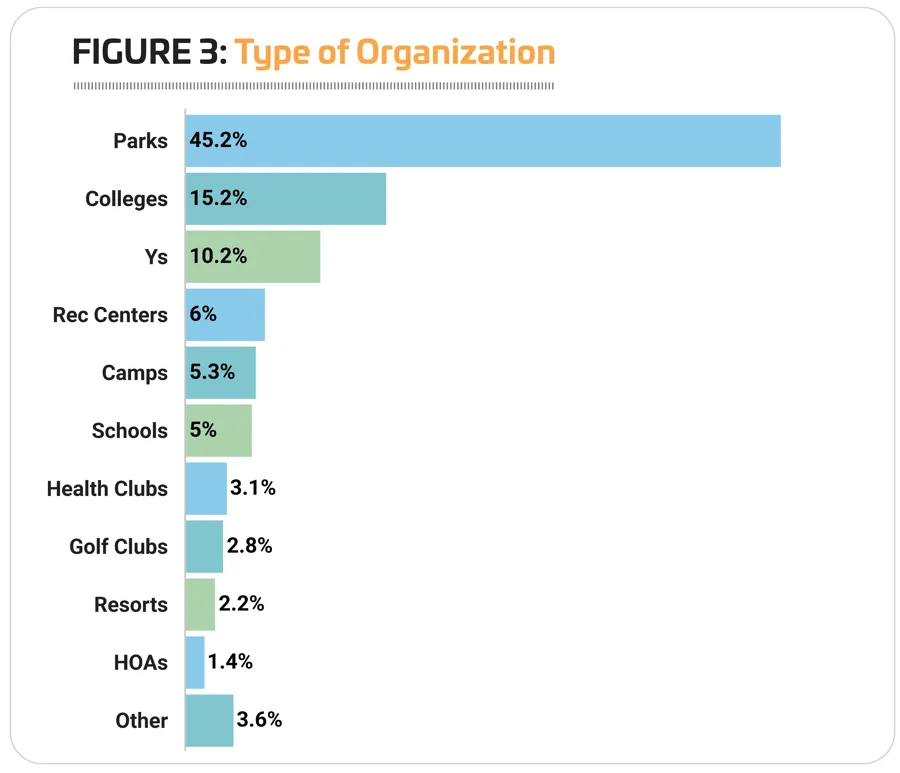

Parks and recreation departments and districts were the type of organization most prominent among respondents, with 45.2% of respondents indicating they work for this type of organization. They were followed by: colleges and universities (15.2%); YMCAs, YWCAs, JCCs and Boys & Girls Clubs (10.2%); community or private recreation and sports centers (6%); campgrounds, RV parks and private or youth camps (5.3%); schools and school districts (5%); sports, health and fitness clubs, and medical fitness facilities (3.1%); golf or country clubs (2.8%); resorts and resort hotels (2.2%); and homeowners' associations (1.4%). Another 3.6% were from other types of organizations, including churches and military installations, among others. (See Figure 3.)

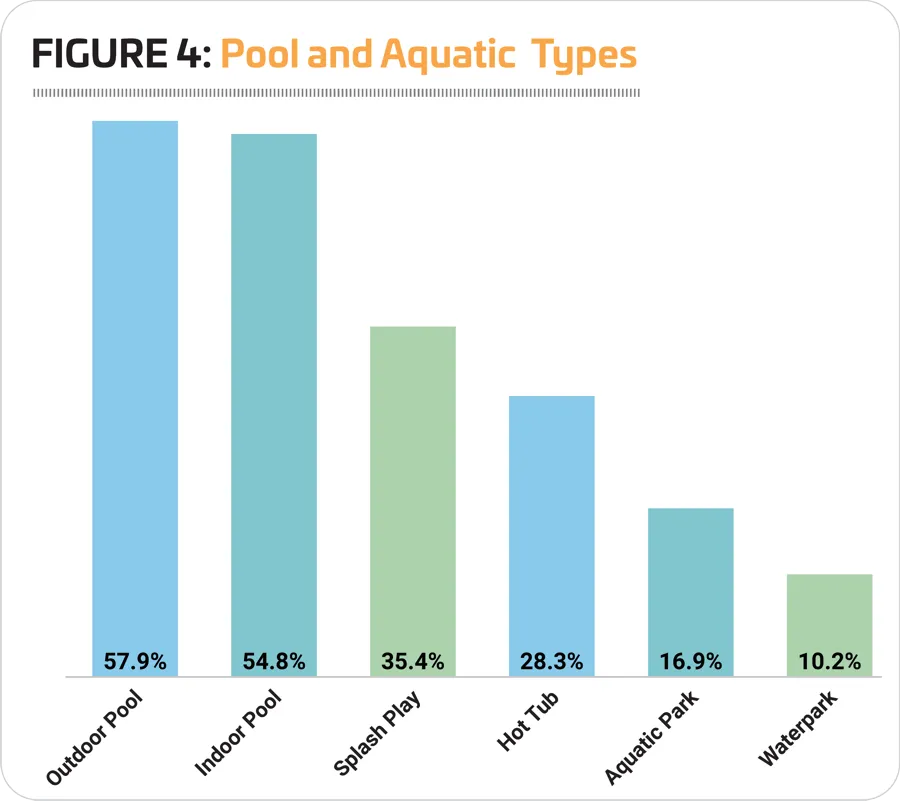

Aquatic facilities are certainly not one-size-fits-all, and there was a wide range of types of aquatic facilities represented in the survey response. The most predominant type was outdoor swimming pools, found in the facilities of 57.9% of the respondents. More than half (54.8%) also had at least one indoor swimming pool. Splash play areas also continue to be popular, with 35.4% of respondents indicating they had at least one. Some 28.3% said they had at least one hot tub, spa or whirlpool. When it comes to slightly more complex facilities, 16.9% of respondents said they had at least one aquatic park (with a focus primarily on swimming pools and other aquatic activities), while 10.2% said they had at least one waterpark (with a focus primarily on rides and waterslides). (See Figure 4.)

Outdoor swimming pools were most commonly found among respondents from camp facilities, where 85.3% said they had at least one outdoor pool. They were followed by parks respondents, 75.7% of whom had at least one outdoor pool, and rec centers, at 53.8%.

Indoor pools were most common for respondents from schools (93.8% had at least one indoor pool), colleges and universities (87.8%), and Ys (80.3%).

Splash play areas were most commonly found among park facilities, where 59.6% of respondents said they had at least one splash play area. They were followed by rec centers, 28.2% of which had at least one splash play area.

Hot tubs, spas and whirlpools were most prevalent among rec centers, where more than half (51.3%) said they had at least one hot tub. They were followed by Ys (43.9%) and colleges (28.6%).

Aquatic parks were most commonly found among the facilities of respondents from parks (29.8% said they had an aquatic park) and rec centers (10.3%).

Finally, waterparks were most prevalent among the facilities of parks respondents (15.1% of whom said they had a waterpark) and camp respondents (14.7%).

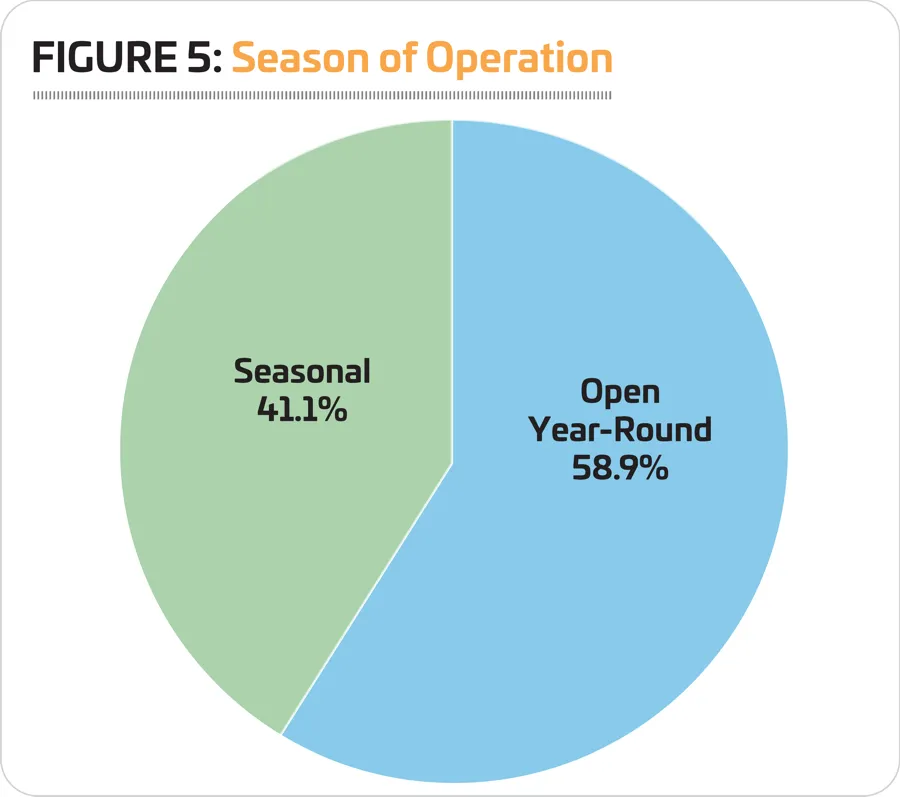

Well over half of respondents (58.9%) said their aquatic facilities are open year-round, while 41.1% said their operations are seasonal. (See Figure 5.)

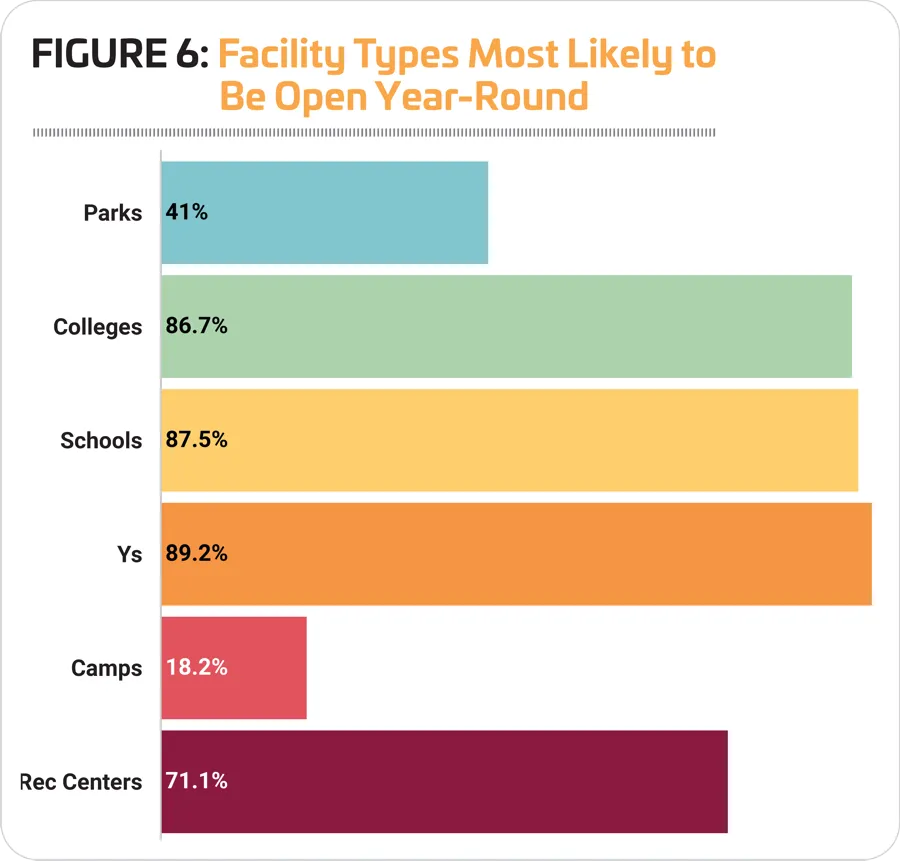

Respondents from Ys, schools and colleges were the most likely to indicate that their aquatic facilities are open year-round. Some 89.2% of Y respondents, 87.5% of school respondents and 86.7% of college respondents said they had year-round operations. Respondents from camps were the least likely to be operating year-round. (See Figure 6.)

