A Look at What's Happening in Recreation, Sports & Fitness Facilities

Survey Methodology

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

This report is based on a survey conducted for Recreation Management by Signet Research Inc., an independent research company. An email was broadcast and respondents were invited to participate. From the launch of the survey on Jan. 17, 2020, to the closing of the survey on Feb. 3, 2020, 1,307 returns were received. The findings of this survey may be accepted as accurate, at a 95 percent confidence level, within a sampling tolerance of approximately +/- 2.7 percent.

A follow-up survey was conducted independently to gather clarifying information in light of the COVID-19 epidemic. From the launch of the survey on May 1, 2020, to the closing of the survey on May 11, 2020, 576 returns were received.

For the past 14 years, we've been keeping track of the trends in recreation, sports and fitness facilities via our State of the Industry Report. We've logged the various ways facilities were affected by—and recovered from—the Great Recession. The results from the 2020 Industry Report Survey, taken in early 2020, largely show continuing growth and strength in the entire industry.

In these pages, we provide a detailed look at the responses collected via our annual 50-question survey. We'll give you a look into how things stood as of January 2020, with detailed responses on such topics as management, operations, construction, programming and more for facilities of all kinds, with detailed information for aquatic facilities, parks and recreation, colleges, schools, Ys and health clubs.

But of course, things can change quickly, and the world of June 2020 is not at all the same as the world of January 2020. Recognizing this, we took a survey of readers in early May 2020, to learn more about the impact of COVID-19-related directives on their revenues and their expected timeline for reopening, as well as what actions they had taken, both to mitigate the impact (such as furloughs and closing facilities) as well as to reach the community with needed resources (such as by providing child care for health care staff, or getting involved in programs to address food insecurity). You'll find that information in the pages to come, but for quick reference, information on the impact on revenues is on page 16, data regarding a timeline for reopening appears on page 31, and you'll find more data about actions facilities have taken in light of the pandemic beginning on page 32.

About the Respondents

Before we get to any updated details, though, let's begin with a general summary of the results of the initial survey. Here, we'll report the results from the initial survey population of 1,307 respondents, adding clarifying information where relevant. After this section, we'll examine more detailed information based on the facility type of the respondents. This begins with a deeper look at responses from respondents whose facilities include aquatic elements. After that, we dive into the responses from the largest facility-type cohorts in the survey population. This includes parks and recreation organizations, colleges and universities, schools and school districts, health clubs, and Ys, JCCs and Boys & Girls Clubs.

It's a lot of data, but if you need more, head over to the RecManagement.com website, and you'll find further discussion of responses from camp facilities and community centers. And, as always, we bring you a weekly dose of research in the Rec Report newsletter, highlighting a different data point every week. (Is there something you'd like to know? Shoot us a message at [email protected], and we'll see if we can find the answer in the data.)

Finally, don't forget to stay tuned next month, when we'll report in our annual Salary Survey on the career and salary trends of these respondents.

The Respondents: A Profile

First off, let's take a look at who the respondents to the Industry Report Survey are, from their roles in their organizations to where they're located and more.

As always, survey respondents serve various functions and in a variety of roles within their organizations, with a majority working in higher-level positions. More than one-third (35.2%) said their job title was "director." More than one-fifth (20.3%) are in administration and management positions, such as administrator, manager or superintendent. Another 16.1% work in operations and facility management, with titles including operations manager, facility manager, building manager or supervisor. Some 11.8% of respondents are in program and activity administration roles, such as activity or program director, manager, coordinator, specialist, coach and instructor. Some 8.2% of respondents said they are either the chairman, CEO, president, vice president or owner of their organization. Another 1.2% are faculty or teachers, while 0.5% are in services such as planners, designers, architects and consultants. Finally, 6.8% of respondents said they hold "other" titles in their organization.

Considering so many respondents hold high-level positions in the recreation, sports and fitness industry, it is not at all surprising that they have a lot of experience under their belts, both in their current positions, as well as in the industry. On average, respondents have been in their current jobs for 11.7 years (up from an average of 10.8 in 2019), and have an average of 22.3 years of experience in the recreation, sports and fitness industry (up from 21.2).

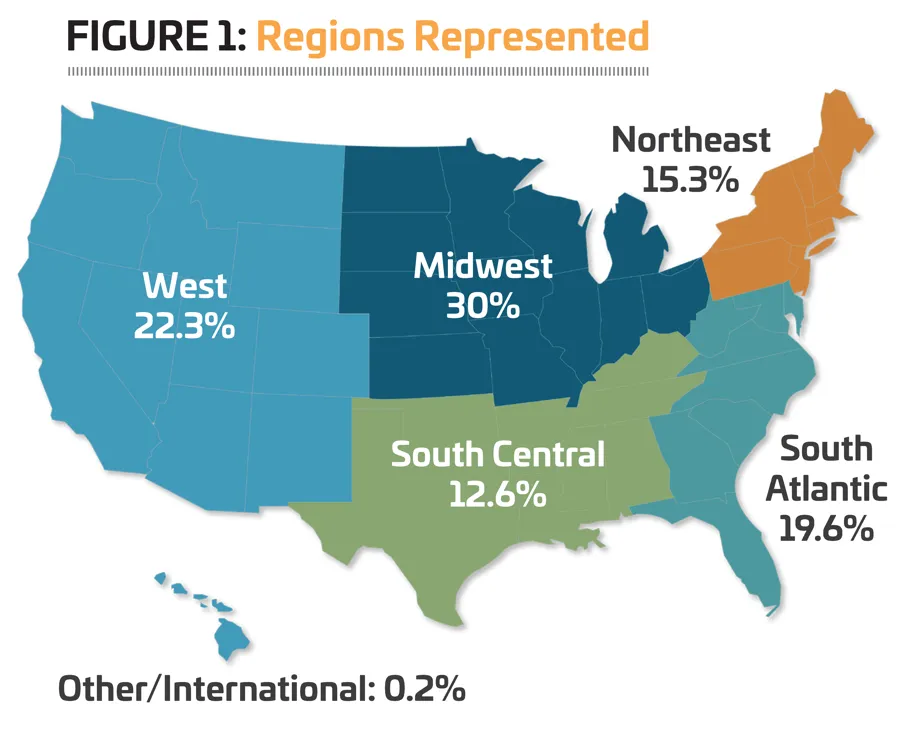

The largest number of respondents in 2020 were from the Midwest, with 30% of respondents indicating they were from Illinois, Indiana, Iowa, Kansas, Michigan, Minnesota, Missouri, Nebraska, North Dakota, Ohio, South Dakota or Wisconsin. (See Figure 1.)

The second largest region, in terms of survey representation, was the West, with 22.3%. This includes Alaska, Arizona, California, Colorado, Hawaii, Idaho, Montana, Nevada, New Mexico, Oregon, Utah, Washington and Wyoming.

The South Atlantic is home to 19.6% of survey respondents. This includes Delaware, Florida, Georgia, Maryland, North Carolina, South Carolina, Virginia, Washington, D.C., and West Virginia.

Some 15.3% of respondents said they were from the Northeast, including the states of Connecticut, Maine, Massachusetts, New Hampshire, New Jersey, New York, Pennsylvania, Rhode Island and Vermont.

Some 12.6% of respondents said they were from the South Central region, which includes Alabama, Arkansas, Kentucky, Louisiana, Mississippi, Oklahoma, Tennessee and Texas.

Finally, just 0.2% of survey respondents said they were from outside the United States.

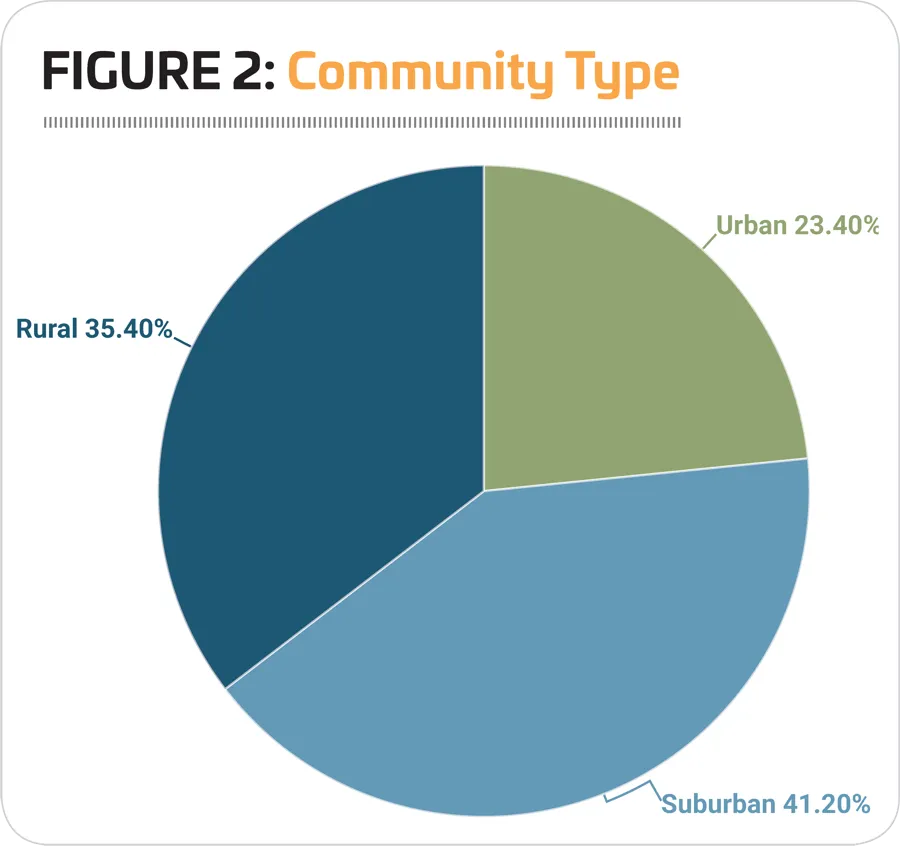

Similar to past years' surveys, the largest percentage of respondents in 2020 said they were from suburban communities. Some 41.2% of respondents call the suburbs home. More than one-third (35.4%) said they were from rural areas, and another 23.4% were from urban communities. (See Figure 2.)

