In these pages, we’ll examine the response from professionals working for parks and recreation districts, departments and related agencies. This group always represents the largest cohort of respondents to the Industry Report survey, hitting a low of 31.5% in 2023 and a high of 47.9% in 2019. In 2026, 40.3% of respondents were from parks and recreation organizations.

As always, park respondents were most likely to be located in the Midwest, with 31.6% of park respondents calling the Midwestern states home. They were followed by the West (26.3%), Northeast (18.9%) and South Atlantic (16.5%) regions. Park respondents were least likely to be located in the South Central states, with just 6.7% of the cohort calling the South Central region home.

As always, park respondents were most likely to be located in the Midwest, with 31.6% of park respondents calling the Midwestern states home. They were followed by the West (26.3%), Northeast (18.9%) and South Atlantic (16.5%) regions. Park respondents were least likely to be located in the South Central states, with just 6.7% of the cohort calling the South Central region home.

Nearly half (49.2%) of park respondents were located in suburban communities. Nearly three in 10 (29.3%) were located in rural areas, and 21.5% said they were from urban communities.

On average, park respondents said the average annual number of patrons they serve is 183,810, down slightly from 189,160 in 2025. The median, however, was higher than in 2025, at 38,690 vs. 29,470. Remember, the median is the number that falls in the exact middle of the spread, meaning half of respondents in 2026 reached fewer than 38,690 patrons in a year, and half reached more. A smaller number of respondents reporting a much higher number can skew the average number higher, and that’s the case here, with one-fifth of respondents (20%) reporting that they serve at least 300,000 people on an annual basis. However, well over half of respondents (53.7%) in 2026 actually reach 50,000 or fewer people annually—and nearly half of those (48.6%, or 26.1% of all park respond ents) said they reach 10,000 or less. Another 12.1% of park respondents said that their annual reach is 50,000 to 100,000 people, while 20.9% reach 100,000 to 200,000, and 13% reach 200,000 to 300,000.

ents) said they reach 10,000 or less. Another 12.1% of park respondents said that their annual reach is 50,000 to 100,000 people, while 20.9% reach 100,000 to 200,000, and 13% reach 200,000 to 300,000.

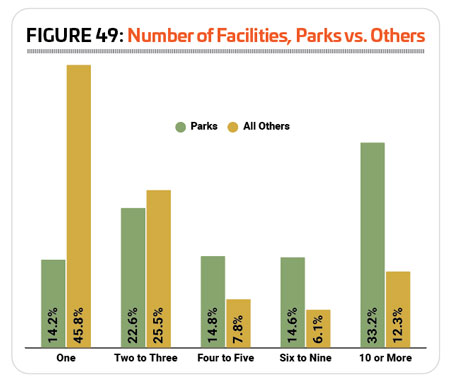

On average, park respondents manage 10.8 separate facilities, down from 13.1 in 2025, but still above the average of 9.4 reported in 2024. Around one-third (33.2%) of park respondents said they manage 10 or more facilities, up slightly from 31.3% in 2025. This compares with just 12.3% of non-park respondents who manage at least 10 facilities. On the other hand, while 45.8% of non-park respondents in 2026 said they manage just a single facility, just 14.8% of park respondents had just a single facility to manage. Another 22.6% of park respondents said they manage two or three facilities, while 14.8% manage four or five. The remaining 14.6% of park respondents said they manage between six and nine facilities. (See Figure 49.)

Park respondents were by far the most likely to report that they reach an all-ages audience with their facilities, programs and services. Some 60.6% of park respondents reach all ages, compared with just 34% of non-park respondents. Another 23% of park respondents said they primarily reach children ages 4 to 12, compared with 11.7% of non-park respondents. Some 12.5% of park respondents primari ly reach adults, with much smaller numbers primarily working with teens (1.8%), seniors (1.2%), or infants and toddlers (0.6%).

ly reach adults, with much smaller numbers primarily working with teens (1.8%), seniors (1.2%), or infants and toddlers (0.6%).

