In these pages, we’ll take a closer look at the response from professionals working for health, sports and fitness clubs, racquet clubs and medical fitness facilities. These respondents comprised 4.6% of the survey population in 2026, virtually unchanged from 4.3% in 2025.

In 2026, the largest number of health club respondents—one-third (33.3%)—were from the South Central region. The next largest group—26.7%—was from the Midwest. Smaller numbers of health club respondents were located in the Northeast (16.7%) and South Atlantic (13.3%) regions, and the smallest number of health club respondents (10%) were from the West.

Half of health club respondents (50%) said they were located in suburban communities. Another 26.7% were from urban areas, and 23.3% said they were located in rural communities.

Health club respondents are the only cohort of survey respondents who are most likely to work with private, for-profit organizations. Some 63.8% of health club respondents said they were with for-profit facilities, compared with just 10.9% of all other respondents. Another 27.7% of health club respondents said they worked with nonprofit organizations, and just 8.5% said they worked for public or governmental organizations.

On average, health club respondents in 2026 said they manage 3.8 individual facilities, representing no change from 2025. Some 60.9% of health club respondents said manage just a single facility, compared with 32% of non-health-club respondents. On the other end of the spectrum, just 8.7% of health club respondents have 10 or more facilities to manage, compared with 21.3% of non-health-club respondents. The remaining 30.4% of health club respondents manage between two and nine individual facilities.

Health club respondents were much less likely than others to report that they had partnered with other organizations, though more than three-quarters (78%)—had done so. This is up from 64.4% in 2025 and compares with 88.3% of non-health-club respondents.

The most common partners for health club respondents in 2026 were: corporations and local business (39% of health club respondents had partnered with businesses, up from 31.1% in 2025); healthcare or medical facilities (36.6% vs. 26.7%); local schools (34.1% vs. 26.7%); nonprofit organizations (26.8% vs. 22.2%), and military as well as other private health clubs (19.5%, compared to 15.6% and 4.4%, respectively).

On average, health club respondents reached an average of 73,630 patrons annually, but because the sample size is small, this number is somewhat distorted. The median number of patrons health club respondents reach annually is just 6,870 (meaning half of respondents have fewer than 6,870 annual patrons, and half have more).

Some 61.4% of health club respondents said they reach 10,000 or fewer people a year, while another 18.2% reach between 10,000 and 50,000. Just 6.8% said that they reach 50,000 to 100,000 people a year, while 13.6% said they serve more than 100,000 patrons on an annual basis.

Health club respondents were much more likely than others to report that their facilities’ primary audience was made up of adults. Some 59.1% of health club respondents said they primarily serve adults, compared with 15.9% of non-health-club respondents. Another 34.1% said they primarily reach all ages, and 6.8% said their primary audience was made up of seniors 65 and older.

Health Club Costs & Revenues

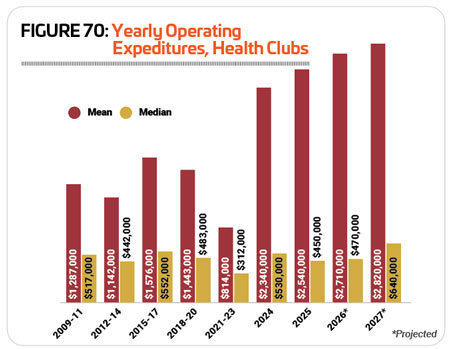

From 2010 to 2020, the average operating budget for health club facilities increased by 12.1%, from $1.287 million in 2009-11 to $1.443 million in 2018-20, while the median actually fell 6.6%, from $517,000 to $483,000, in the same time frame. This means that while the highest spenders were gradually spending more, the number of respondents spending lower amounts increased by a larger amount.

From 2010 to 2020, the average operating budget for health club facilities increased by 12.1%, from $1.287 million in 2009-11 to $1.443 million in 2018-20, while the median actually fell 6.6%, from $517,000 to $483,000, in the same time frame. This means that while the highest spenders were gradually spending more, the number of respondents spending lower amounts increased by a larger amount.