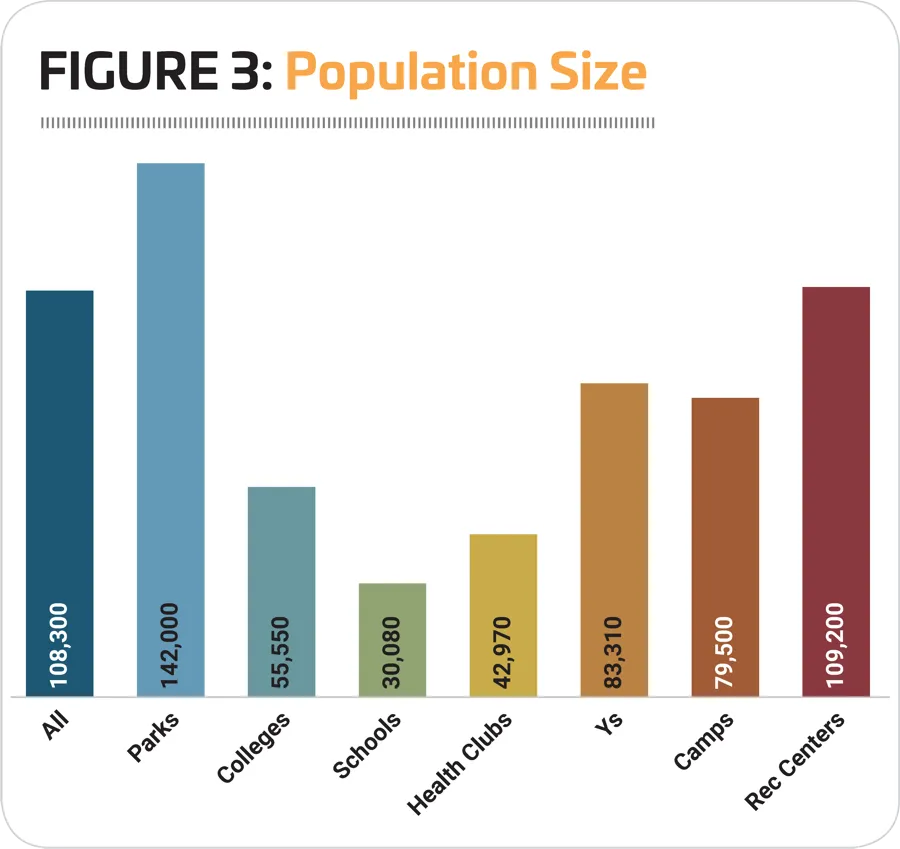

On average, the departments, facilities and organizations covered here serve a population of 108,300 people, up substantially from 2019, when the average was 92,030. In fact, with the exception of 2017, the population size of respondents has been on the rise since 2016, when it was 83,200 people.

Despite the higher average population, though, a majority of respondents said their facilities reach fewer than 50,000 people. Some 61.6% of respondents said their facilities reach an average population of 50,000 or fewer people. And more than three in 10 (30.9%) said they reach fewer than 10,000. Another 14.6% of respondents said they serve a population of 50,000 to 99,999 people. Some 11.5% said their facilities reach an average population of between 100,000 and 199,999 people. Finally, 12.3% of respondents said they reach a population of 200,000 or more.

Respondents from parks and recreation districts and departments reach the largest population size, serving an average of 142,000, up substantially from 118,600 in 2019. They were followed by recreation centers, at 109,200; Ys (83,310); camps (79,500); colleges (55,550); health clubs (42,970); and schools (30,080). (See Figure 3.)

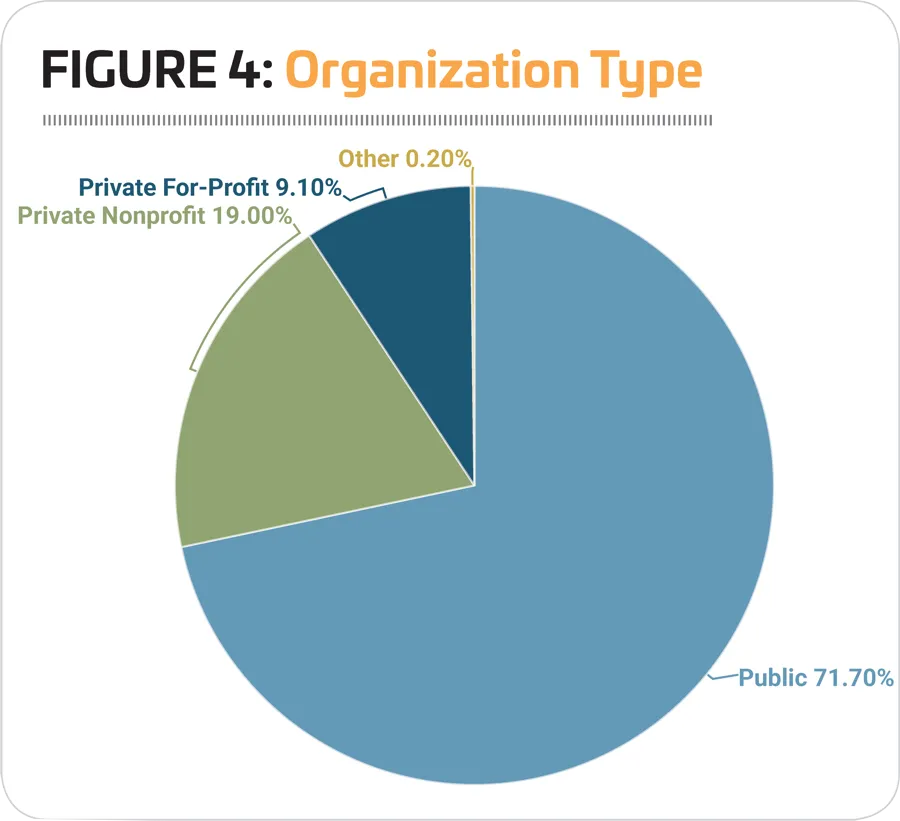

Respondents were most likely to report from public organizations, such as parks and recreation districts and departments, public universities and school districts. More than seven in 10 (71.7%) respondents said they were with public organizations. (See Figure 4.) They were followed by those working for private nonprofit organizations. Some 19% of respondents represent private nonprofits, such as Ys, Boys & Girls Clubs, JCCs and other similar facilities. Finally, 9.1% of respondents reported from private, for-profit organizations, which includes facilities like health clubs, resorts, waterparks and others.

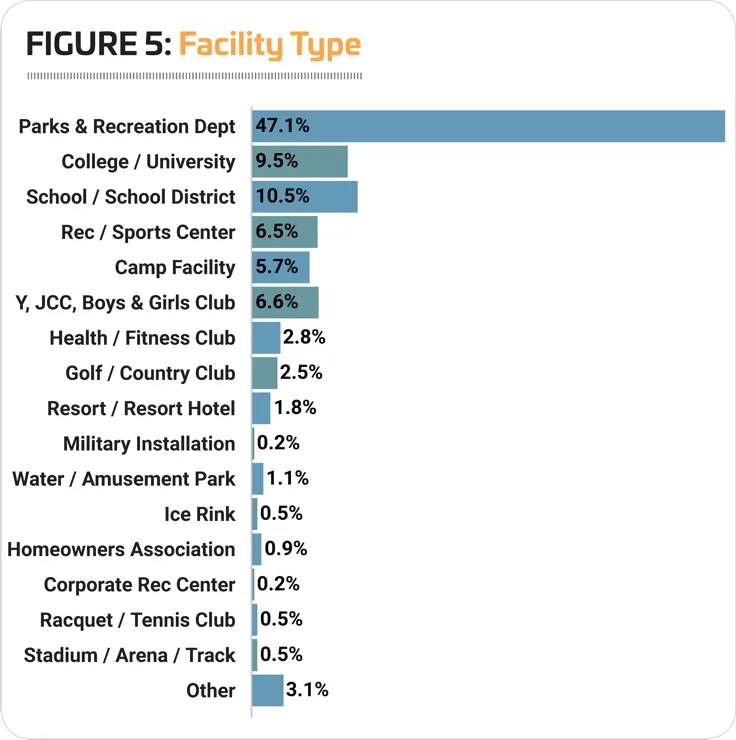

The largest percentage of respondents were from parks and recreation departments, park districts and similar organizations. Nearly half (47.1%) of respondents said they represented parks. (See Figure 5.) They were followed by respondents from schools and school districts (10.5%); colleges and universities (9.5%); YMCAs, YWCAs, JCCs and Boys & Girls Clubs (6.6%); community or private recreation and sports centers (6.5%); and campgrounds, RV parks and private or youth camps (5.7%). Smaller numbers of respondents reported from other types of facilities, including: sports, health, fitness and medical fitness facilities (2.8%); golf and country clubs (2.5%); resorts and resort hotels (1.8%); waterparks, theme parks and amusement parks (1.1%); homeowners associations (0.9%); ice rinks (0.5%); racquet and tennis clubs (0.5%); stadiums, arenas and tracks (0.5%); and corporate recreation and sports centers (0.2%). Another 3.1% of respondents said they work for "other" types of facilities.

When it comes to organizational structure, some types of facilities are more likely to be public or government-based organizations, while others are more likely to be nonprofit or for-profit organizations. A vast majority (98.5%) of park respondents indicated that they were with public organizations. Also highly likely to be from public organizations were respondents from schools and school districts (92.7%) and those from colleges and universities (66.9%).

Similarly, a vast majority of respondents from Ys and similar organizations said that they were with private nonprofits. Some 95.3% of Y respondents said they were private nonprofits. More than half (54.7%) of camp respondents and 29% of college and university respondents said they were with private nonprofit organizations.

For-profit organizations were most common among those from sports, health, fitness and medical fitness facilities, where more than half (51.4%) said they were with for-profit organizations. Some 29.3% of camp respondents said they were for-profit.