Not surprisingly, respondents who only had indoor pools were more likely to operate year-round than those who only had outdoor pools. Among those with indoor-only facilities, 89.7% said they operated year-round. This compares with 21.8% of those with outdoor-only facilities.

Among respondents with seasonal operations, May was the most common month for beginning the aquatic season, while September was the most likely month for closing operations for the year. Some 58.4% of those with seasonal operations said their season begins in May, while 24% said they open for the season in June. On the other end of the season, 47.5% of those with seasonal operations close down in September, and 29.3% end their season in August.

Budget Issues

After a relatively sharp increase from 2018 to 2019, aquatic operating costs fell in 2020, for obvious reasons. Pools still had to be maintained, but with fewer swimmers, costs were down, even with the costs associated with managing social distancing requirements. From 2018 to 2019, the average operating costs for aquatic facilities rose 9.4%, from $530,000 to $580,000. In 2020, those costs were down 5.2% from 2019 to an average of $550,000. Looking forward, respondents expected to spend an average of $610,000 in 2021, up 10.9% over 2020, but up just 5.2% over the average cost in 2019. (See Figure 7.)

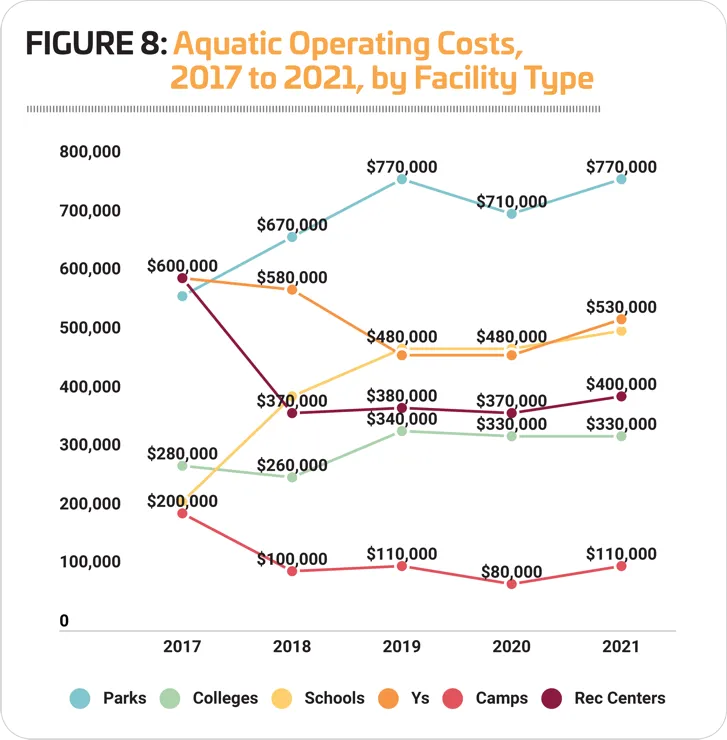

Respondents from parks had the highest average operating costs in 2019, reporting that they spent an average of $770,000. They were followed by schools and Ys, spending $480,000 and $470,000, respectively. Camps had the lowest average operating cost by far, spending an average of $110,000 in 2019. (See Figure 8.)

From 2019 to 2020, all types of respondents reported either no change or a decrease in their aquatic operating costs. The greatest decrease was reported by respondents from camps, who saw their aquatic operating expenses fall 27.3%, from $110,000 in 2019 to $80,000 in 2020. Smaller decreases were reported by parks (down 7.8%), colleges and universities (down 2.9%) and rec centers (down 2.6%). Respondents from schools and Ys reported no change to their average operating cost in that time frame.

Only colleges expect that their operating expenses in 2021 will be lower than their expenses in 2019. Among college respondents, no change is expected from 2020 to 2021, which marks a 2.9% lower average cost than 2019 ($330,000 vs. $340,000). Respondents from parks and camps expect their average operating cost in 2021 to return to the same level as 2019. The greatest increase over 2019 is expected by respondents from Ys, who anticipate an average operating cost of $530,000, up 12.8% from $470,000 in 2019. Smaller increases are expected among respondents from schools (up 6.3% in 2021 from 2019's cost) and rec centers (up 5.3%).

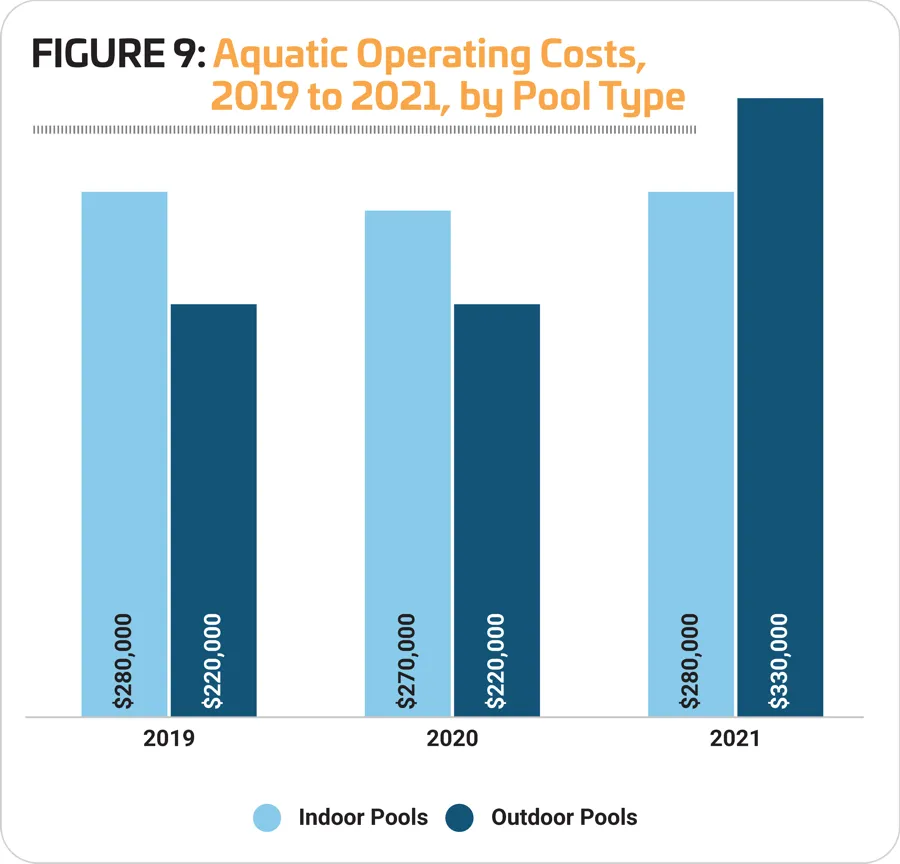

Comparing costs between facilities that only feature indoor or only feature outdoor pools, the data shows that those whose facilities only include indoor pools saw a slight decrease in operating expenses from 2019 to 2020, while those with only outdoor pools reported no change. From 2019 to 2020, those with indoor pools only saw their average operating costs fall by 3.6%, from $280,000 to $270,000. Looking forward, they expect their operating costs in 2021 to be the same as their costs in 2019. At the same time, while those with outdoor pools only reported no change to their average costs from 2019 to 2020, they expect a 50% increase in 2021, to an average of $330,000. (See Figure 9.)

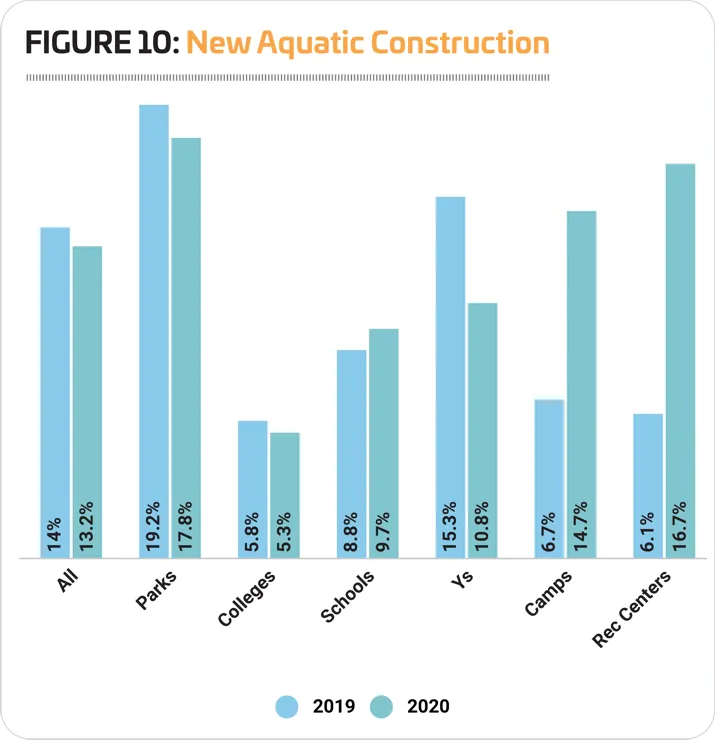

Some 13.2% of respondents reported that they had built a new aquatic facility in the past three years, down slightly from 14% in 2019 who had built a new facility. Respondents from parks were the most likely to have done so, with 17.8% indicating they had built a new aquatic facility in the past three years. That said, there was a significant increase in the number of rec centers and camps that had built new facilities. Some 16.7% of rec centers in 2020 said they had built a new aquatic facility in the past several years, compared to 6.1% in 2019. And among camps, 14.7% in 2020 said they had recently built new facilities, compared with 6.7% in 2019. Schools also saw an increase in the number of respondents who have built new aquatic facilities, from 8.8% in 2019 to 9.7% in 2020. (See Figure 10.)