The change in the average between 2018-20 and 2024 reflects an adjustment in the survey instrument to allow for higher reported amounts. This led the mean to jump 62.2% from $1.443 in 2018-20 to $2.34 million in 2024. This makes the median—the exact middle of the spread, with half of respondents spending more and half spending less—more reflective of the actual increase in spending for most respondents. Median spending increased 9.7% from $483,000 in 2018-20 to $530,000 in 2024.

From 2024 to 2025, average operating costs for health club respondents increased 8.5%, from $2.34 million to $2.54 million. At the same time, however, median spending fell by 15.1%, from $530,000 to $450,000, again reflecting a small concentration of respondents spending much higher amounts, while the majority of respondents are undertaking projects that are far less costly.

Looking forward, health club respondents are expecting their operating costs to increase by 11% over the next couple of years, from $2.54 million in 2025 to $2.82 million in 2027. Here, the median cost increases at a much faster rate of 42.2%, from $450,000 to $640,000. This means the larger number of respondents with lower operating costs expect to spend more. (See Figure 70.)

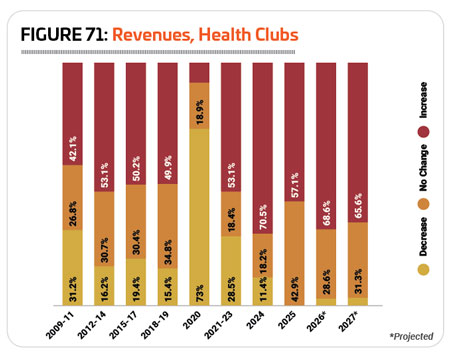

In the years leading up to 2020, around half of health club respondents were reporting that their revenues were increasing year over year, with 53.1% reporting an increase in 2012-14, 50.2% reporting an increase in 2015-17 and 49.9% reporting an increase in 2018-19. (See Figure 71.)

In the years leading up to 2020, around half of health club respondents were reporting that their revenues were increasing year over year, with 53.1% reporting an increase in 2012-14, 50.2% reporting an increase in 2015-17 and 49.9% reporting an increase in 2018-19. (See Figure 71.)

2020 obviously presented a challenge for health club respondents, and 73% of respondents reported that their revenues fell in that time. The instability continued into 2021-23, but in 2024, the highest number of health club respondents in 20 years, 70.5%, reported that their revenues had increased year over year, and in 2025, not a single health club respondent reported a decrease in revenues, while 57.1% reported an increase and 42.9% reported no change.

Looking forward, health club respondents continue to be relatively optimistic about 2026 and 2027, with around two-thirds anticipating their revenues to increase in 2026 (68.6%) and 2027 (65.6%).

On average, health club respondents in 2026 said they earn back 66.6% of their operating costs via revenues, down from 71.5% in 2025. Half (50%) of health club respondents said they earn back more than 70% of their costs via revenues, compared with 32.2% of non-health-club respondents. And 37.5% of health club respondents said they earn back more than 90% of their costs via revenues, versus 18.6% of non-health-club respondents. At the other end of the spectrum, 18.8% of health club respondents earn back 30% or less of their costs via revenues, compared with 26.8% of non-health-club respondents.

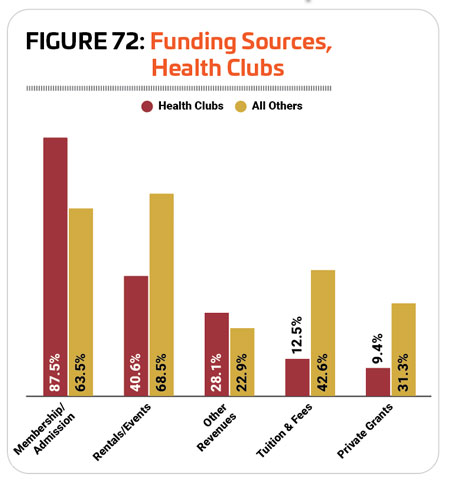

When it comes to supporting their operations, health clubs are the most likely to receive funding through membership and admission fees. Some 87.5% of health club respondents said their facilities were funded through membership and admission fees, compared with 63.5% of non-health-club respondents. The next most common sources of funding for health clubs were rentals and private events (40.6% of health club respondents funded their facilities this way), other revenues (28.1%), tuition and fees (12.5%) and private grants (9.4%). (See Figure 72.)