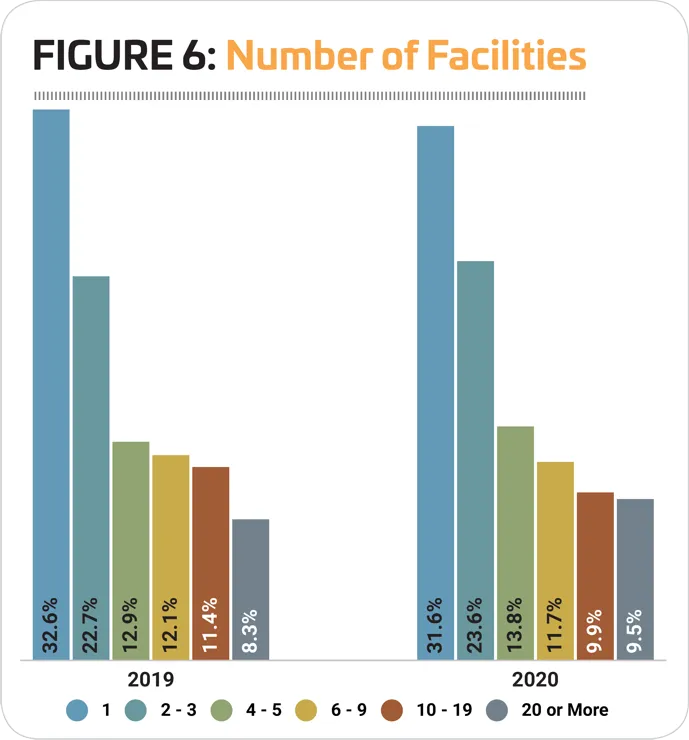

On average, survey respondents manage 8.3 facilities, up from 7.9 in 2019, showing a continuing increase from an average that has ranged between 6.4 and 7.4 in past surveys. This is driven by a decrease in the percentage of respondents who indicate that they manage between one and three facilities, down from 59.7% in 2018 to 55.2% in 2020. Around another quarter (25.5%) said they manage between four and nine facilities, and another 19.4% said they manage 10 or more facilities. (See Figure 6.)

Respondents from urban and suburban communities were more likely than those from rural areas to report that they manage a larger number of facilities. Conversely, rural respondents were more likely to report that they manage a single facility. On average, urban respondents manage 10 facilities, suburban respondents manage 8.8 facilities, and rural respondents manage 6.5. Some 20.9% of urban respondents and 22% of suburban respondents said they manage 10 or more facilities, compared with 15.1% of rural respondents. On the other hand, 33.8% of rural respondents said they manage a single facility, compared with 29.8% of suburban and 31.6% of urban respondents.

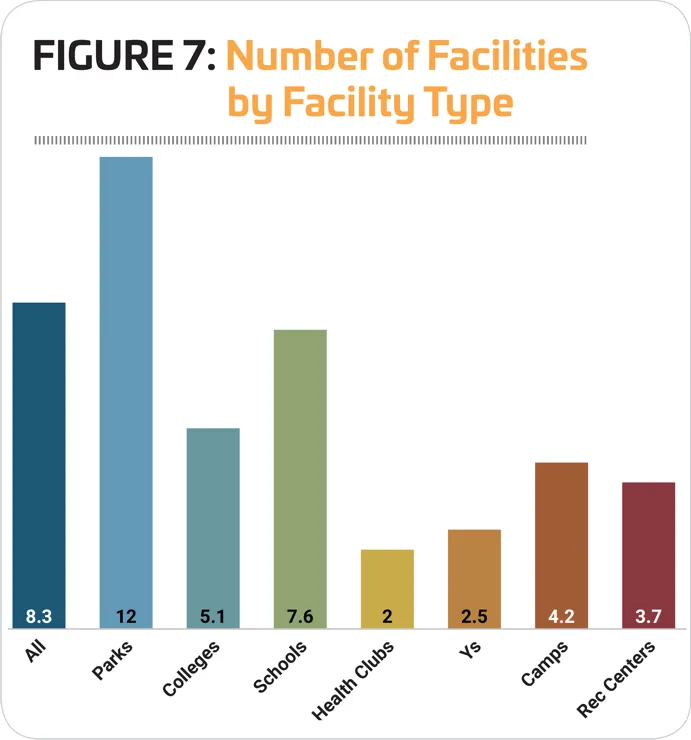

Respondents from parks facilities were the most likely to report that they manage a larger number of facilities. On average, parks respondents manage 12 facilities (up from 10.7 in 2019), with 30.5% reporting that they manage 10 or more facilities. (See Figure 7.) They were followed by school respondents, who manage an average of 7.6 facilities, with 17.6% reporting that they manage 10 or more.

Respondents from health clubs and camps were the most likely to report that they manage just a single facility, with 69.4% of health club respondents and 62.3% of camp respondents indicating that they manage just a single facility.

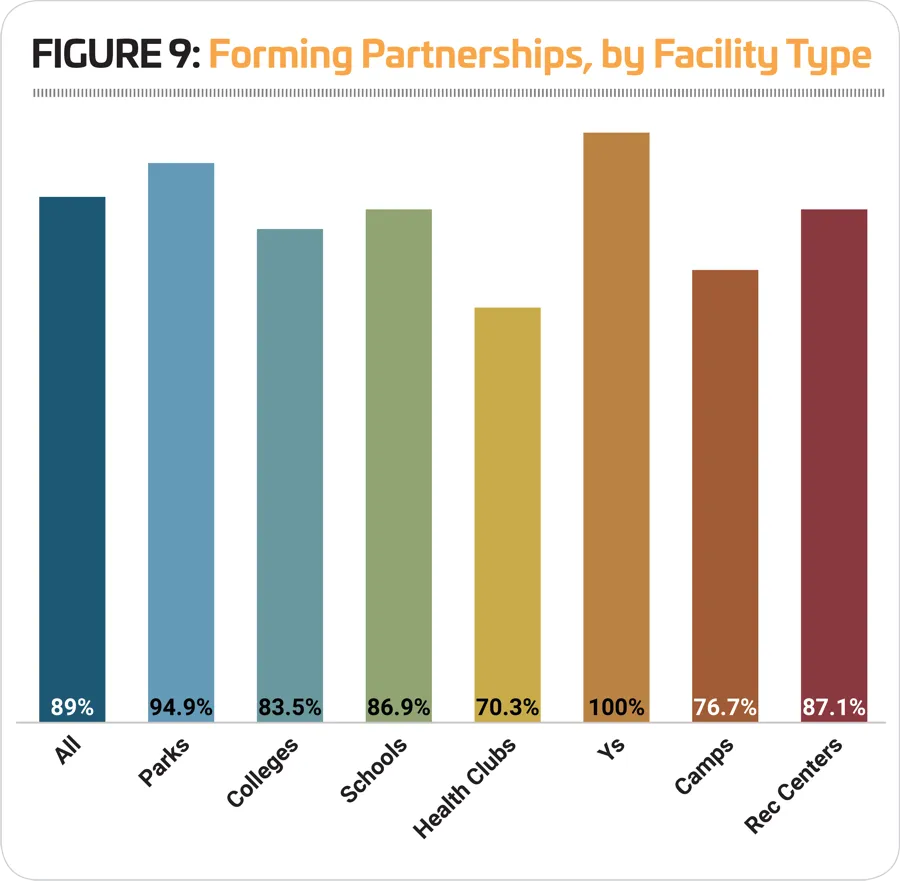

Many recreation, sports and fitness facilities partner with other organizations in order to broaden their capabilities in terms of funding, programming, outreach and more. A vast majority, 89%, of respondents to the Industry Report survey indicated that they form these kinds of partnerships, up from 87.9% in 2019.

As usual, local schools hold the top spot as the most common type of partner for all facility types. Nearly two-thirds (64.2%) of survey respondents said they had partnered with local schools. (See Figure 8.) They were followed by local government (58.8%), nonprofit organizations (50.9%), state government (39.4%), and corporations or local businesses (37.5%).

Respondents from Ys and parks were the most likely to report that they had partnered with outside organizations, while those from health clubs and camps were the least likely to do so. All Y respondents (100%) said they partner with other organizations, and 94.9% of parks respondents had done so. This compares with 70.3% of health club respondents and 76.7% of camps. (See Figure 9.)

Given that all Y respondents report partnering with other organizations, it's no surprise that they were the most likely to partner with most of the different types of organizations covered by the survey. The only exceptions were local government, and colleges and universities. Ys were more likely than other respondent types to indicate that they partnered with local schools (91.9% of Ys had partnered with local schools), nonprofit organizations (82.6%), corporations and local businesses (72.1%), health care facilities (59.3%), state government (51.2%), other Ys (48.8%), military (33.7%), federal government (30.2%), and private health clubs (11.6%).

Park respondents were the most likely to report that they had partnered with local government (73.7% had done so), while college respondents were the most likely to report that they had partnered with other colleges and universities (64.4%).

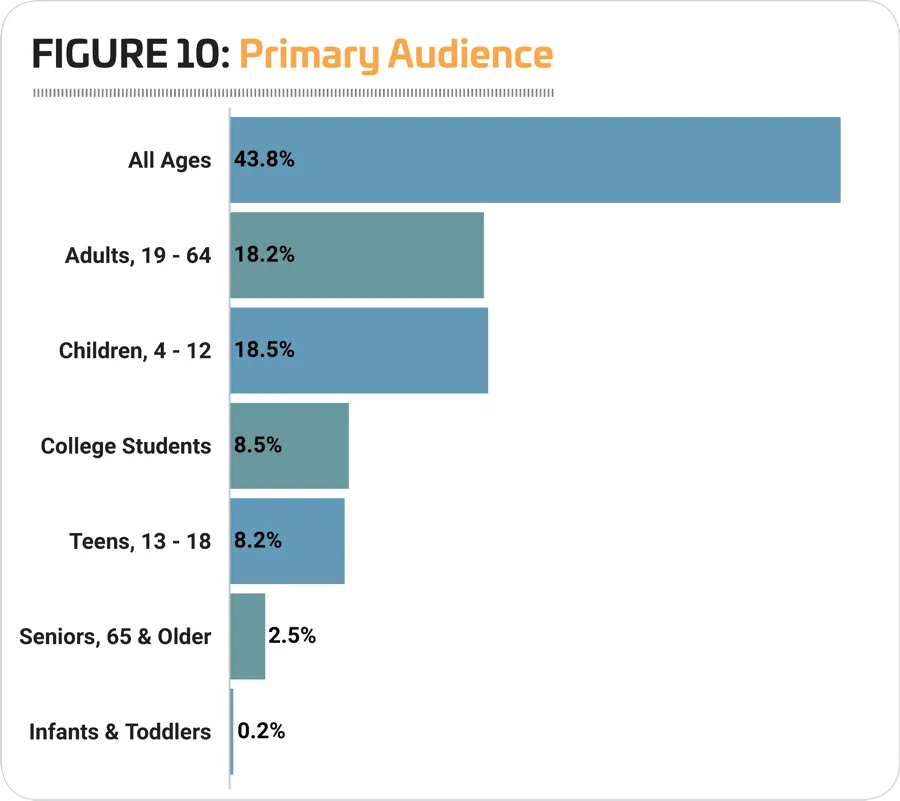

When it comes to the primary audience served by their facilities, respondents were most likely to report that they reach all ages. Some 43.8% of respondents said their facilities reach an audience of all ages. The next largest groups primarily reach children ages 4 to 12 (18.5%) and adults 19 to 64 (18.2%). Smaller numbers of respondents said their primary audience was made up of college students (8.5%), teens ages 13 to 18 (8.2%), seniors (2.5%), or infants and toddlers (0.2%). (See Figure 10.)