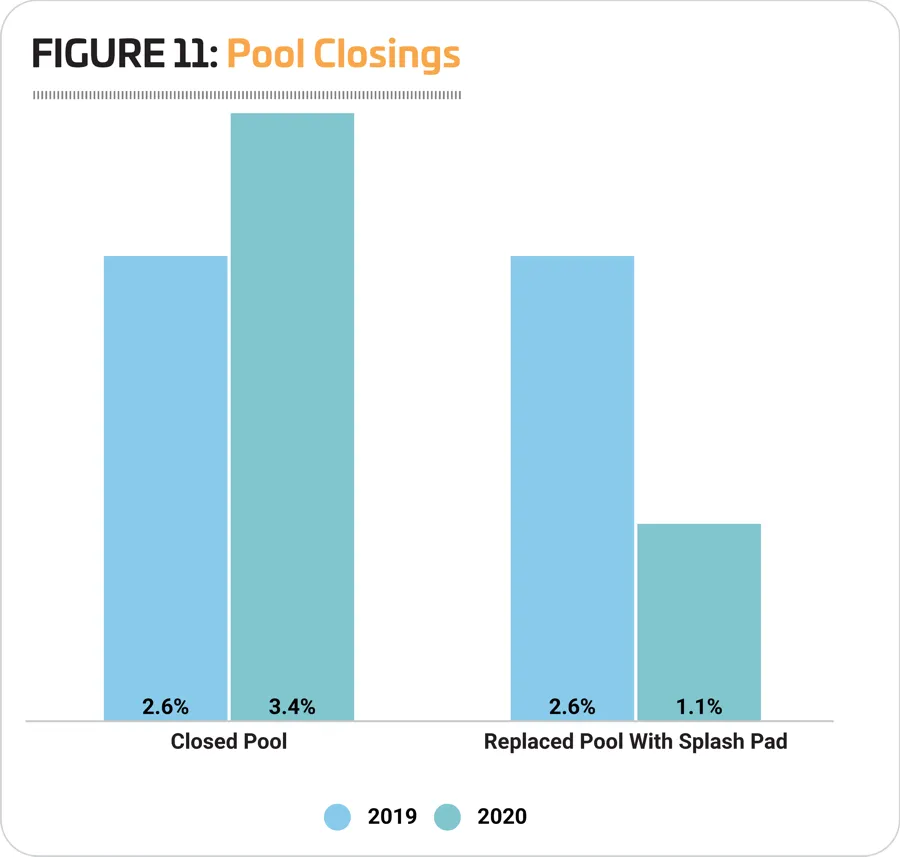

When it comes to pool closings, while they continue to be relatively rare, there was a slight increase in the number of respondents who said they had permanently closed a pool. In 2020, 3.4% of all respondents said they had permanently closed a pool without building a replacement, compared to 2.6% in 2019. At the same time, the number who had replaced a pool with a splash pad decreased, from 2.6% in 2019 to 1.1% in 2020. (See Figure 11.)

Respondents from schools and colleges were the most likely to report that they had permanently closed an aquatic facility, with 6.5% of schools and 6.4% of colleges indicating they had done so. Respondents from parks were the most likely to report that they had replaced a pool with a splash pad, with 2.1% indicating they had taken this action.

Water & Resource Management

Respondents to the Aquatic Report survey indicated the various types of systems used to filter their water and maintain water quality, as well as their use of secondary disinfection and their methods for conserving resources, such as water, chemicals and energy.

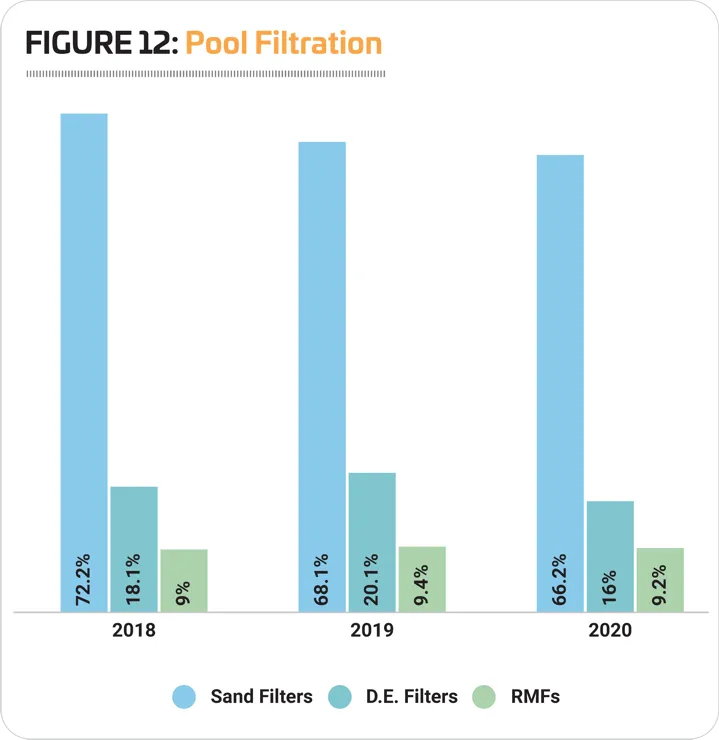

When it comes to pool filtration, sand filters are still dominant, though the number of respondents using them has fallen over the past three years, from 72.2% in 2018 to 66.2% in 2020. Diatomaceous earth (D.E.) filters also saw a decline in use in 2020, from 20.1% in 2019 to 16% in 2020. Regenerative media filters (RMFs) have seen fairly steady use over the past three years, with around one out of 10 respondents (9.2%) using them in 2020. (See Figure 12.)

A majority of respondents—80%--said they currently use chlorination systems at their aquatic facilities, while 11.6% are using bromination systems. More than one-third (35.6%) said they currently use a tablet chlorination system, while 7% are using salt chlorine generators.

Looking forward, 11.6% of respondents said they had plans to add new systems or update existing systems at their aquatic facilities over the next three years. As that relates to pool filtration, respondents were most likely to be planning to add either RMFs or sand filters. Some 16% planned to add RMFs, and 16% planned to add sand filters. Another 13.3% are planning to add D.E. filters at their aquatic facilities.

For the most part, the numbers of respondents planning these system changes at their facilities have all decreased from last year. The one exception is salt chlorine generation. Some 12% of respondents said they are planning to add salt chlorine generators, up from 10.5% in 2019.

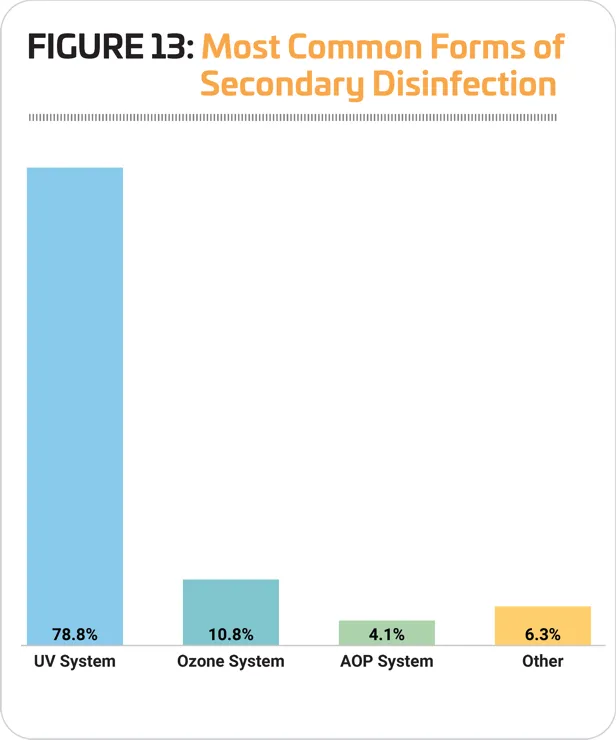

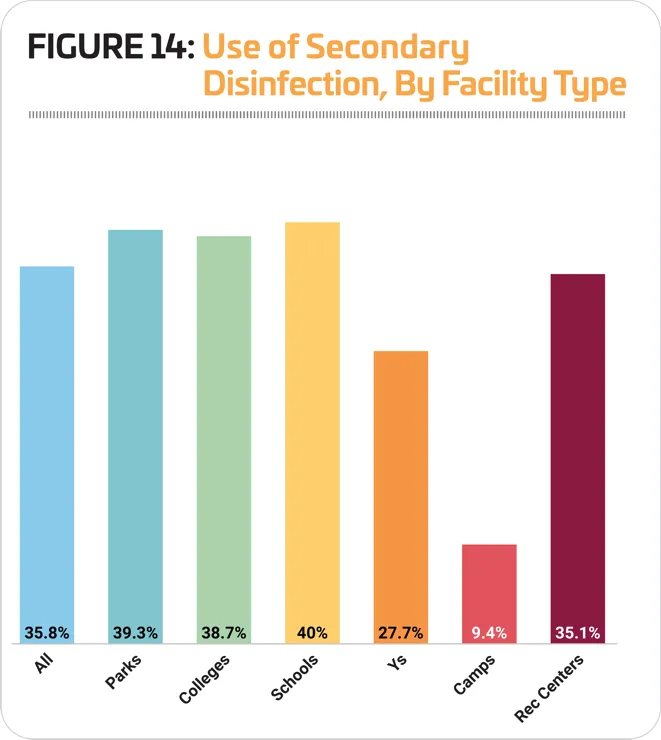

When it comes to secondary disinfection, which is recommended by the Model Aquatic Health Code (MAHC) as a way to improve water quality and prevent recreational water illnesses, 35.8% of respondents indicated that they currently employ some form of secondary disinfection, down from 36.4% in 2019, but still above 2018's 32%. More than three-quarters (78.8%) of respondents using secondary disinfection said they are using UV systems, down from 84.7% in 2019. Another 10.8% are using ozone systems (up from 6.5%), and 4.1% are using AOP (advanced oxidation process) systems, up from 4%. Some 6.3% said they are using some other form of secondary disinfection. (See Figure 13.)

Respondents from schools, parks and colleges were the most likely to report that they currently use a form of secondary disinfection at their aquatic facilities. Some 40% of school respondents said they do so, followed by parks (39.3%) and colleges (38.7%). Camp respondents were the least likely to use secondary disinfection—just 9.4% said they do so. (See Figure 14.)

Respondents whose facilities have higher average operating costs are more likely to report that they use secondary disinfection than those with lower costs. Well over half (58.8%) of those whose operating costs average more than $500,000 a year said they currently use secondary disinfection, down slightly from 63.9% in 2019. For those with operating costs between $250,000 and $499,999, 37.5% currently use secondary disinfection, up from 33.9% in 2019. And for those whose costs are less than $250,000 on average, 25% currently use secondary disinfection, down slightly form 25.8% in 2019.

Respondents who have indoor pools only are more than twice as likely to use secondary disinfection than those with outdoor pools only. Some 28.2% of indoor pool respondents said they currently use secondary disinfection, compared with just 10.4% of those with outdoor pools. UV is the most common method used, with 23.6% of indoor pool respondents using this method, compared with 10.4% of those with outdoor pools only.

Looking forward, among those respondents who said they plan to make additions or modifications to their water treatment systems over the next few years, 41.3% are planning to add UV systems (down from 46.7% in 2019). Another 14.7% are planning to add AOP systems (up from 14.3%), and 12% are planning to add ozone (down from 15.2%).