When it comes to supporting their operations, health clubs are the most likely to receive funding through membership and admission fees. Some 87.5% of health club respondents said their facilities were funded through membership and admission fees, compared with 63.5% of non-health-club respondents. The next most common sources of funding for health clubs were rentals and private events (40.6% of health club respondents funded their facilities this way), other revenues (28.1%), tuition and fees (12.5%) and private grants (9.4%). (See Figure 72.)

Health club respondents have been much more likely to report that they’ve taken action to reduce their facilities’ operating costs over the past couple of years. In 2026, 81.3% of health club respondents said they had done so, down just slightly from 82.9%. In 2024, 69.7% of health club respondents said they had acted to reduce costs.

Health club respondents in 2026 were most likely to say that they had increased their fees. Some 46.9% of health club respondents had increased their fees, down from 2025 when 61% had increased fees. Nearly a third (31.3%) said they had reduced staff or improved energy efficiency at their facilities, down from 39%. Another quarter (25%) said they had cut programs or services, up from 12.2%. And 18.8% said they had put construction plans on hold, down only slightly from 19.5% in 2025.

Health Club Facility Use, Amenities & Construction

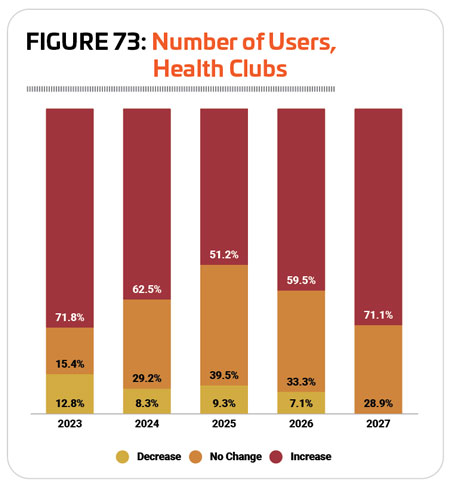

Slightly fewer health club respondents reported that the number of people using their facilities increased in 2025 (51.2%) than in 2024 (62.5%). Another 39.5% of respondents said that this number remained the same in 2025 (compared with 29.2% reporting no change in 2024), while 9.3% reported a decrease. (See Figure 73.)

Slightly fewer health club respondents reported that the number of people using their facilities increased in 2025 (51.2%) than in 2024 (62.5%). Another 39.5% of respondents said that this number remained the same in 2025 (compared with 29.2% reporting no change in 2024), while 9.3% reported a decrease. (See Figure 73.)

In 2026, health club respondents were most likely to be expecting traffic to increase (59.5%) or stay the same (33.3%). Just 7.1% of health club respondents are expecting the number of people using their facilities to decrease in 2026. And looking forward to 2027, health club respondents are even more optimistic, with 71.1% projecting use of their facilities to increase and 28.9% expecting no change.

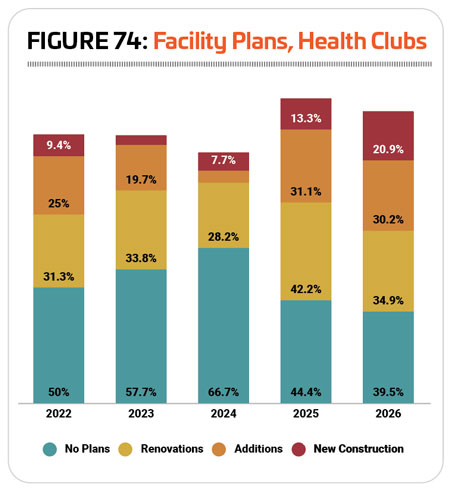

More health club respondents reported in 2026 that they were planning construction of some kind over the next few years than in any year since 2018, when 66.7% reported that they had construction plans. Some 60.5% of health club respondents in 2026 have such plans, up from 55.6% in 2024.