Given the different nature of the programs and services offered by different facility types, it comes as no surprise to find that some are more likely to serve specific audiences (such as college students or adults) than others.

Respondents from Ys were the most likely to report that they serve all ages, with 59.5% indicating that this is their primary audience. They were followed by rec centers (53.4%) and park respondents (53.4%).

Children ages 4 to 12 were most likely to be the primary audience for park respondents, 26.4% of whom said they primarily reach children. They were followed by camps (20.3%) and recreation centers (18.8%).

Adults from age 19 to 64 were the most likely to be the primary audience for health club respondents, with 72.2% indicating this is the main audience they reach. They were followed by Ys (20.9%) and camps (17.6%).

College students, obviously, were most likely to be the primary audience for college and university respondents, 85.4% of whom said this was their main audience. Teens were the predominant audience for schools and school districts (51.8%). And seniors were more likely to be the primary audience at health clubs (8.3%) than other facility types.

Revenues & Expenditures

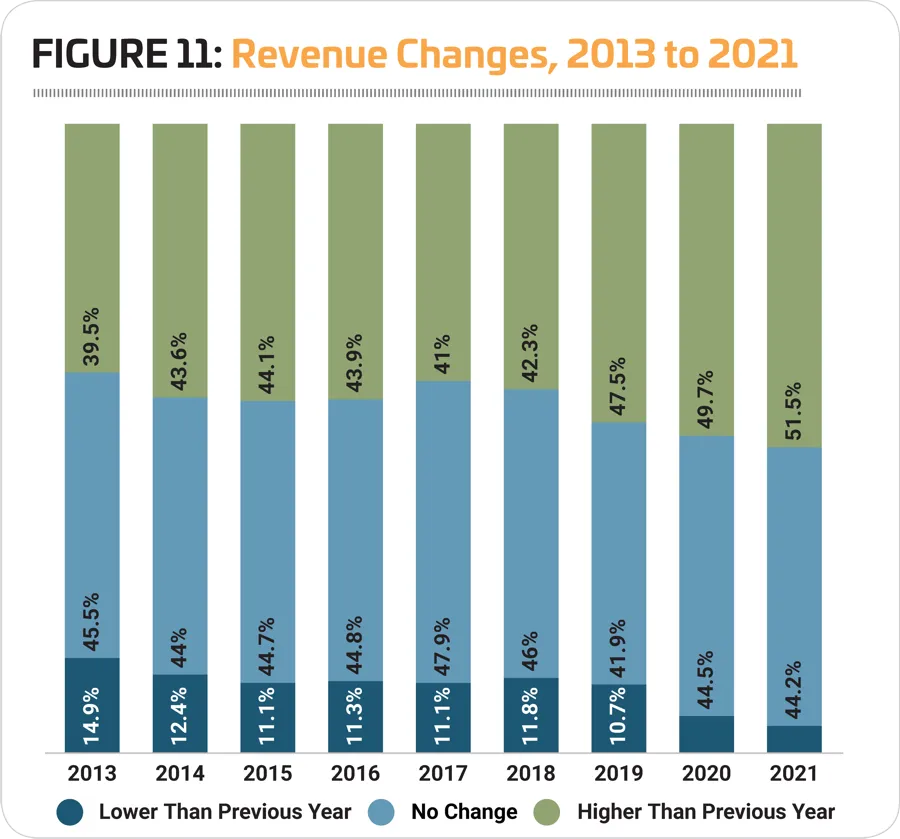

Since 2012, the percentage of respondents who report that their revenue has increased year-over-year has grown from 39.5%, to 47.5% in 2019. In that same time period, the percentage reporting that their revenue has fallen has decreased, from 14.9% who saw revenues decrease from 2012 to 2013, to 10.7% reporting a decrease in 2019 from 2018. (See Figure 11.)

When the Industry Report survey was conducted, in January 2020, nearly half (49.7%) of respondents were expecting their revenues to increase this year, and more than half (51.5%) said they expected their revenues to increase in 2021. Of course, that was before the COVID-19 crisis led to social distancing measures that required the closing of nearly all facilities across the country. For updated data reflecting the impact of COVID-19, see "COVID-19 Impact: Revenues" on the next page.

COVID-19 IMPACT: REVENUES

In our COVID-19 Update Survey, we asked respondents about the impact of the measures taken to address the pandemic on their revenues.

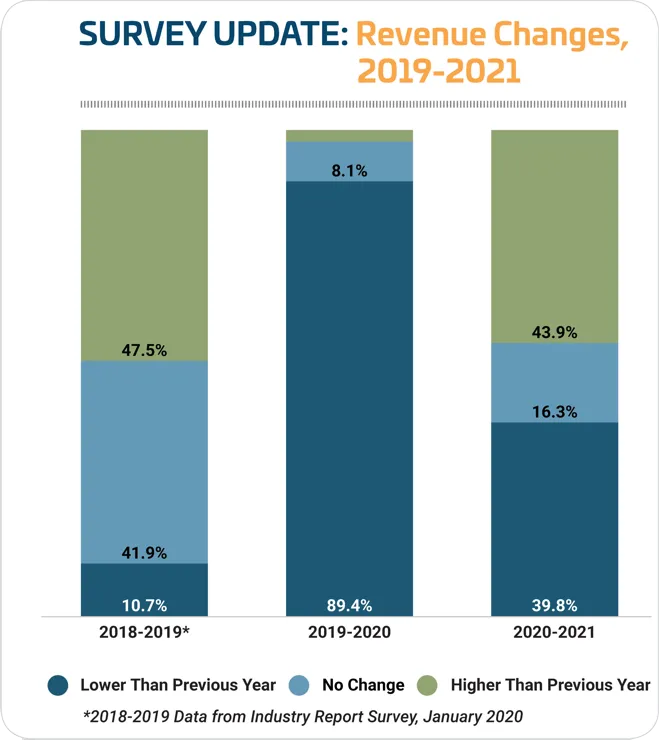

While 10.6% said they expect their revenues in 2020 to be higher than or the same as 2019, the vast majority of respondents are expecting a hit.

Most respondents expect their revenues to decrease from 30-50%. Some 35.9% of respondents are expecting revenues to fall by 20-30%, and 28.7% are expecting a drop of 40-50%. And 15% of respondents expect their revenues to drop by more than half in 2020.

Respondents expect recovery to begin in 2021, with 43.9% projecting revenues to increase. Another 16.3% expect no change to revenues in 2021.

Of the 39.8% who are expecting lower revenues in 2021 than in 2020, 8.3% expect revenues to fall by 10%, 21.2% expect a drop of 20-30%, 8.2% expect a drop of 40-50%, and 2.1% expect their revenues to fall by more than 50%.

Here's what three respondents had to say about the impact:

"COVID-19 has devastated our revenues. We are heavily dependent on tourism. We have reduced over 90% of our staff, including full-time staff." (Parks & Recreation)

"Resulted in closure of campus to all but essential personnel. Transitioned all academic programs to distance learning model until further notice. Suspended all athletic, recreation and intramural activities until further notice. Significantly impacted budget for 2019-20 and beyond, due to loss of revenue and reduced funding, full extent TBD." (College/University)

"Closed all buildings to the public but increased attendance to parks and trails by 176%. Made up lost revenue through program cancelations, no seasonal hiring and eliminated contract hiring, while repurposing present staff to keep them employed." (Parks & Recreation)

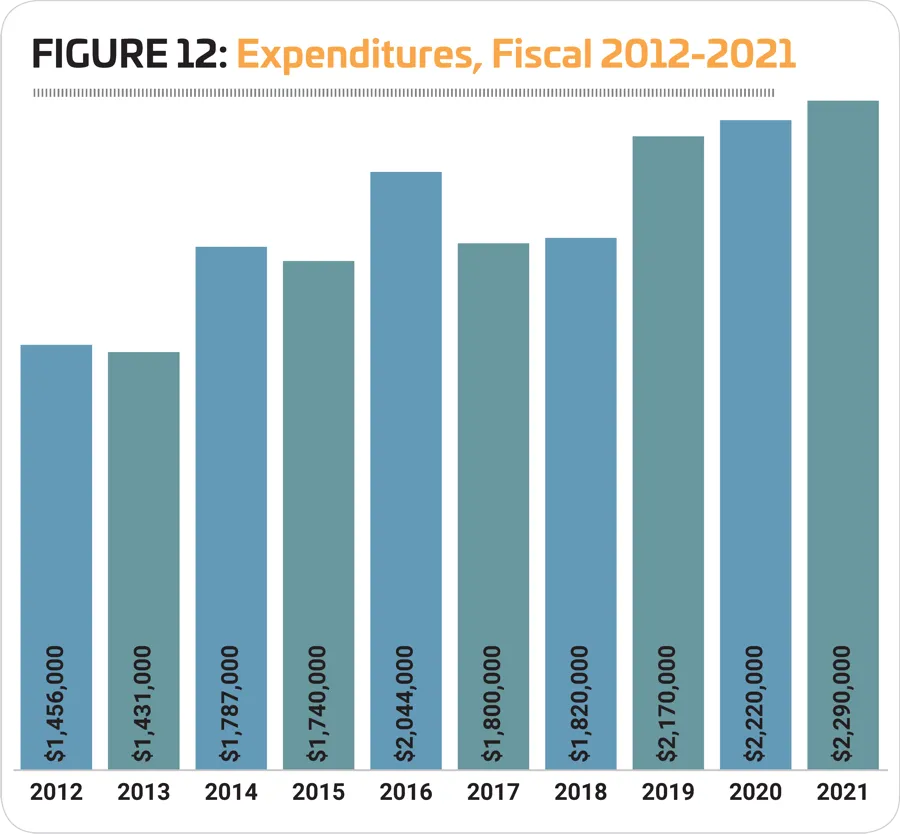

The average annual operating expenditure for respondents to the Industry Report survey continues to rise, reaching $2,170,000 in fiscal 2019, an increase of 19.2% from the average of $1,820,000 reported in 2018. However, it is just 6.2% higher than the average reported in fiscal 2016, of $2,044,000. (See Figure 12.)