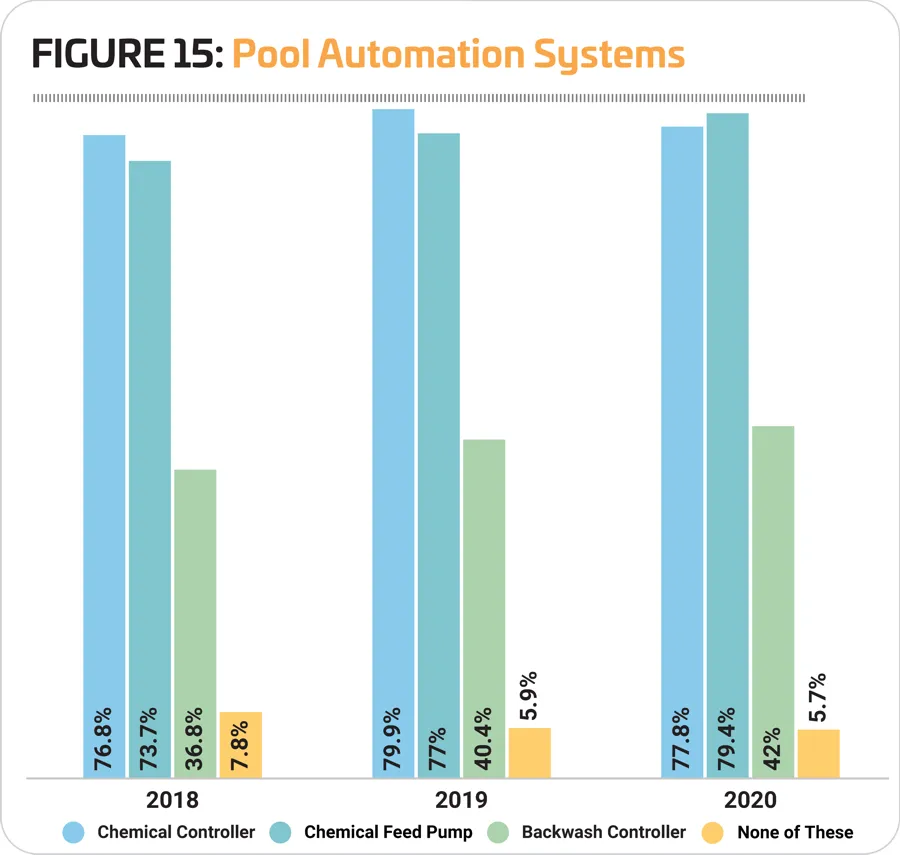

The use of pool automation systems has seen growth over the past few years, as the percentage of respondents who report that they do not use a chemical controller, chemical feed pump or backwash controller has fallen. Some 79.4% of respondents in the current study said they use chemical feed pumps, up from 77% last year. Another 77.8% use chemical controllers (down from 79.9%), and 42% use backwash controllers (up from 40.4%). (See Figure 15.)

Slightly fewer respondents to this year's survey said they have strategies and tools in place to conserve resources. In 2019, we reported that 71% of respondents were conserving resources, a number that fell to 69.2% in 2020. More than half (53.8%) said they aim to conserve chemicals, while slightly fewer respondents said they have strategies and tools for conserving energy (47%, down from 53.6%) and water (45%, up from 43.4%).

Respondents from schools and camps were the most likely to report that they currently aim to conserve energy, chemicals or water. Some 84.4% of school respondents currently do so, up from 70.6% in 2019. Interestingly, camps were the least likely to take such actions in 2019, and the percentage of camp respondents who aim to conserve resources has grown dramatically over the past three years, from 46.9% in 2018 to 78.1% in 2020. Parks and Ys were the least likely to report that they have strategies and tools for conserving chemicals, energy and water in 2020—with 66.8% of parks and 69.5% of Ys indicating they employ such measures.

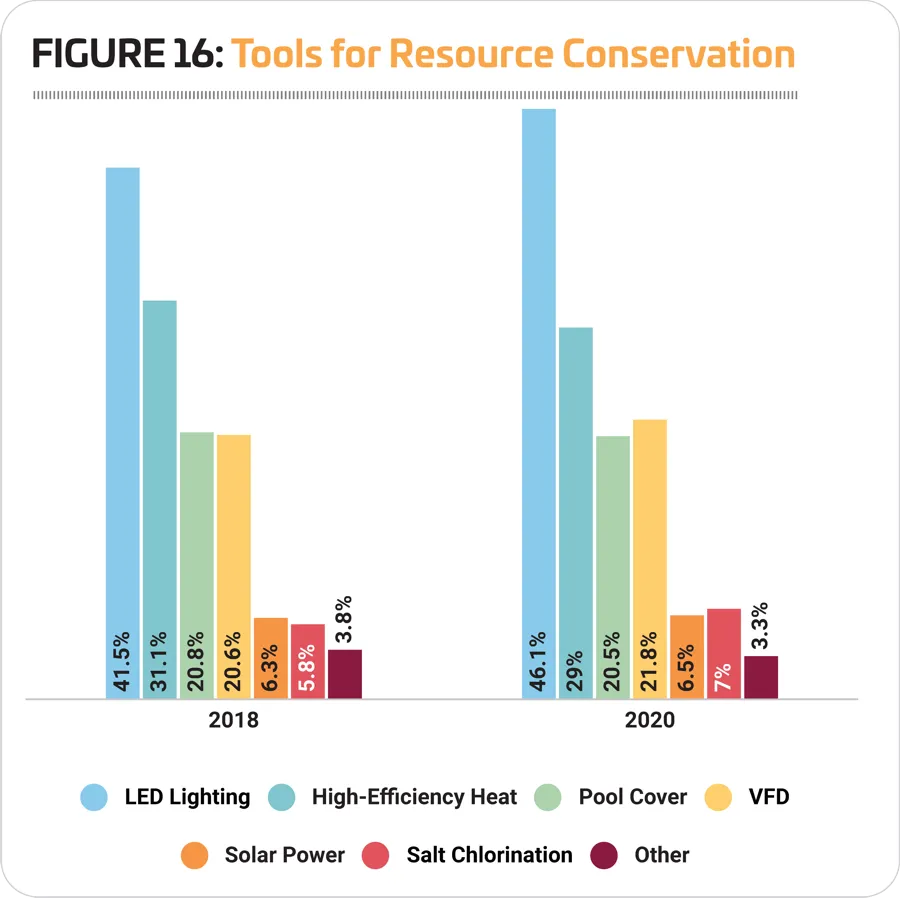

The most common tools used to conserve energy, chemicals and water at aquatic facilities included LED lighting (used by 46.1% of all respondents, up from 41.5% in 2018) and high-efficiency heaters (used by 29%, down from 31.1% in 2018). Another 21.8% rely on VFDs, up from 20.6%, and 20.5% use pool covers or blankets, virtually unchanged from 2018. (See Figure 16.)

CERTIFIABLE

Certifications, such as the Certified Pool & Spa Operator (CPO), with their ongoing educational requirements, help ensure that aquatic facility professionals are on top of all the best practices in aquatic operations. Indeed, a growing number of respondents to the Aquatic Report survey report that they or someone at their facility currently hold this type of certification.

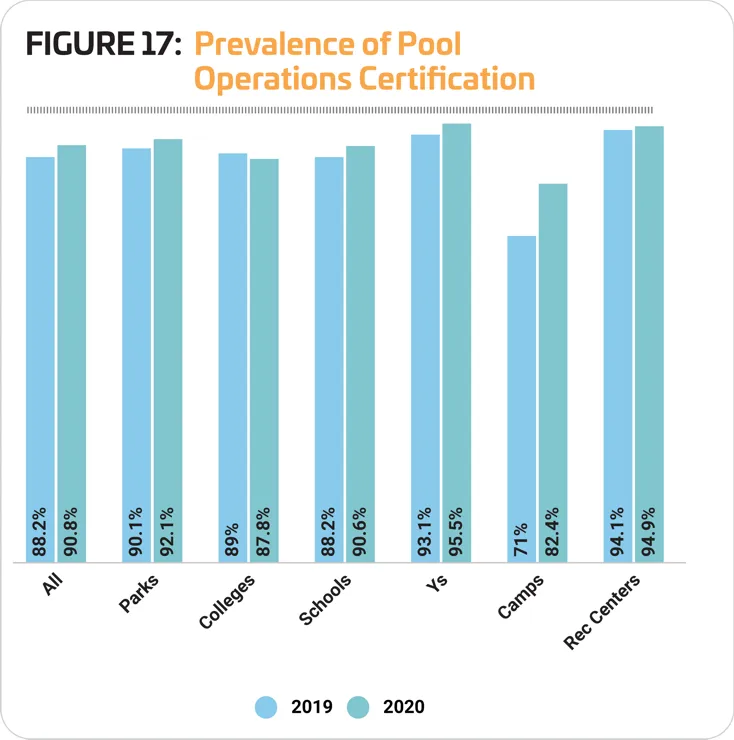

In 2020, 90.8% of all respondents said they or someone at their facility is certified, up from 88.2% in 2019. Respondents from Ys and rec centers were the most likely to be certified. Some 95.5% of Y respondents and 94.9% of rec center respondents said they or someone at their facility was certified in aquatic management or pool operations. In fact, the number reporting that they are certified grew for almost every category covered by the survey in 2020, with the exception of respondents from colleges and universities. (See Figure 17.)

Outfitting Aquatics

Over the past couple of decades, aquatic facilities have evolved rapidly beyond the rectangular pools of the past to include a wide variety of features that bring fun and fitness to the water, expanding all the ways people use aquatic facilities to keep them coming back for more.

Here are some of the more common features found among aquatic respondents' facilities:

- Lifeguard Stand: 78.2%

- Lane Lines: 77.7%

- Pool Lift or Other Accessibility Equipment: 63.6%

- Pool Exercise Equipment: 54.1%

- Diving Boards: 48.3%

- Starting Platforms: 46.3%

- Pool Slides: 36.7%

- Shade Structures: 34.3%

- Zero-Depth Entry: 34.2%

- Water Basketball Equipment: 33.9%

- Scoreboard: 28%

- Water Playground: 16.7%

- Pool Inflatables: 18.4%

- Water Polo Equipment: 20.8%

- Water Volleyball Equipment: 15.3%

- Teaching Platform: 15.3%

- Lazy River: 13.8%

- Diving Platforms: 13.2%

- Swim Platform 9.2%

- Poolside Cabanas: 9.5%

- Swim Wall or Pool Bulkhead: 11.3%

- Poolside Climbing Wall: 8.1%

- Lily Pads/Water Walk: 6.7%

- Underwater Treadmill or Bike: 4.3%

- Wave Pool: 2.7%

- River Raft Ride: 1.7%

- Surf Machine: 1.1%

- Water Coaster: 0.5%

The features that saw the greatest increase from 2019 to 2020, in terms of the number of respondents who include them in their facilities, include: water basketball equipment (up 3.5 percentage points); scoreboards (up 3); pool exercise equipment (up 2.6); swim walls or pool bulkheads (up 2.5), and water polo equipment (up 1.2).

Respondents from parks were the most likely to include many of these types of features at their facilities. Interestingly, most of the equipment related to aquatic recreation was most likely to be found at facilities operated by parks, while fitness and competitive equipment was more dominant at other types of facilities.

Parks were more likely than others to include: pool slides, water coasters, river raft rides, poolside climbing walls, lily pads and water walks, wave pools, water playgrounds, zero-depth entry, lazy rivers, shade structures, surf machines, and lifeguard stands.