Around one-fifth (20.9%) of health club respondents in 2026 said they were planning to build new facilities, up from 13.3% in 2025—the highest number of health club respondents to report that they were planning to build new facilities since 2014 (25.9%). Another 30.2% of health club respondents in 2026 were planning additions to their existing facilities, down slightly from 31.1% in 2025. And 34.9% said they were planning renovations, down from 42.2%. (See Figure 74.)

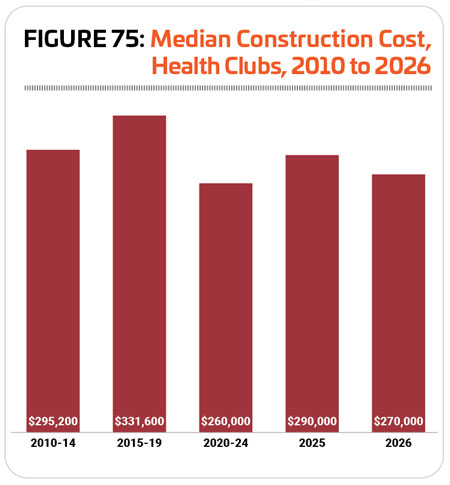

The median cost for construction spending on health club facilities in 2026 was $270,000, a 6.9% decrease from 2025’s median of $290,000. Unlike most other facility types, health club respondents have been increasingly likely to spend less on their construction plans over time rather than more. Median spending on health club facility construction has fallen 8.5% since 2010-14, when the median spending was $295,200. (See Figure 75.)

The median cost for construction spending on health club facilities in 2026 was $270,000, a 6.9% decrease from 2025’s median of $290,000. Unlike most other facility types, health club respondents have been increasingly likely to spend less on their construction plans over time rather than more. Median spending on health club facility construction has fallen 8.5% since 2010-14, when the median spending was $295,200. (See Figure 75.)

It’s not hard to imagine what kinds of amenities would most likely feature in health club respondents’ facilities. One would expect fitness equipment and exercise rooms, locker rooms and courts for racquet and other sports to be common. And this is indeed the case, as the most common features found in health club respondents’ facilities in 2026 include: fitness centers with weights and cardio equipment (95.7% of health club respondents had fitness centers, up from 90.9% in 2025); exercise studio rooms for aerobics, yoga and similar types of classes (82.6%, up from 81.8%); locker rooms (73.9%, down slightly from 76.4%); Wi-Fi services (60.9%, down from 67.3%); indoor courts for sports like basketball, volleyball or racquet sports (37%, down from 40%); indoor aquatic facilities (37%; down from 41.8%); childcare centers (32.6%, down from 34.5%); indoor tracks for walking or running (30.4%, up from 23.6%); concessions (17.4%, down from 43.6%); and outdoor courts for sports like basketball, tennis or pickleball (15.2%, down from 23.6%).

Health club respondents in 2026 were among the least likely to report that they had plans to add features or amenities at their facilities over the next few years, second to school respondents. Some 19.1% of health club respondents said they had plans to make such additions, up from 14.9% in 2025. This compares with 32.9% of non-health-club respondents in 2026 who have plans to add features to their facilities.

The amenities that health club respondents are most likely to be planning to add over the next few years include:

The amenities that health club respondents are most likely to be planning to add over the next few years include:

1. Outdoor sports courts (33.3%)

2. Playgrounds (22.2%)

3. Outdoor fitness equipment (22.2%)

4. Natural turf sports fields (22.2%)

5. Classrooms and meeting rooms (22.2%)

6. Indoor sports courts (22.2%)

7. Wi-Fi services (22.2%)

8. Indoor tracks (22.2%)

9. Locker rooms (22.2%)

10. Challenge course and ropes courses (22.2%)

Health Club Programming

While plenty of health club visitors and members are content to get a workout using a combination of cardio machines, weight machines, free weights and mats, programming can be an even greater draw, allowing members not just to get fit but to socialize as well. Great programming can also be a great marketing tool, getting potential members in the door and keeping existing members coming back for more. So it comes as no surprise that 100% of health club respondents in 2026 said they provide programming at their facilities, unchanged from 2025.