Looking forward, respondents in January were expecting their operating expenses to climb a further 5.5% over the next two years, reaching an average of $2,290,000 in fiscal 2021. These projections will certainly be affected by social distancing measures and facility closures in various ways, which will become clearer over time

From 2018 to 2019, respondents from rural communities reported the steepest increase to their operating costs. The average operating cost for rural respondents in 2019 was $1,430,000, 40.2% higher than the average reported for 2018, $1,020,000. Urban and suburban respondents also reported a substantially higher average cost in 2019, with suburban respondents reporting a 16.7% increase from $2,150,000 in 2018 to $2,510,000 in 2019, and urban respondents reporting a 13.8% increase, from $2,390,000 in 2018 to $2,720,000 in 2019.

Looking forward, rural respondents continue to expect the steepest increase in their operating costs, projecting a 9.8% increase from 2019's average to $1,570,000 in 2021. They were followed by suburban respondents, who expect operating costs to increase 5.6%, to an average of $2,650,000 in 2021. Urban respondents projected an increase of 2.9%, to an average of $2,800,000 in 2021.

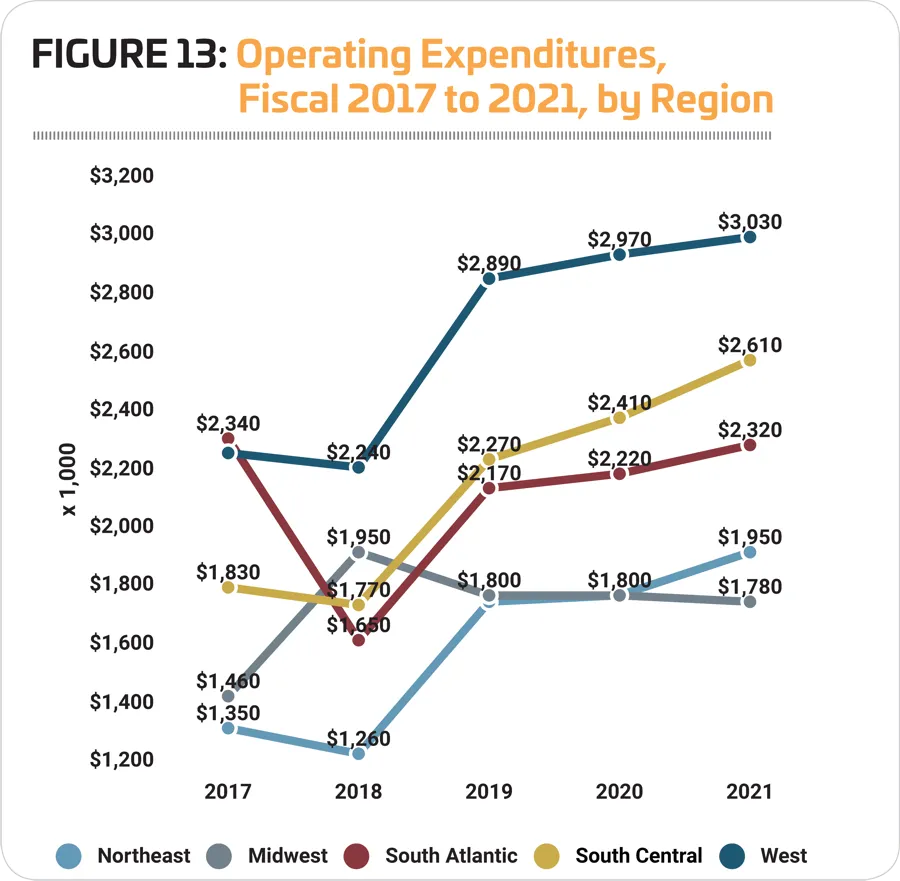

After being the only category of respondents to report an increase in average operating expenses in 2018, respondents from the Midwest were the only respondents in 2020 who reported a decrease to their average operating expenses in 2019. Midwestern respondents reported an average operating expenditure of $1,800,000 in 2019, 7.7% lower than the average for 2018 of $1,950,00. The steepest increase to the average expense from 2018 to 2019 was reported by those in the Northeast, who saw a 41.3% jump to $1,780,000. They were followed by those from the South Atlantic (reporting a 31.5% increase), the West (29%) and the South Central region (28.2%). (See Figure 13.)

Looking forward, Midwestern respondents continue to be the only region expecting operating expenses to either hold steady or fall, projecting a 1.1% decrease from fiscal 2019 to 2021, to an average of $1,780,000. The greatest increase was expected by respondents in the South Central region. South Central respondents projected a 15% increase to their average operating expense, to $2,610,000 in 2021. They were followed by respondents in the Northeast (projecting a 9.6% increase), the South Atlantic (6.9%), and the West (4.8%).

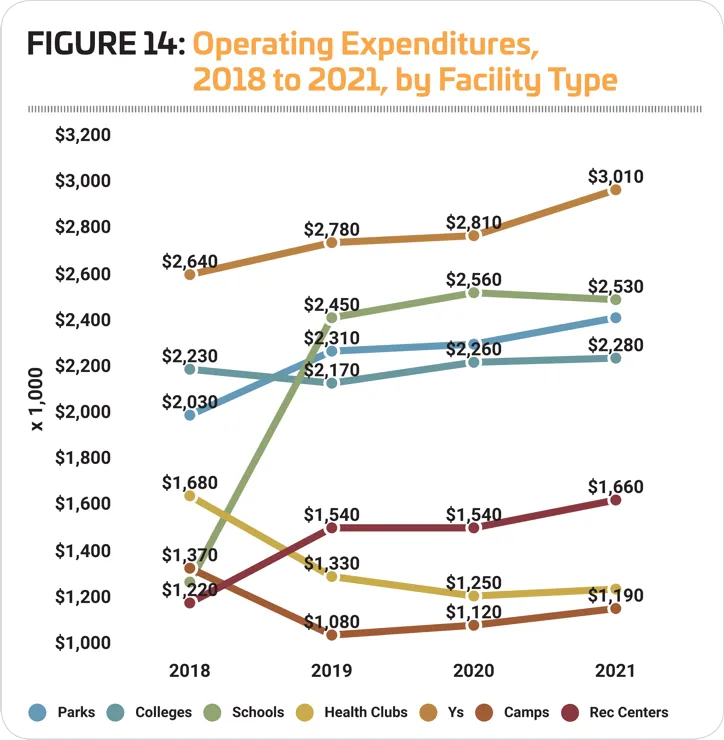

From fiscal 2018 to fiscal 2019, respondents from parks, schools, Ys and rec centers reported increases to their average operating expenditures, while those from camps, health clubs and colleges saw decreases. The greatest increase was seen among school respondents who reported an average operating expenditure of $2,450,000 in 2019, 87% higher than the average reported in 2018. They were followed by rec centers, reporting an increase of 26.2% to an average of $1,540,000 in 2019; parks (up 13.8% to $2,310,000); and Ys (up 5.3% to $2,780,000). The greatest decrease was reported by camp respondents who had an average operating expense of $1,080,000 in 2019, 21.2% lower than the average reported in 2018. They were followed by health clubs, down 20.8% to an average of $1,330,000; and colleges, down 2.7% to an average of $2,170,000. (See Figure 14.)

Looking forward, only health club respondents expect their operating costs to decrease between 2019 and 2021. They projected a 3.8% drop, to an average of $1,280,000 in 2021. The greatest increase was expected by respondents from camps, who projected a 10.2% increase to an average operating expenditure of $1,190,000 in 2021. They were followed by Ys (up 8.3% to $3,010,000 in 2021), rec centers (up 7.8% to an average of $1,660,000), parks (up 6.1% to $2,450,000), colleges (up 5.1% to $2,280,000) and schools (up 3.3% to $2,530,000).

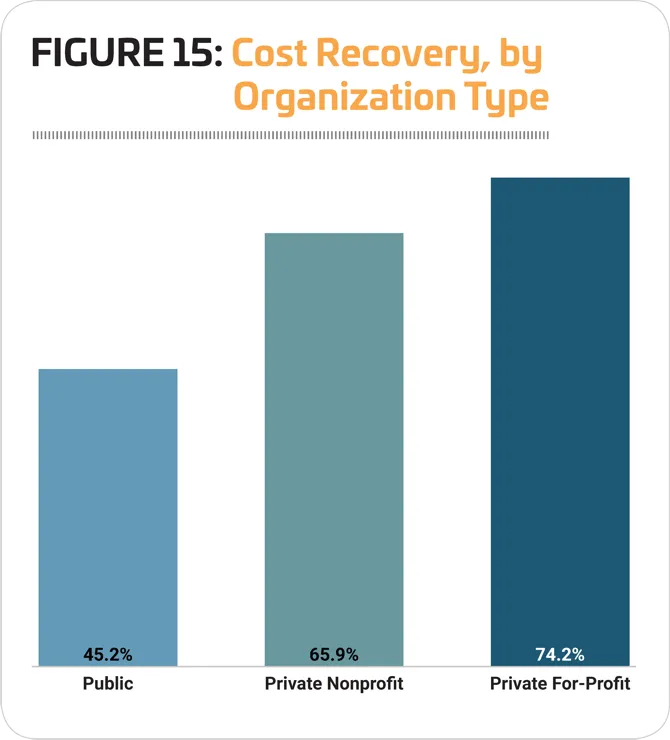

When it comes to costs and revenues, the percentage of costs recovered tends to depend on the type of organization represented. Obviously, private for-profit organizations will be more likely to cover a higher percentage of their operating expenditures via revenues than nonprofits and public organizations. On average, all respondents said they recover 51.7% of their operating costs, up from 47.3% in 2019. For public organizations, 45.2% of costs are recovered, up from 42% in 2019. This compares with 74.2% for private for-profit organizations (up from 69.3%) and 65.9% for private nonprofits (up from 60.1%). (See Figure 15.)