Respondents from schools were more likely than others to include: diving boards, starting platforms, lane lines, water basketball equipment, scoreboards, and swim platforms.

College respondents were more likely than others to include diving platforms, water polo equipment and swim walls or bulkheads.

Respondents from Ys were more likely to include pool exercise equipment, underwater treadmills or bikes, and pool lifts or accessibility equipment.

Respondents from camps were more likely than others to use pool inflatables and water volleyball equipment; and rec center respondents were more likely to have teaching platforms and poolside cabanas.

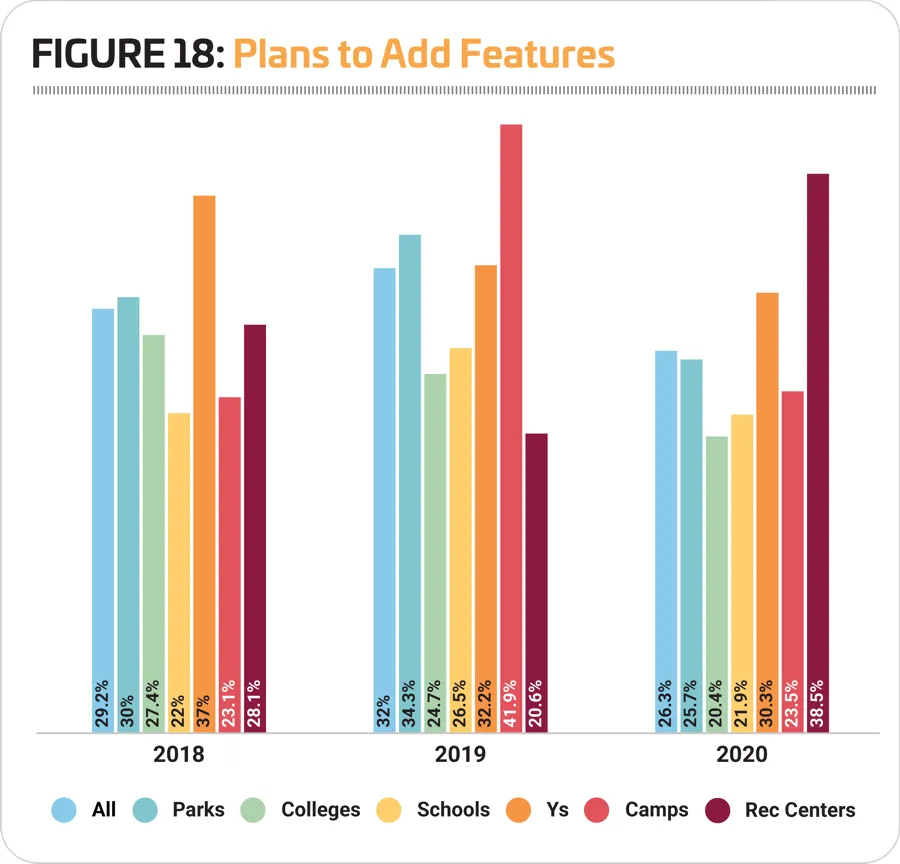

Not surprisingly, considering the challenges that pandemic-related shutdowns will place on facilities, the number of respondents with plans to add features at their facilities fell in 2020 to 26.3%, down from 32% in 2019. Respondents from rec centers and Ys were the most likely to have such plans. Some 38.5% of rec center respondents and 30.3% of Y respondents said they planned to add features at their facilities. Respondents from colleges and schools were the least likely to be planning to add features to their facilities, though 20.4% and 21.9%, respectively, said they were planning to do so. (See Figure 18.)

The 10 most commonly planned additions at aquatic facilities include:

- Shade structures (planned by 28.2% of those who will be making additions, down slightly from 28.9%)

- Poolside climbing walls (21.2%, down from 21.5%)

- Pool inflatables (21.2%, up from 20.2%)

- Pool slides (15.3%, down from 18.9%)

- Pool lifts and accessibility equipment (14.7%, up from 12.3%)

- Water playgrounds (14.1%, down from 15.9%)

- Zero-depth entry (13.5%, up from 13.2%)

- Pool exercise equipment (12.9%, down from 18.4%)

- Underwater treadmills or bikes (12.4%, up from 12.3%)

- Poolside cabanas (11.8%, down from 14.9%)

In addition to being among those most likely to be planning any additional features at their aquatic facilities, respondents from Ys were the most likely to be planning to add more different kinds of features than any other respondent cohort, other than camps. Respondents from Ys were the most likely to be planning to add: pool slides, pool inflatables, lane lines, underwater treadmills or bikes, zero-depth entry, lazy rivers, water polo equipment, and swim platforms.

While camps were less likely to be planning additional features, they were still the most likely to be planning to add: starting platforms, wave pools, water playgrounds, pool lifts and accessibility equipment, shade structures, water basketball equipment, water volleyball equipment, and swim walls or pool bulkheads.

Respondents from parks were the most likely to be planning to add: water coasters, pool exercise equipment, teaching platforms, poolside cabanas, and surf machines.

Rec center respondents were the most likely to be planning to add poolside climbing walls, diving boards and scoreboards. College respondents were the most likely to be planning to add diving platforms, while those from schools were the most likely to be planning to add lifeguard stands.

Programming

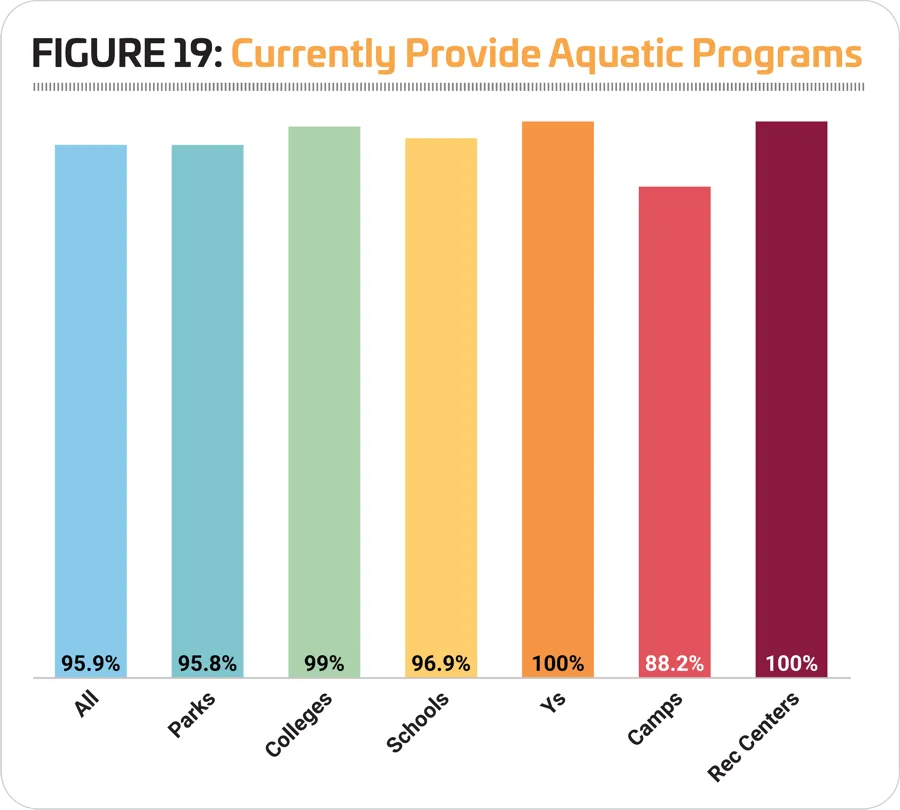

Not every aquatic facility needs to offer programming to entice swimmers to the water (splash pads and waterparks, for example). However, offering programs like learn-to-swim and aquatic exercise offers a way to boost revenues and outreach. A majority—95.9%—of respondents to the survey said they do currently provide some type of programming at their facilities. This is virtually unchanged from 2019, when 95.8% provided programming. In fact, 100% of respondents from Ys and recreation centers said they currently provide programming. They were followed by college respondents, 99% of whom currently provide programming. Camp respondents were least likely to do so, though a majority—88.2%—of these respondents said they currently do provide programming at their aquatic facilities. (See Figure 19.)

The following are the types of programs covered in the survey and their prevalence among respondents' offerings:

- Learn-to-Swim Programs (79.1%)

- Lifeguard Training (76.1%)

- Leisure Swim Time (73.3%)

- Lap Swim Time (73.3%)

- Birthday Parties (58.5%)

- Aquatic Aerobics (65.2%)

- Water Safety Training (56.3%)

- Youth Swim Teams (57.2%)

- Swim Meets & Other Competitions (49%)

- Aquatic Programs for Those With Physical Disabilities (34.6%)

- School Swim Teams (33.3%)

- Aquatic Programs for Those With Developmental Disabilities (28%)

- Water Walking (29.1%)

- Dive-In Movies (24.3%)

- Aquatic Therapy (24%)

- Adult Swim Teams (20.2%)

- Aqua-Yoga & Other Balance Programs (22.1%)

- Diving Programs & Teams (17.5%)

- Water Polo (15.8%)

- Doggie Dips (12%)

- Collegiate Swim Teams (11.7%)

Only two types of programs saw an increase in 2020: collegiate swim teams (up 2.6 percentage points), and water polo (up 0.5).

Ys generally lead the way in terms of programming, whether facilities are aquatic or not, and this year offers no exception to that rule. Respondents from Ys were the most likely to offer: learn-to-swim programs, youth swim teams, aquatic programs for those with physical and developmental disabilities, aquatic aerobics, aqua-yoga, water walking, lap swimming, aquatic therapy, water safety programs, lifeguard training and birthday parties.

Respondents from colleges were the most likely to provide adult and collegiate swim teams, leisure swim and water polo programs.

School respondents were the most likely to provide school swim teams, swim meets and competitions, and diving programs and teams.

Park respondents were the most likely to offer doggie dips and dive-in movies.

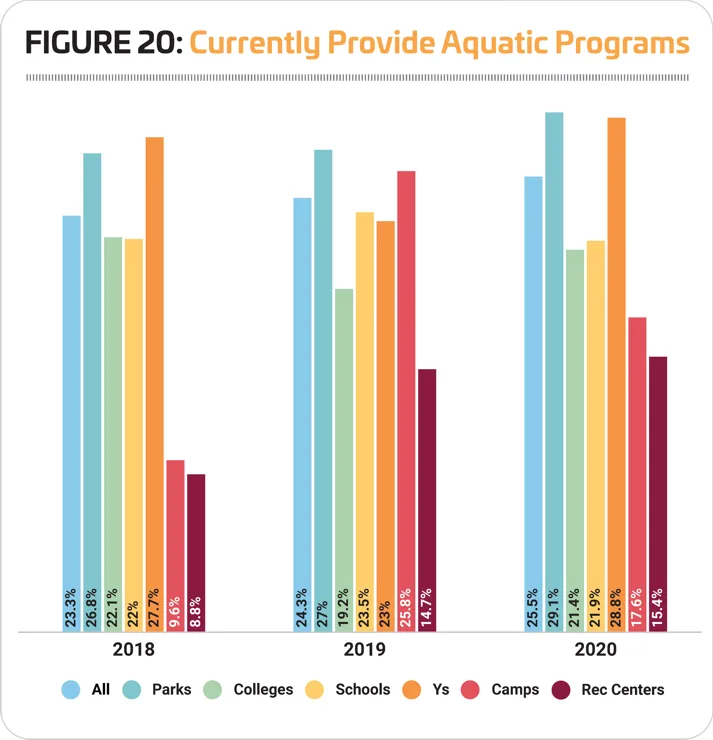

More than one-quarter (25.5%) of respondents said they have plans to add more programs at their facilities over the next three years, up from 24.3% in 2019. Respondents from parks and Ys were the most likely to report that they have such plans. Some 29.1% of park respondents said they would be adding programs at their facilities, up from 27% in 2019. And 28.8% of Y respondents plan to add programs, up from 23%. Rec center respondents were the least likely to be planning program additions, though 15.4% said they have such plans, up from 14.7% in 2019. (See Figure 20.)