The most commonly offered program types for health club respondents in 2026 include: fitness programs (92.5% of health club respondents offer formal fitness programs covering cardio, strength training and more, up from 91.1% in 2025); group exercise programs (92.5%, up from 80%); functional fitness programs (85%, up from 82.2%); personal training (80%, up from 75.6%); mind-body balance programs like yoga and tai chi (70%, down from 75.6%); nutrition and diet counseling (55%, virtually unchanged from 55.6%); programs for active older adults (50%, down from 53.3%); aquatic exercise programs (37.5%, up from 33.3%); and holiday events and other special events (37.5%, down from 44.4%).

In 2026, health club respondents were among those most likely to report that they are planning to add programming at their facilities within the next few years. Some 34% of health club respondents said they had such plans, compared with 24.8% of non-health-club respondents. This is up over the past few years, as 27.9% of health club respondents in 2025, and 25% in 2024 had plans to expand their program lineup.

The programs health club respondents are most likely to be planning to add over the next few years include:

1. Nutrition and diet counseling (no change from 2025)

2. Holiday events and other special events (up from No. 15 in 2025)

3. Educational programs (up from No. 11)

4. Youth sports (up from No. 5)

5. Mind-body balance programs like yoga (no health club respondents planned to add mind-body programs in 2025)

6. Programs for active older adults (up from No. 16)

7. Sports tournaments and races (up from No. 17)

8. Personal training (up from No. 18)

9. Fitness programs (up from No. 12)

10. Functional fitness programs (no health club respondents planned to add functional fitness in 2025)

Industry Challenges & Influences

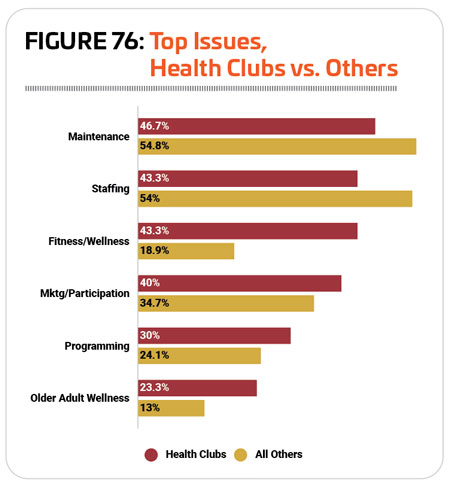

When asked about the top challenges for their facilities, health club respondents differed somewhat from the rest of the respondents. While they were still most likely to name equipment and facility maintenance as their top two issues, with 46.7% and 43.3% of health club respondents, respectively, they were somewhat less likely than other respondents to name these as their top challenges, as 54.8% of non-health-club respondents called equipment and facility maintenance and 54% named staffing issues as a top challenge.

Tied with staffing challenges, general fitness and wellness was much more likely to be named as a top challenge by health club respondents than by non-health-club respondents. Some 43.3% of health club respondents aid that general fitness and wellness was a top issue for their facilities, compared with just 18.9% of non-health-club respondents.

Health club respondents were also more likely than non-health-club respondents to cite marketing and increasing participation (40% vs. 34.7%), coming up with new and innovative programming (30% vs 24.1%) and older adult fitness and wellness (23.3% vs. 13%) as top challenges at their facilities. (See Figure 76.)

Health clubs also responded differently from most respondents when asked about the factors that have had the greatest influence or impact on their facilities and programming over the past 20 years. While most respondents named budgetary pressure as the No. 1 influence, for health club respondents aging equipment and infrastructure, increasing participation, and difficulty finding and retaining employees all ranked higher. Some 57.1% of health club respondents said aging equipment and infrastructure was the top influence on their facilities over the past 20 years, compared with 49.7% of non-health-club respondents. Another 28.8% of health club respondents named increasing participation and a growing number of users as a top influence (vs. 21.9% of non-health-club respondents), while 28.8% said difficulty finding and retaining employees was a top influence (vs. 21.9%). Budgetary pressures, as well as inflation-related challenges were the next most commonly cited influence on health club facilities, though they were much less likely than others to name them as such, with 21.4% of health club respondents naming budgetary pressures and 21.4% naming inflation as top influences, compared with 56.1% and 28.4% of non-health-club respondents, respectively. RM