Park respondents are among the most likely to report that they partner with other organizations. Such partnerships can be helpful to expand an organization’s reach, programming opportunities, outreach and more. Some 93% of park respondents said they had formed such partnerships, compared with 84.3% of non-park organizations.

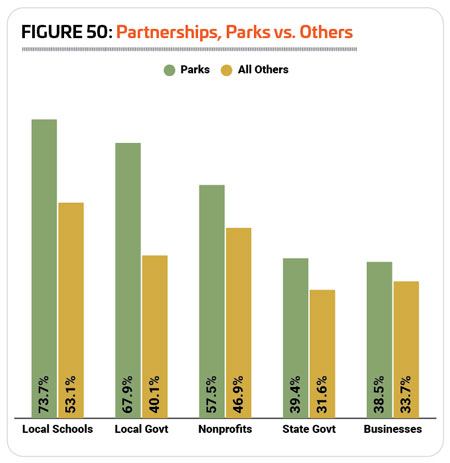

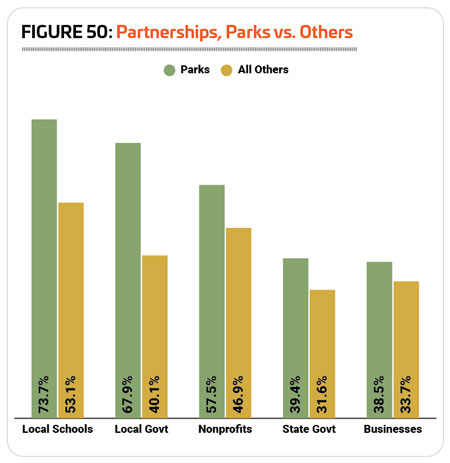

The most common partners for parks were local schools, with 73.7% of park respondents indicating they had partnered with them, up from 71% in 2025. This compares with 53.1% of non-park respondents who had partnered with local schools. More than two-thirds (67.9%) of park respondents said they had partnered with local government, compared with 40.1% of non-park respondents. The next most common partners for parks were nonprofits (57.5% vs. 46.9% of non-park respondents), state government (39.4% vs. 31.6%), and corporations and local businesses (38.5% vs. 33.7%). (See Figure 50.)

Parks were also more likely than others to partner with the federal government (21.4% vs. 17.4%).

Park Costs &  Revenues

Revenues

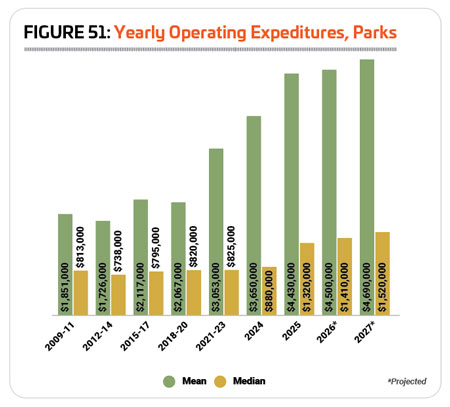

In the decade between 2010 and 2020, median spending for parks stayed relatively constant, increasing by just 0.9% from an average of $813,000 for 2009-11 to $820,000 for 2018-20. At the same time, however, the mean increased by 11.7%, from

$1.851 million to $2.067 million. This trend is even more exaggerated when comparing 2018-20 to 2024, where

the mean increases by 76.6% as the survey instrument changed to account for even higher levels of spending, driving the mean even higher, from $2.067 million to $3.65 million. At the same time, the median increased by just 7.3%, from $820,000 to $880,000.

From 2024 to 2025, this trend is reversed, with the median increasing at a faster clip than the mean. Mean operating costs in 2024 were $3.65 million, and rose 21.4% to $4.43 million in 2025. At the same time, median operating costs rose 50%, from $880,000 to $1.32 million. This can indicate that more respondents are reporting increasing spending over this time, rather than being driven by a small number of very high values. In other words, the spenders in the middle are increasing their spending faster than the spenders at the top.