The top 10 most commonly planned program additions include:

- Programs for those with physical disabilities (planned by 30% of those who will be adding programs, up from 28.3% in 2019)

- Dive-in movies (29.1%, down from 38.7%)

- Programs for those with developmental disabilities (26.1%, virtually unchanged from 26%)

- Aqua-yoga and other balance programs (24.2%, down from 28.3%)

- Aquatic aerobics (18.8%, down from 21.4%)

- Learn-to-swim programs (16.4%, up from 12.1%)

- Water safety training (12.7%, up from 11%)

- Adult swim teams (10.9%, down from 16.2%)

- Lifeguard training (10.9%, up from 9.2%)

- Youth swim teams (10.3%)

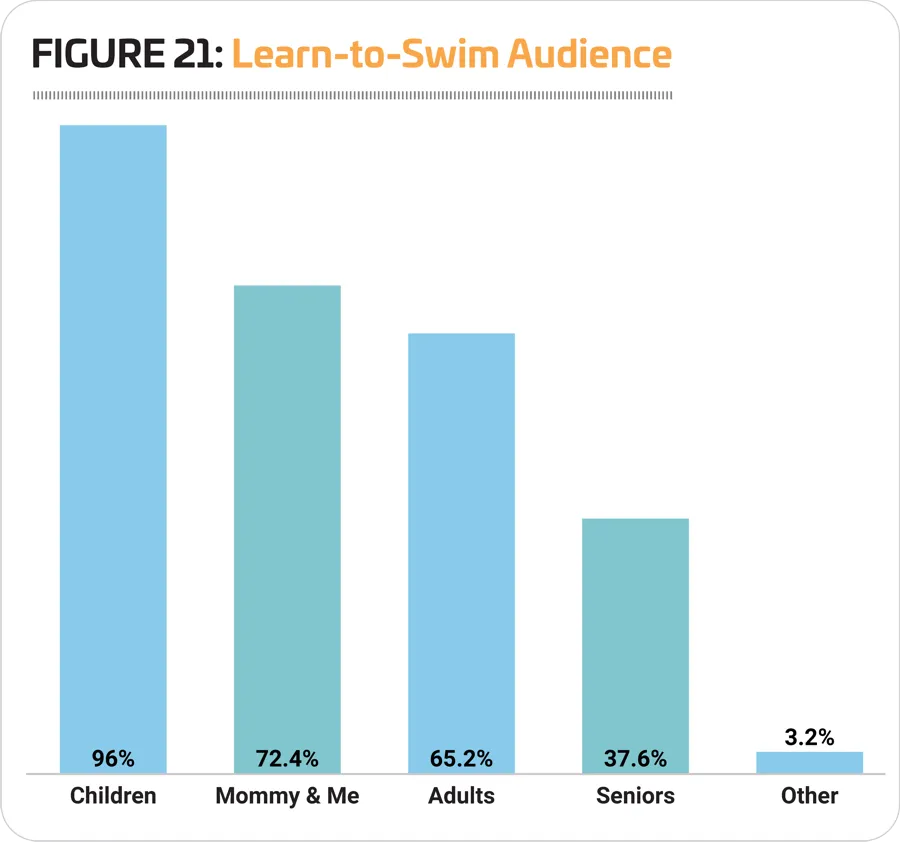

We asked the 79.1% of respondents who offer learn-to-swim programs some further questions about the audience they reach with their programs. While children are obviously the most common audience for such programs, there are learn-to-swim programs designed to meet just about everyone's needs.

A substantial majority (96%) of respondents who provide learn-to-swim programs are reaching children ages 17 and younger. Another 72.4% provide programs for parents and babies or toddlers (such as mommy—or daddy—and me classes). Almost two-thirds (65.2%) provide learn-to-swim programs for adults 18 and up, and 37.6% provide learn-to-swim programs for seniors. (See Figure 21.)

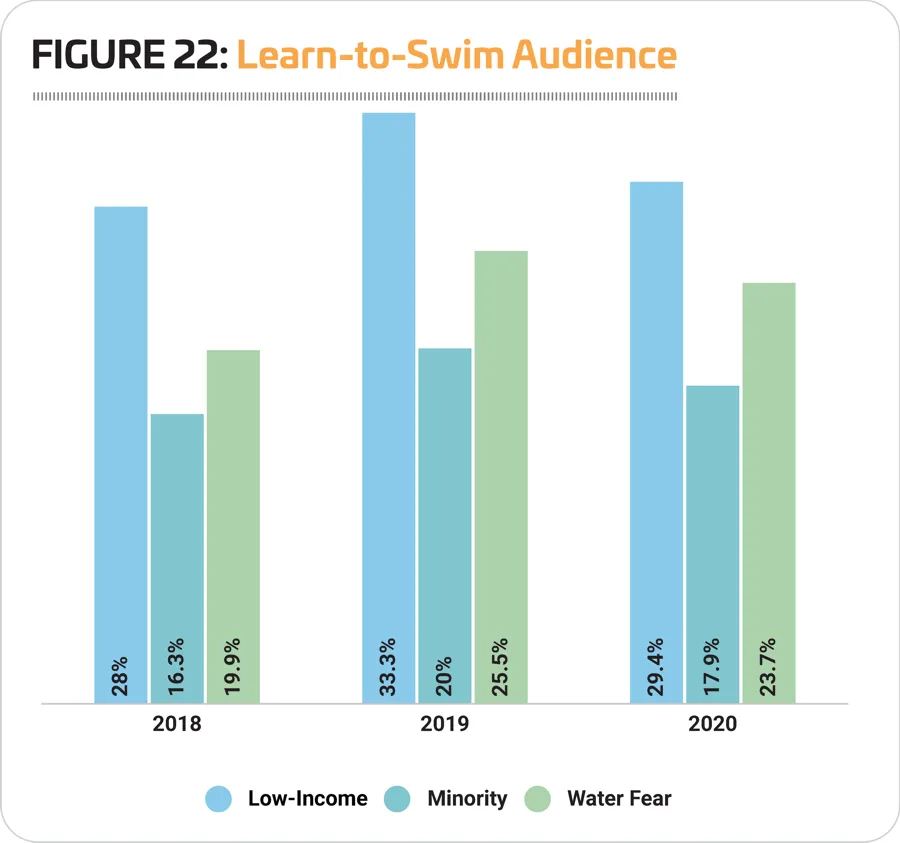

According to USA Swimming, 79% of children in low-income families have little to no swimming ability. There are also racial disparities in swimming ability: 64% of black children and 45% of Hispanic children have little to no swimming ability, compared with 40% of white children. To address these disparities, as well as to reach those who lack swimming ability because of a fear of water, many facilities have outreach programs aimed specifically at low-income, minority and water-phobic groups. Nearly three in 10 (29.4%) respondents said they currently have a low-income outreach program, down from 33.3% in 2019. Another 17.9% said they engage in minority outreach, down from 20%. And 23.7% offer learn-to-swim programs that aim to help patrons overcome water fear, down from 25.5% in 2019. (See Figure 22.)

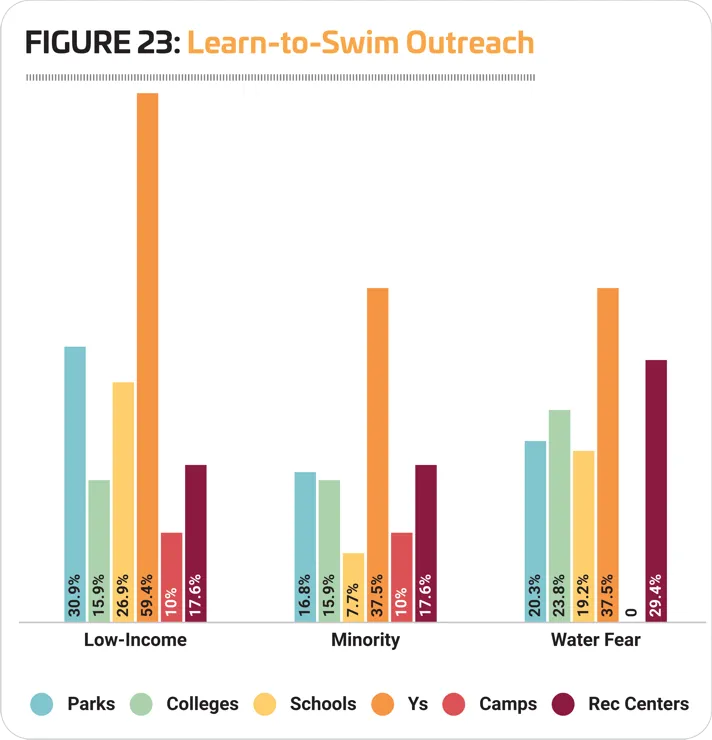

Respondents from Ys were by far the most likely to reach out to low-income, minority and water-phobic audiences. In fact, more than half (59.4%) of Y respondents who had learn-to-swim programs said they had low-income outreach programs, while 37.5% engaged in minority outreach, and 37.5% had programs for those looking to overcome a fear of water. More than three in 10 park respondents (30.9%) said they had low-income outreach programs. Some 17.6% of rec center respondents had minority outreach programs. And 29.4% of rec center respondents provided programs to help people overcome their water fears. (See Figure 23.)

Safe in the Water

As mentioned, more than half (56.3%) of respondents provide water safety training as part of their programming lineup, but this isn't the only way these facilities address safety and work to prevent drownings.