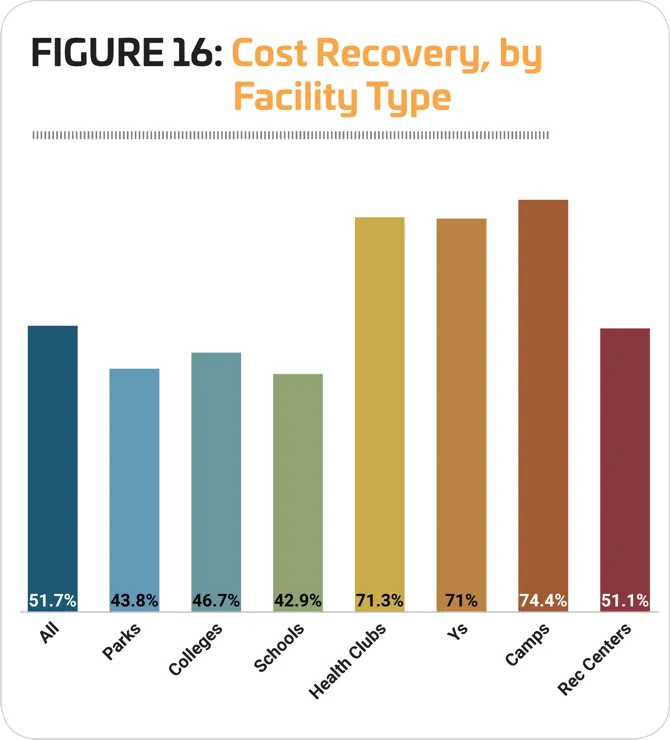

Depending on the type of facility, some are more or less likely to recover more or less of their costs via revenues, with some like parks and schools relying more heavily on tax dollars, while others like health clubs receive little support outside of the revenues they earn.

Respondents from camps, health clubs and Ys are the most effective at covering their operating costs with revenues. Camp respondents recover nearly three-quarters (74.4%) of their costs, while health clubs earn 71.3% and Ys earn 71%. Respondents from schools and parks earn back the lowest percentage of their operating costs via revenues, with parks earning back 43.8% and schools earning 42.9%. (See Figure 16.)

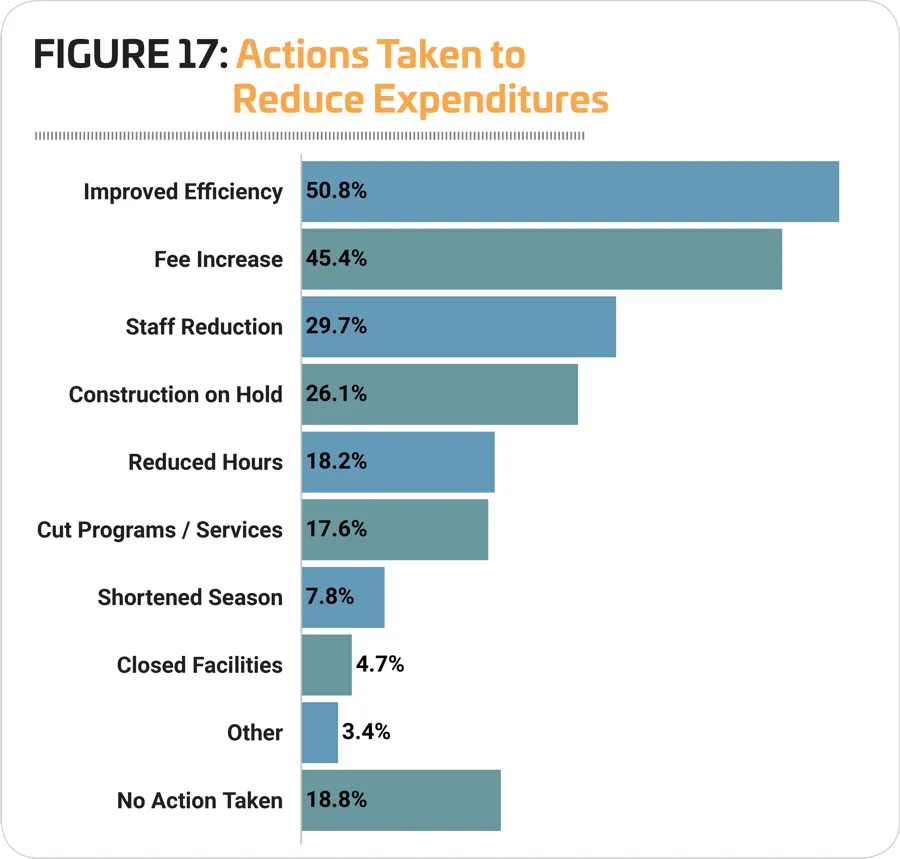

After dropping fairly steadily for the past decade, the percentage of respondents who reported that they had taken action to reduce their operating expenses in the past year increased in 2019. This even before COVID-19 began having an impact on facilities and budgets. Some 81.2% of respondents in January said that they had taken action to reduce their expenditures, up from 80.3% in 2019.

More than half (50.8%) of respondents said they had improved energy efficiency in order to reduce expenditures. As in most years, this was the most common action taken. It was followed closely by increasing fees, an action taken by 45.4% of respondents. More than one-quarter of respondents said they had reduced staffing levels (29.7%) or put construction or renovation plans on hold (26.1%). Fewer respondents had taken other actions, such as reducing their hours of operation (18.2%), cutting programs or other services (17.6%), shortening the season (7.8%) or closing facilities (4.7%). (See Figure 17.)

We also asked respondents in our Industry Survey Update questionnaire about similar actions they've taken in light of the COVID-19 emergency. You'll find a summary of those responses under the "Challenges, Then & Now" section, beginning on page 32.

In January's survey, respondents from Ys, camps, health clubs and parks were the most likely to report that they had taken action to reduce their expenditures. Some 90.6% of Ys, 87.8% of camps, 81.1% of health clubs and 80.6% of parks said they had taken such action. Respondents from colleges and schools were less likely to indicate that they had taken action to reduce their expenses, though more than three-quarters (76.9% of colleges and 76.3% of schools) had done so.

Respondents from Ys were more likely than others to report that they had improved energy efficiency (67.1% of them had done so), increased fees (65.9%), reduced staff (48.8%), or cut programs and services (23.5%).

Respondents from colleges were more likely than others to report that they had reduced their hours of operation (33.1%) or closed facilities entirely (5.8%), while those from camps were most likely to report that they had put construction or renovation plans on hold (34.7%) and parks were the most likely to report that they had shortened their season of operation (10.1%).

Facility Usage & Membership

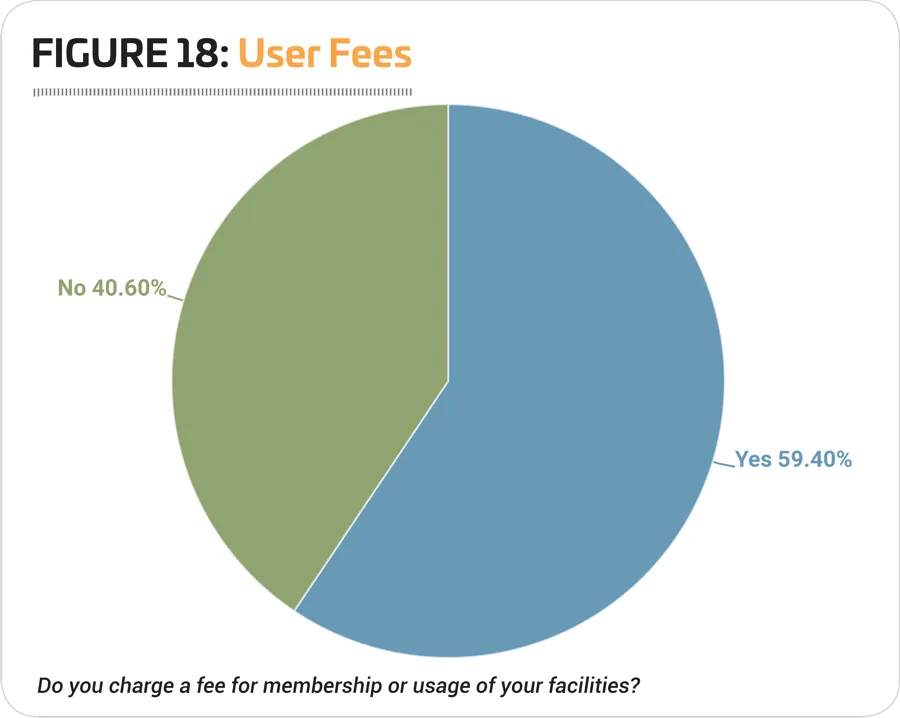

As is generally the case, around six in 10 respondents said they currently charge a fee for membership or for using their facilities. Nearly six in 10 (59.4%) respondents said they currently charge a fee, up slightly from 58.2% in 2019. (See Figure 18.)

Respondents from Ys, health clubs and colleges were the most likely to report that they charge a fee for membership or for using their facilities. Some 94.2% of Y respondents, 86.5% of health club respondents and 66.9% of college respondents said they charge a fee for membership or use.

Conversely, schools were the least likely to charge a fee, though the percentage who do so increased substantially from 2019. Some 26.3% of school respondents said they charge a fee for using their facilities, up from 18.7% in 2019.