Respondents projected a similar trend looking forward, with the mean expected to rise 5.9% from $4.43 million in 2025 to $4.69 million in 2027, and the median expected to increase 15.2%, from $1.32 million to $1.52 million. (See Figure 51.)

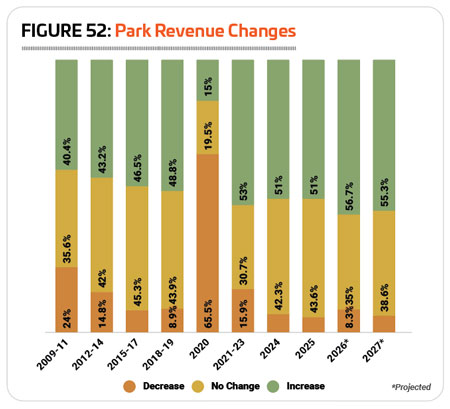

When it comes to revenues, park respondents have become increasingly more likely to report increases over time, with the unsurprising exception of the year 2020, when COVID had a dramatic impact. Looking at the data, you can see the impact of the Great Recession on the numbers reported for 2009 to 2011, with respondents in that time frame being more likely than usual to report that their revenues had decreased. Nearly a quarter (24%) of respondents in 2009-11 reported that their revenues had declined. But in the following years, the numbers reporting such decreases fell, from 14.8% in 2012-14 to 8.9% in 2018-19. Obviously, 2020 saw that number spike, but then in the following years, as the effect of the pandemic has receded, respondents are less likely than ever to report decreases, and in fact 2025 saw the lowest number of park respondents reporting a decrease since we started collecting data—just 5.4%.

At the same time, respondents have grown more likely over time to report that their revenues are increasing year-over-year. In 2009-11, 40.4% of park respondents reported that their revenues increased, and by 2018-19, nearly half (48.8%) were seeing increases. Following the pandemic, that number has increased further, with 53% of respondents reporting increases for 2021-23, and 51% reporting an increase in both 2024 and in 2025. (See Figure 52.)

At the same time, respondents have grown more likely over time to report that their revenues are increasing year-over-year. In 2009-11, 40.4% of park respondents reported that their revenues increased, and by 2018-19, nearly half (48.8%) were seeing increases. Following the pandemic, that number has increased further, with 53% of respondents reporting increases for 2021-23, and 51% reporting an increase in both 2024 and in 2025. (See Figure 52.)

Looking forward, park respondents expect this trend to continue, with 56.7% expecting an increase in 2026 and 55.3% expecting an increase in 2027.

On average, park respondents in 2026 said that they recover 42.8% of their operating expenses via revenues, virtually no change from 2025 (43.1%), but still below the 51.6% recovered by respondents in 2024. Well over a third of park respondents (36.9%) said they recover 30% or less of their costs via revenues, compared with 19.2% of non-park respondents. And about half as many park respondents (18.5%) said they recover more than 70% of their operating costs via revenues, compared with 40.5% of non-park respondents.

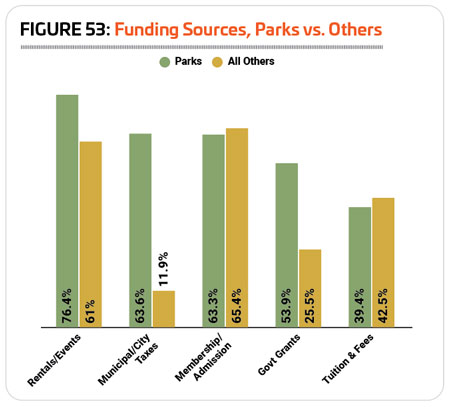

Facility rentals and private events continued to be the most common source of funding for park respondents, with more than three-quarters (76.4%) indicating this is a source of funding. This compares with 61% of non-park respondents. The next most common source of funding for parks in 2026 was municipal and city taxes, with 63.6% of park respondents indicating they receive funding this way, compared with just 11.9% of non-park respondents. Membership and admission fees followed close behind as a funding source, with 63.3% of parks and 65.4% of non-park respondents indicating they received funding through these kinds of fees. (See Figure 53.)