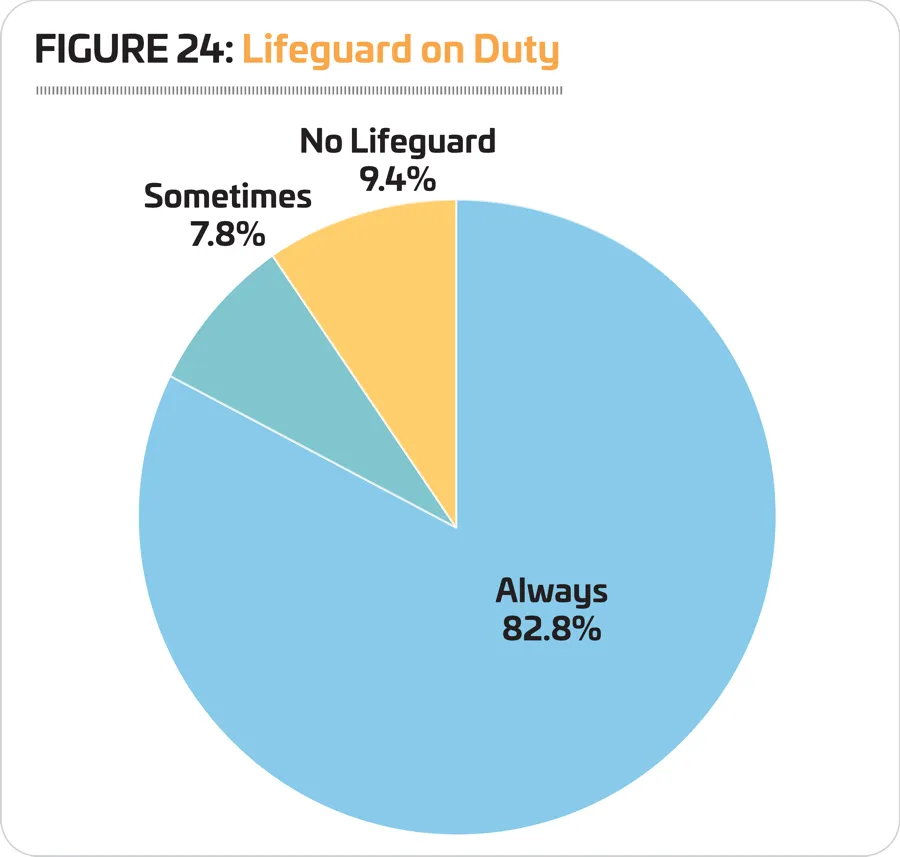

A majority of respondents—90.6%—said a lifeguard is on duty at least some of the time during their operating hours. Some 82.8% said a lifeguard is on duty at all times the facility is open (down slightly from 84.1% in 2020), and 7.8% said a lifeguard is on duty during at least some hours of operation (up from 6.5%). Just 9.4% said there is never a lifeguard on duty at their facilities, representing no change from last year's report. (See Figure 24.)

As was the case in last year's survey, 100% of the respondents from Ys said that a lifeguard is on duty at least some of the time. But in a change, this year 100% of Y respondents said a lifeguard is on duty at all times, whereas last year, that number was 98.8%, with 1.2% indicating a lifeguard was on duty only sometimes.

Colleges and schools were the next most likely to have a lifeguard on duty, with 96.9% of each cohort indicating that a lifeguard is on duty at least some of the time. They were followed by park respondents, 95.5% of whom said a lifeguard is on duty at least some of the time.

Camps were the least like to indicate that a lifeguard is on duty during their hours of operation, though more than three-quarters (78.8%) said they have lifeguards. They were followed by rec centers, 87.2% of whom said a lifeguard is on duty at least some of the time during their hours of operation.

Lifeguards are aquatic facilities' most important tool to prevent drownings at their facilities, but they are not the only tool in that kit. When it comes to drowning prevention, here are the methods most often used by respondents:

- Lifeguard on Duty (90.6%, no change from 2020)

- Life Preservers Required for Less-Skilled Swimmers (51.6%, down from 56.9%)

- Video or Other In-Pool

- System for Detecting Swimmers

- in Trouble (5.4%, down slightly from 5.5%)

- Safety Device That Sounds an Alarm When Submerged (4%, down from 4.8%)

- Other (5%)

- None (7%, up from 5.7%)

Tracking Usage of the MAHC

Established by the U.S. Centers for Disease Control & Prevention (CDC), the Model Aquatic Health Code (MAHC) brings together the most up-to-date science and best practices with the goal of helping state and local government officials develop and update their pool codes. Historically developed at the local and state level, such codes govern pool operations, including how and how often water is tested, how aquatic facilities are built, how chemicals should be used to keep water safe and free from disease and more. The MAHC aims to create a more standardized set of guidance to establish rules and regulations for aquatic facilities that are based on industry consensus around best practices.

The MAHC was first released in the summer of 2014, but it is a fluid code, meant to be updated regularly as new information and input is made available. The third edition of the code was published in 2018, and the fourth edition is anticipated to be released for the summer 2021 swim season, according to the Council for the MAHC.

The code is not a federal law, which means government agencies can choose whether to adopt it at all, whether to use all of the MAHC or just part of it, or whether to modify all or part of it to fit their needs.

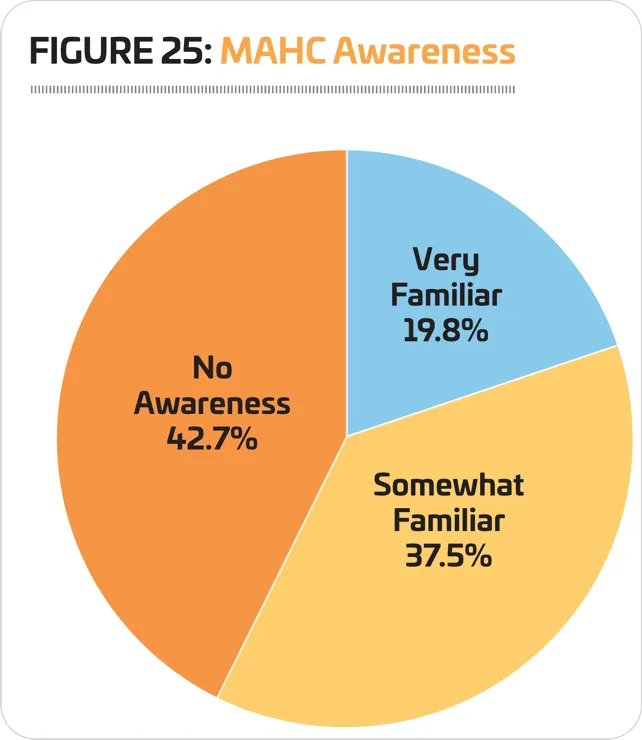

Nearly six in 10 (57.3%) respondents said they are familiar with the MAHC, representing virtually no change from last year's survey. Some 19.8% said they are very familiar with the MAHC, and 37.5% are somewhat familiar. (See Figure 25.)

To ensure the MAHC is regularly updated, a nonprofit organization, the Council for the Model Aquatic Health Code (CMAHC) was created in 2013. The council serves as a clearinghouse for input and advice on improvements to the MAHC. CMAHC members can take part in the process of updating the MAHC and have their input heard by the CDC as it revises and releases the next edition. (To learn more about participating in the CMAHC, visit www.cmahc.org.)

While a majority of respondents to the Aquatic Trends survey said they did not participate at all in the CMAHC, some 7.9% had some involvement, and 1.4% are on the committee itself.

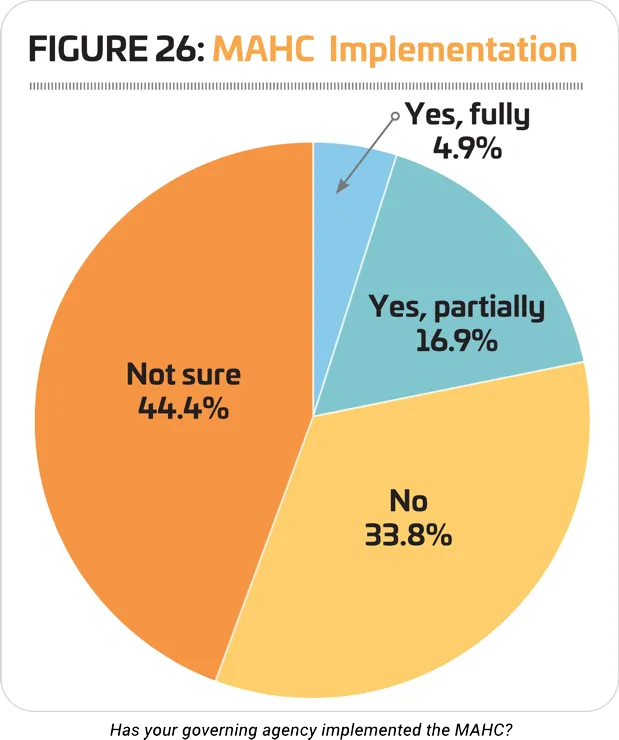

We also asked respondents whether the regulatory agency that governs their facilities has adopted the MAHC, either fully or partially. The largest number of these respondents—44.4%—were not sure, down from 46.3% last year. One-third (33.8%) said their regulatory agency had not adopted the MAHC. Some 4.9% said the MAHC had been fully implemented by their regulatory agency, and 16.9% said their agency had adopted portions of the code. (See Figure 26.)

Industry-Wide Challenges

Before we get to the elephant in the room, it's important to note that the impact of COVID-19 is not the only challenge or issue that aquatic managers have to deal with. Keeping equipment up to date and ensuring you have a well-trained staff in place, as well as budget challenges and managing safety also continue to be daily challenges aquatic managers must address.

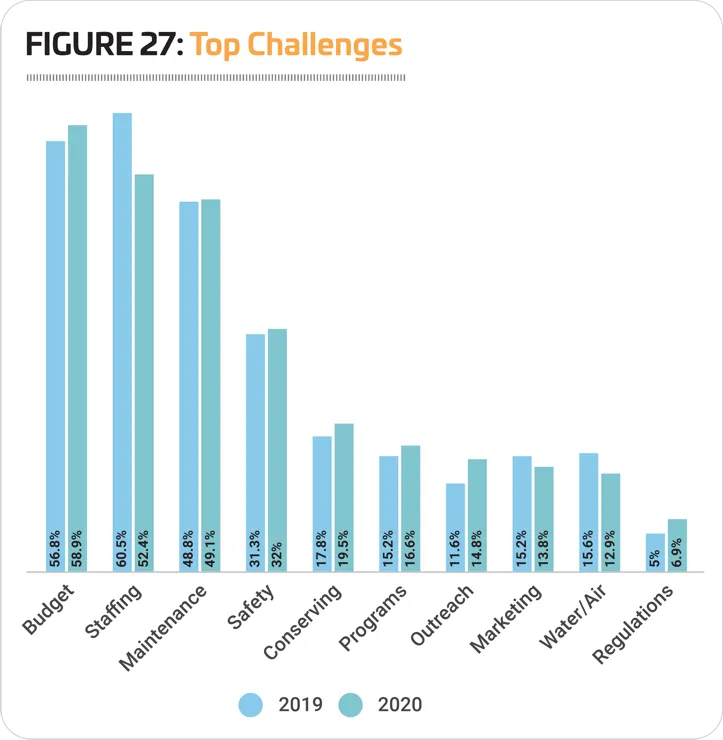

Respondents in 2020 said the top issues currently facing the aquatics industry include: budgets, staffing and equipment facility maintenance. This represents a slight shift from 2019, when staffing was the No. 1 concern for aquatic facilities.

Some 58.9% in 2020 said budgetary issues were the top challenge for the aquatics industry, up from 56.8% in 2019. Another 52.4% said staffing was a top challenge, down from 60.5%; and 49.1% said equipment and facility maintenance was their top challenge, up from 48.8%. (See Figure 27.)