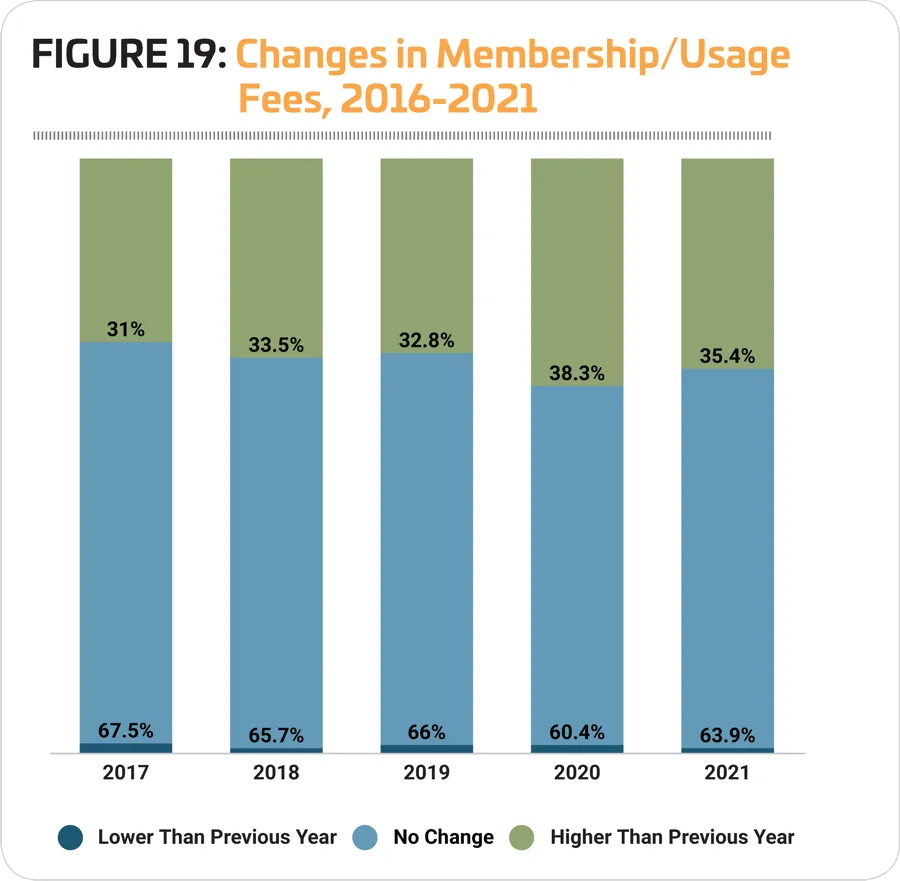

Of those respondents who currently do charge a fee for membership or for using their facilities, the percentage who have increased their fees decreased slightly in 2019. While 33.5% of respondents who charge fees said they had increased the cost in 2018, 32.8% had done so in 2019. At the same time, the percentage who said fees had remained the same increased, from 65.7% in 2018 to 66% who kept fees steady in 2019. (See Figure 19.)

Looking forward, more respondents were expecting that they would increase their fees in 2020 and in 2021. Some 38.3% of those who charge a fee said that fee would be increased in 2020, while 35.4% said an increase would be made in 2021.

Among the facilities that charge a fee for membership or usage, those from camps, Ys and health clubs were the most likely to report that they had raised their fees from 2018 to 2019, while those from colleges were the least likely to have increased fees. Some 51.2% of camp respondents who charge a fee said they had raised that fee in 2019, down from 57.9% who reported raising fees in 2018. They were followed by Ys (47.5%, up from 44.9%) and health clubs (31.3%, down from 43.2%). Just 24.1% of college respondents said they had increased their fee from 2018 to 2019.

The same trend mostly holds true for the next two years, with camps continuing to be the most likely to plan fee increases. Some 56.1% of camp respondents who charge a fee said they would be increasing it in 2020, and 61% expected an increase in 2021. They were followed by Ys, where 54.3% were anticipating a fee increase in 2020 and 42.9% projected an increase in 2021.

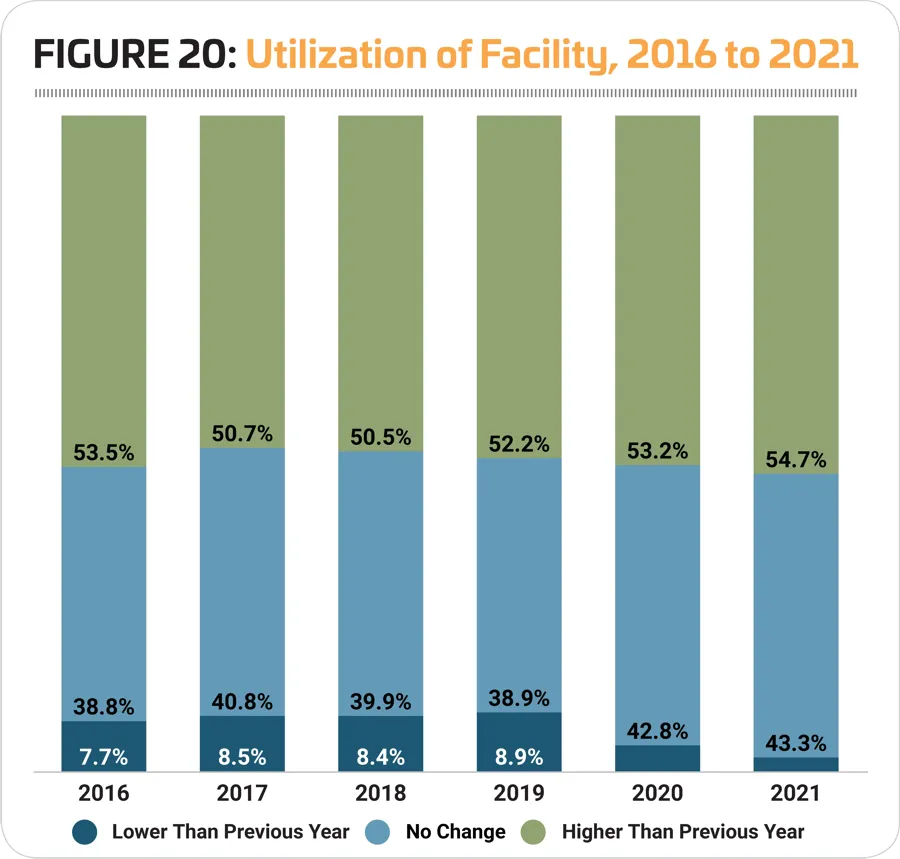

More than half (52.2%) of respondents said that the number of people using their facilities had increased from 2018 to 2019, up from 50.5% reporting an increase from 2017 to 2018. At the same time, 38.9% reported no change in the number of people using their facilities, while 8.9% saw a decrease. (See Figure 20.)

Looking forward, the percentage of respondents who in January were expecting to see further increases in the number of people using their facilities grows slightly over the next two years, while the percentage expecting a drop in numbers falls. From 2019 to 2020, 53.2% of respondents said they expected the number of people using the facilities to increase, while 4% expected a decrease. And from 2020 to 2021, 54.7% of respondents were expecting an increase, with 2% projecting a decline in the number of people using their facilities.

From 2018 to 2019, respondents from rec centers and parks were the most likely to report that the number of people using their facilities had increased, while those from colleges were least likely to see an increase. Some 60% of rec center respondents and 58.7% of park respondents said the number of people using their facilities had grown from 2018 to 2019. At the same time, just over a third (35.5%) of college respondents reported an increase in 2019.

Looking forward, rec centers and parks remain more likely to report that they expected increases in 2020 and 2021, with 61.4% of rec centers and 57.3% of parks projecting an increase in 2020, and 65% of rec centers and 59.3% of parks anticipating an increase in 2021.

Staffing

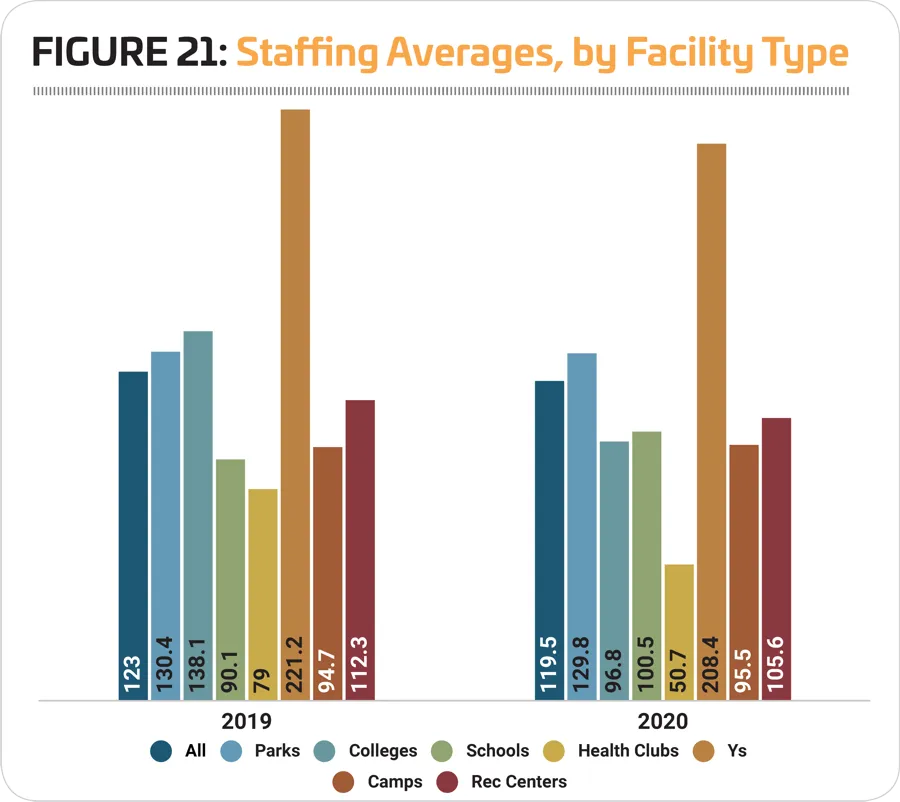

There was a slight decrease in the average number of people employed at the organizations covered by the survey. While in 2019, respondents said they employed an average of 124 workers, in 2020, respondents employed an average of 119.5 workers. On average, in January 2020, survey respondents employed: 31.1 full-time employees (up from 26.7 in 2019); 45.6 part-time employees (down from 47.9), 51.2 seasonal workers (up from 47.2), 46.4 volunteers (up from 42), and 12 employees of "other" designations.