Facility rentals and private events continued to be the most common source of funding for park respondents, with more than three-quarters (76.4%) indicating this is a source of funding. This compares with 61% of non-park respondents. The next most common source of funding for parks in 2026 was municipal and city taxes, with 63.6% of park respondents indicating they receive funding this way, compared with just 11.9% of non-park respondents. Membership and admission fees followed close behind as a funding source, with 63.3% of parks and 65.4% of non-park respondents indicating they received funding through these kinds of fees. (See Figure 53.)

In addition to events and rentals, and municipal taxes, park respondents were more likely than others to indicate that they received funding through government grants (53.9% of park respondents vs. 25.5% of non-park respondents), concessions (34.4% vs. 20.8%), district taxes (12.1% vs. 6.3%) and state taxes (9.4% vs. 5.8%).

More than three-quarters of park respondents (78.6%) said that they had taken action in the past few years to reduce their operating costs, down from 80.1% in 2025. This compares with 82.3% of non-park respondents in 2026 who had taken action to reduce their costs.

The most common methods park respondents used to reduce their costs included: fee increases (56.6% of park respondents had increased fees, up from 53.8% in 2025); improving energy efficiency (31.9%, down from 35%); putting construction or renovation plans on hold (31.5%, up from 30.3%); reducing staff (25.1%, up from 22.3%), and cutting programs or services (18%, virtually unchanged from 17.9%).

Park Facility Use, Amenities & Construction

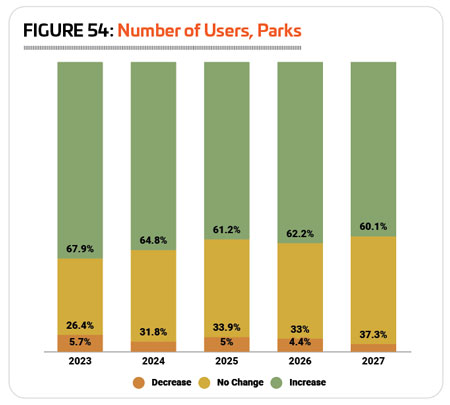

Slightly fewer park respondents saw increasing numbers of people using their facilities in 2025 than in 2024 and 2023. In 2025, 61.2% of park respondents said the number of people using their facilities had risen, down from 64.8% in 2024 and 67.9% in 2023. Another 33.9% of park respondents said there was no change to the number of people using their facilities in 2025, and just 5% reported a decrease. (See Figure 54.)

Looking forward, park respondents expect a similar picture to play out over the next couple of years, with 62.2% expecting usage of their facilities to increase in 2026 and 60.1% expecting an increase in 2027. Very few respondents are anticipating declining usage of their facilities in 2026 (4.4%) and 2027 (2.6%).

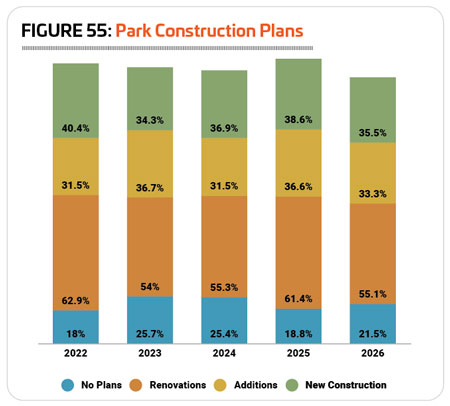

More than three-quarters of respondents from parks (78.5%) in 2026 said they have plans for construction over the next few years. This is down slightly from 2025, when 81.2% of park respondents were planning construction, but higher than the number reported for 2024 (74.6%). (See Figure 55.)