The area of concern that saw the greatest increase over 2019 in terms of the number of respondents naming it a top challenge, was outreach to minorities and other underrepresented populations. Some 14.8% in 2020 named this a top concern, up 3.2 percentage points from 2019.

Other areas that were of greater concern in 2020 than in 2019 include: regulatory issues (up 1.9 percentage points); resource conservation (up 1.7); new programming ideas (up 1.4); and safety and risk management (up 0.7).

Parks were the most likely to indicate that staffing was a top concern. That said, they were most likely to consider budgetary issues as their top challenge (63.8%). This was followed by staffing (59%) and equipment and facility maintenance (47.6%).

College respondents were the most likely to name budgetary issues as their top challenge. More than seven in 10 (70.1%) college respondents said budgets were their top issue. That's up from 67.1% in 2019. This was followed by equipment and facility maintenance (55.7%) and staffing concerns (43.3%).

For school respondents, budgets were the top concern for 56.7%, followed by equipment and facility maintenance (53.3%) and staffing (50%). School respondents were also the most likely to report that outreach to minorities and underrepresented populations was a top concern for the aquatics industry. Some 23.3% of school respondents named this as a top concern.

For respondents from Ys, 56.1% named budgetary issues as a top industry concern, followed by staffing (51.5%) and equipment and facility maintenance (43.9%).

Camp respondents were the most likely to name equipment and facility maintenance as a top concern. In fact, this group of respondents bucked the trend for the year and named equipment and facility maintenance as their No. 1 concern, with 60.6% choosing this area. It was followed by budgetary issues (42.4%) and safety and risk management (39.4%).

Finally, 61.5% of rec center respondents named budgetary issues as their top concern. This was followed by staffing (41%) and equipment and facility maintenance (38.5%).

The Pandemic Effect

Obviously, the massive closures and adaptations to operations when (and if) facilities reopened was a tremendous challenge for aquatic facilities in 2020. With a vaccine distribution plan just getting under way, there is more hope for 2021, but with most experts hoping for a return to normal in late summer and early fall, the impact to the aquatics industry will be ongoing.

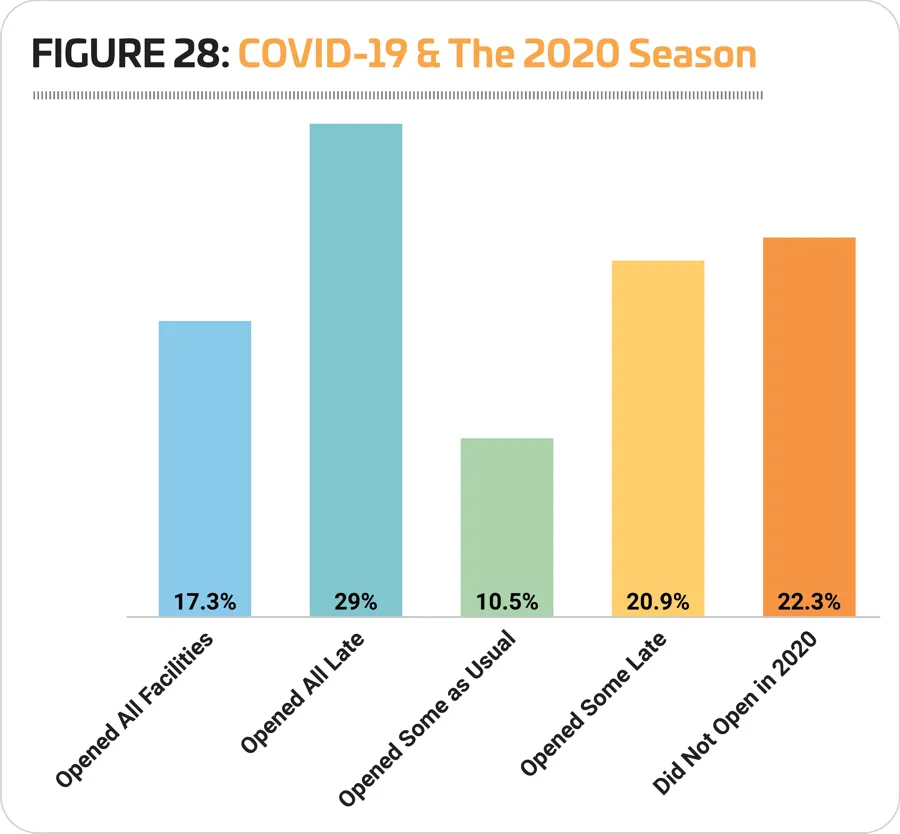

We asked respondents whether their aquatic facilities opened for the 2020 season, and in what capacity. More than two-thirds (77.7%) of respondents said they were open in some capacity for the 2020 season, and 22.3% did not open at all. Just under one-fifth (17.3%) of respondents said they opened all of their aquatic facilities according to their usual schedule, and 29% opened all of their facilities, but later than their usual opening date. Another 10.5% said they opened some, but not all, of their aquatic facilities according to their usual schedule, and 20.9% opened some, but not all, of their facilities, but later than their usual opening date. (See Figure 28.)

Respondents from Ys were the most likely to report that they had opened all of their aquatic facilities according to their regular schedule in 2020. Nearly half (47%) of Y respondents had done so. They were followed by schools, 21.9% of whom said their aquatic facilities were open as usual in 2020.

Respondents from camps were the most likely to indicate that they did not open at all in 2020, with more than a third (36.4%) reporting they did not open any aquatic facilities last year. They were followed by park respondents, 29.9% of whom did not open their aquatic facilities at all in 2020.

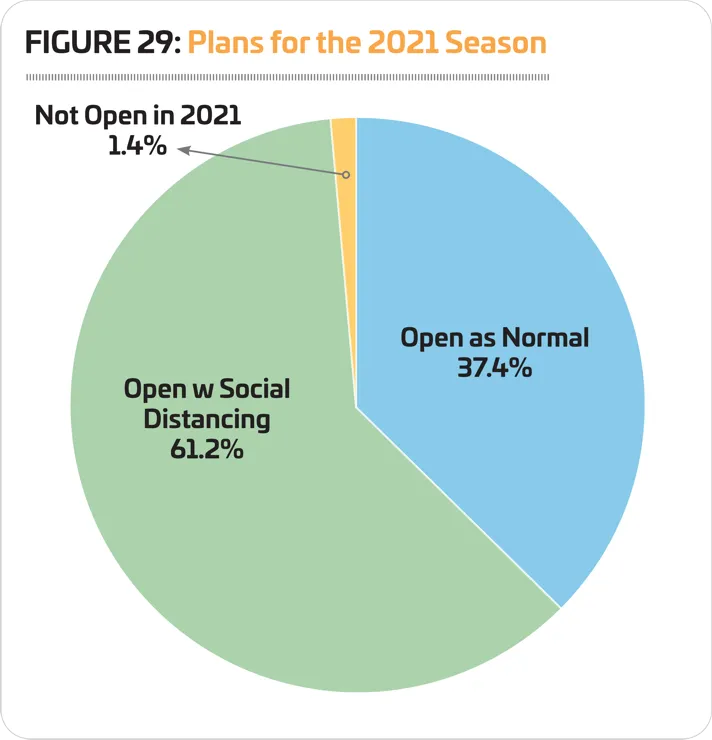

Looking forward, respondents were fairly positive about their prospects for the 2021 season. A full 98.6% of respondents expect their aquatic facilities to be either open as normal in 2021 (37.4%) or open as usual but with social distancing measures in place (61.2%). Only 1.4% said they will not be opening their aquatic facilities in 2021. (See Figure 29.)

We also asked respondents to describe the impact of COVID-19 on their facilities. There were a vast number of comments about lost revenues due to closures, and the methods (and associated challenges) of enforcing social distancing protocols once facilities were open again. Many respondents were also concerned about the impact on public safety following a season with so few learn-to-swim and water safety opportunities. Here are some additional comments from respondents:

"Due to COVID-19 we had intermittent closures of several facilities. The reduction in both expenditures and revenue will be felt for at least the next several years."

"At this point we have been closed since mid-March. We have no date for re-opening, but hope in spring of 2021. I think recertifying staff so we can re-open will be a huge challenge as well as getting our staff to return after having been gone for a calendar year."

"Operating with limited and modified programming limited the users of the community. Additionally, staffing was negatively impacted as hiring was difficult and current staff were not comfortable returning to work during COVID-19."

"Challenging summer, however we were able to open for 8 weeks out of our traditional 16-week season. Overall, very successful without a COVID case reported. Contact tracing and temp. check measures in place upon check-in. More staff hired (budgetary impacts) to ensure all safety precautions were followed."

"We lost five months of operation. Two of which were summer months. We remain at greatly reduced capacity. Safety issues continue to be top priority but cost recovery is a big issue moving forward."

"We have been closed for three consecutive seasons: Spring 2020, Summer 2020 and Fall 2020. Our health department has not prioritized our return to the pool for Winter 2021. We may not reopen until Spring or Summer of 2021. By then, with the high turnover of staff, it will be as if we are starting over, from scratch. We are the largest learn-to-swim program in our state with 12 pools that can be busy 5-6 days/week. Deaths due to drowning in Lake Michigan were at an all-time high this summer. For a large metropolis on the Lakefront, we are not surprised and recognize the role we play in water safety messaging."

"Since we provide various services to both indoor and outdoor facilities, both seasonal and year-round, the impact of the crisis had different impacts upon the facilities. Year-round indoor facilities have been hit hard due to closures and programming cancellations. The seasonal summer outdoor facilities, on the other hand, were able to adapt better due to the logistics of being outdoors and self-distancing is much easier. Yet membership at all facilities took a hit. The larger the facility the harder they were hit, especially economically. Smaller-scale facilities were able to adapt better, yet still certainly felt the impact. NYS and specifically NYC & Long Island imposed strict protocols for private and public aquatic and sports facilities. Though it hurts economically, health and safety were and still is key to providing a safe environment for members and staff. The impact still continues due to strict restrictions within New York State. It's a difficult balance between health and safety and downturns economically due to that. In the end there will be facilities that will permanently close, but NYS is trying to assist business weather this crisis. We'll see what the 6-12 months bring us all."

"Obviously, it was a difficult year, but I believe that the pandemic brought about a deeper appreciation for aquatics. Whether it be someone who needs exercise and lap swimming was the best option or parents who now have to be in the water with their children for lessons, it is a new aquatic world."

We also asked respondents about their post-COVID plans for their facilities, and generally speaking, everyone is looking forward to getting back to business as usual. Many respondents simply responded that they can't wait to simply open their facilities, but there was also a heavy emphasis on safety, as well as the need for staff training, ensuring facilities are in good working order, and boosting attendance again:

"After a rollercoaster of a year so far, the No. 1 goal is to take the lessons and solutions we learned from the summer and fall of 2020 and use that knowledge to improve both on health/safety and also using creative ways to rebound economically."

"Water safety should be the number one goal for every aquatic facility every year in my opinion. You can have a great business plan or want to introduce new programming, but without great water safety none of that really matters. We have worked really hard this past year to create a good lifeguard program for our own staff. Our number one goal this year will be to continue to build our water safety program so that everyone who swims at our facility will be able to have fun and exercise while feeling confident that they are safe and secure." RM