Park respondents were most likely to be planning renovations to their existing facilities, with 55.1% of park respondents indicating they would be pursuing renovations, down from 61.4% in 2025. Another 35.5% of park respondents were planning to build new facilities, down from 38.6% in 2025; and 33.3% were planning additions to their existing facilities, down from 36.6%.

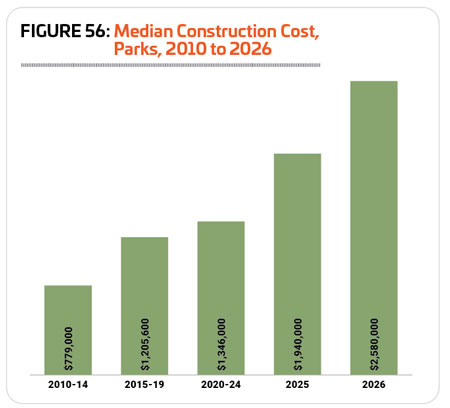

The median cost for construction spending on park facilities in 2026 was $2.58 million, a 33% increase over 2025’s median of $1.94 million. Since 2010-14, median spending on park facility construction has increased 231.2%, from $779,000. (See Figure 56.)

When it comes to outfitting park facilities, a wide range of features and amenities can be used to meet the diverse needs of a community, from sports and fitness to relaxation and more. The most common features found in park respondents’ facilities in 2026 include: playgrounds (84.9% of park respondents had playgrounds, down from 86.7% in 2025); park shelters, gazebos, etc. (84.4%, up from 83.1%); park restroom structures (81.9%, down from 82.7%); outdoor courts for sports like basketball, tennis or pickleball (74.5%, down from 75.3%); open spaces like gardens and natural areas (74%, down from 77.2%); walking and hiking trails (71.4%, down from 73.6%); natural turf sports fields (69.6%, up from 70.7%); bleachers and seating (68.4%, virtually unchanged from 68.6%); concessions (62.5%, up from 57%); and classrooms and meeting rooms (61.5%, up from 58.4%).

Respondents were the cohort second most likely to have plans to add features at their facilities over the next few years, after camp respondents. Some 43.3% of park respondents in 2026 said they were planning to add features at their facilities, virtually unchanged from 44% in 2025. This compares with 24.9% of non-park respondents who have plans to add features and amenities at their facilities.

The amenities that park respondents in 2026 are most likely to be planning to add over the next few years include:

1. Splash play areas (planned by 26% of park respondents who will be adding features)

2. Playgrounds (24.9%)

3. Park shelters (19.8%)

4. Walking and hiking trails (18.6%)

5. Park restroom structures (18.1%)

6. Outdoor fitness equipment or fitness trails (17.5%)

7. Synthetic turf sports fields (16.4%)

8. Dog parks (15.8%)

9. Bike trails (15.3%)

10. Outdoor sports courts (14.1%)

Park Programming

Just about all park respondents—98.7%—said that they provide programming at their facilities, virtually the same as in 2025 (99%) and 2024 (98.7%). This compares with 95.8% of non-park respondents.

The most commonly offered program types for park respondents in 2026 include: holiday events and other special events (83.7% of park respondents host such events, up from 81% in 2025); youth sports (69%, virtually unchanged from 68.9%); group exercise (63.9%, up from 60%); arts and crafts (63.3%, down from 64.3%); day camps and summer camps (63%, down from 66.6%); educational programs (60.2%, down from 62.8%); programs for active older adults (58.6%, down from 61.5%); mind-body balance programs such as yoga and tai chi (57.7%); adult sports (55.2%, up from 54.2%); and fitness programs (54.5%, up from 52.2%).

Park respondents were more likely than others to report that they were planning to make additions to their program lineup over the next several years. Some 28.9% of park respondents in 2026 said they had such plans, down from 32.3% in 2025. This compares with 22.7% of non-park respondents.

The programs park respondents are most likely to be planning to add over the next few years include:

1. Teen programs (up from No. 3 in 2025)

1. Teen programs (up from No. 3 in 2025)

2. Educational programs (up from No. 7)

3. Programs for people with disabilities (up from No. 17)

4. Environmental education (down from No. 2)

5. Arts and crafts (up from No. 14)

6. Performing arts programs (up from No. 13)

7. Group exercise programs (down from No. 5)

8. Day camps and summer camps (up from No. 11)

9. Adult sports (down from No. 8)

10. Adaptive sports (up from No. 19)

Outreach & Impact

From wellness and conservation initiatives to outreach programs for disadvantaged community members and beyond, park respondents reach far beyond the borders of their parks, rec centers, sports fields and other spaces to have an impact on the communities they serve. The Industry Report survey asks respondents to register their involvement in a variety of initiatives, and as usual, park respondents in 2026 were more likely to select a number of different initiatives. Some 86.6% of park respondents were involved in at least one of the initiatives covered by the survey, compared with 77.7% of all other respondents.

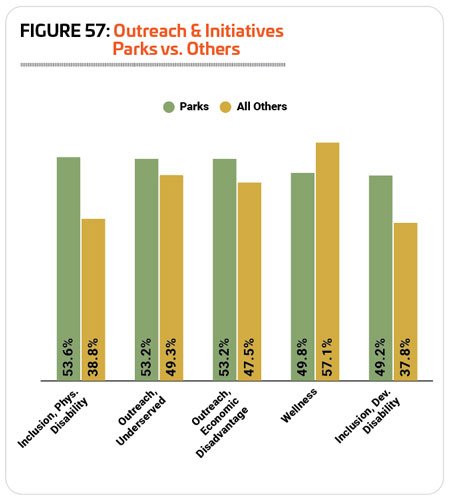

Park respondents were most likely to be working on inclusion initiatives for individuals with physical disabilities, with 53.6% of park respondents indicating they were involved in this kind of outreach. This compares with 38.8% of non-park respondents. The other types of initiatives that park respondents were most likely to be involved in include: outreach to underserved populations (53.2% vs. 49.3%); outreach to economically disadvantaged populations (53.2% vs. 47.5%); wellness initiatives (49.8% vs. 57.1%, one of the few initiatives that park respondents were less likely to be involved with than their peers in other cohorts); and inclusion initiatives for individuals with developmental disabilities (49.2% vs. 37.8%). (See Figure 57.)

Other initiatives that park respondents were more likely than other cohorts to take up include: resource conservation and green initiatives (37.3% of park respondents vs. 18.7% of all others); programs to connect people with nature (36.9% vs. 21.7%); wildlife conservation (16.6% vs. 6.2%); community or regional disaster recovery assistance (16.3% vs. 8.5%); climate resilience initiatives (10.5% vs. 5.5%); and wildfire prevention (9.8% vs. 5.5%).

When asked what factor has had the greatest impact on park facilities and programming over the past 20 years, budgetary pressures held the No. 1 position, with 60.2% of park respondents indicating this was a top influence on their facilities and programs. This compares with 50.9% of non-park respondents. More than half of park respondents (54%) also named aging equipment and infrastructure as a major influence, compared with 47.2% of non-park respondents. Economic and inflation-related challenges were named as an influence by 24.6% of park respondents (compared with 30.6% of non-park respondents), while 23.2% said increasing participation and a growing number of visitors was a major influence (vs. 21.5% of non-park respondents).

Park respondents were also more likely than non-park respondents to point to political challenges (17% vs. 10.3%), visitor expectations and demands (14.9% vs. 11.7%), inclusion and accessibility (12.8% vs. 9%), and sustainability and resource conservation (8.3% vs. 4.6%) as major influences on their facilities and programs over the past 20 years. RM