As is generally the case, Ys employ the highest number of employees, with an average of 208.4 total employees, down from 221.2 in 2019. They were followed by parks and recreation respondents, who employed an average of 129.8 workers, and rec centers, with 105.6. The smallest number of people were employed by health clubs, with an average of 50.7 employees in 2020. (See Figure 21.)

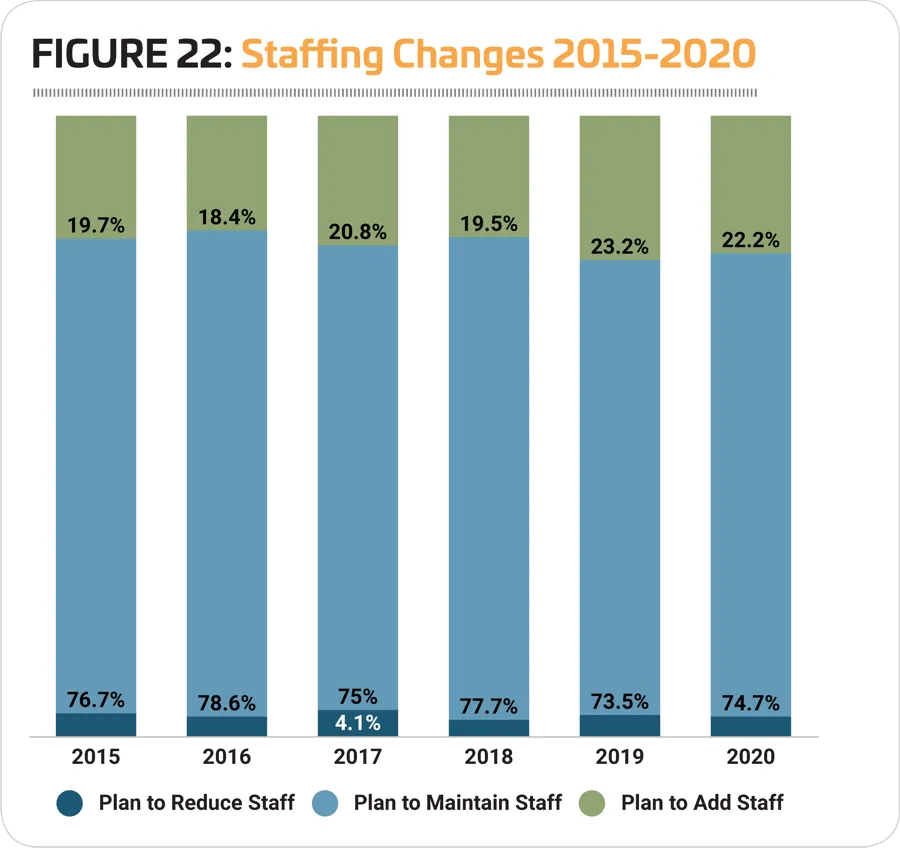

From 2015 to 2020, the percentage of respondents who report that they plan to add staff at their facilities has hovered just above or below one-fifth. In 2020, 22.2% of respondents said they were planning to add more staff at their facilities, down slightly from 23.2% in 2019. At the same time, 74.7% of respondents said they were planning to maintain existing staffing levels, and 3.1% were planning a reduction. (See Figure 22.)

That said, in the wake of COVID-19, nearly two-thirds (65.7%) of respondents to the Update Survey said they had put hiring plans on hold, and 44.8% said they had laid off or furloughed their existing staff.

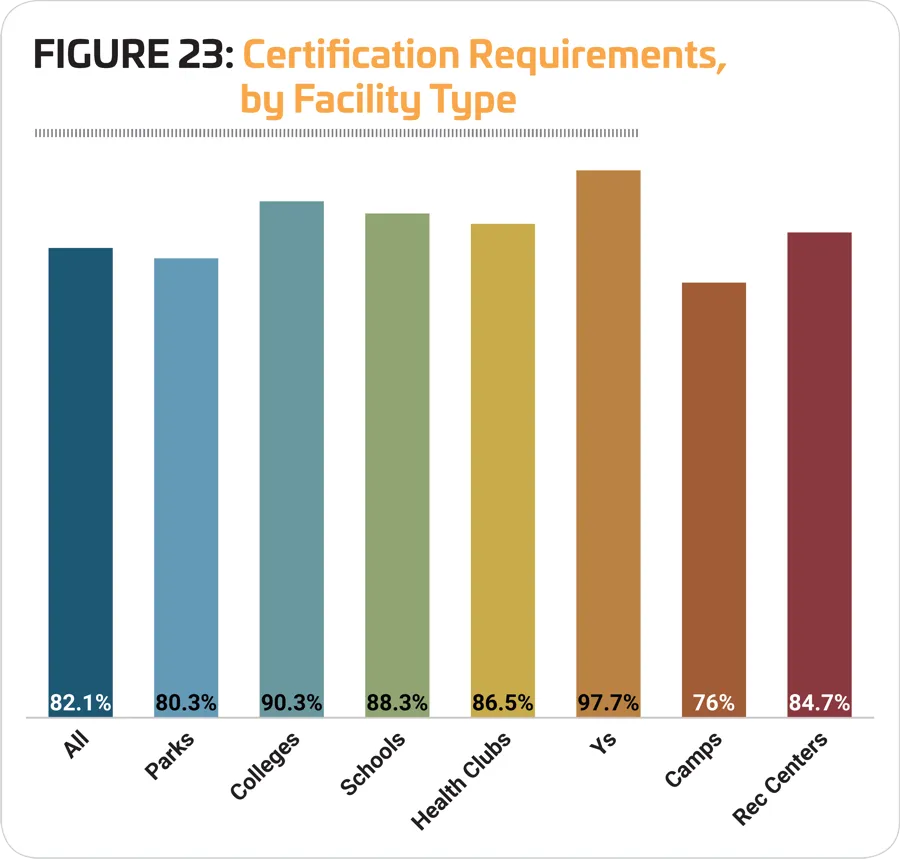

Certifications continue to be a powerful tool that organizations and their employees (and potential employees) alike rely on to encourage and measure ongoing professional development in the field. Some certifications help prove a certain level of skill and knowledge to maintain safety requirements (think lifeguard or food-service certification), while others simply test and qualify other types of professional expertise. A majority of respondents (82.1%) said they require certifications for at least some of their staff members, down slightly from 83.2% in 2019.

Respondents from Ys, colleges and schools were the most likely to require certification for some of their employees. Some 97.7% of Y respondents said they currently require certification. They were followed by colleges, with 90.3% requiring certification, and schools, at 88.3%. Respondents from camps were the least likely to require certification for their staff, though 76% said they do have such a requirement, up from 72.6% in 2019. (See Figure 23.)

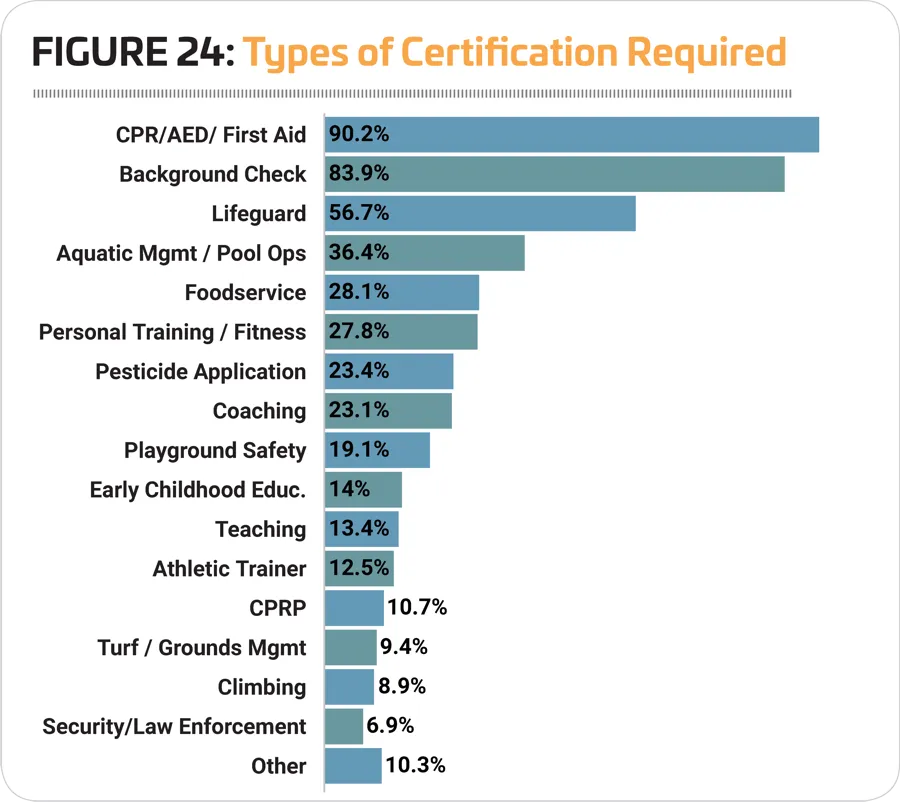

Of those respondents that require certification, the most common types of certification required included CPR/AED/First Aid (required by 90.2% of those who said they require some staff members to be certified), background checks (83.9%), and lifeguard certification (56.7%). (See Figure 24.) More than one-quarter of respondents also require an aquatic management/pool operations certification (36.4%), food service certification (28.1%), or personal training/fitness certification (27.8%). More than one-fifth expect a pesticide application certification (23.4%) or a coaching certification (23.1%).

Respondents from facilities that include aquatic elements are obviously much more likely to require lifeguard and aquatic management or pool operations certifications for some of their staff members. While 56.7% of all respondents who require certification said they ask some staff members to achieve lifeguard certification, for those with aquatic facilities, that number jumps to 87%. And while 36.4% of all respondents require aquatic management and pool operations certifications, 58.5% of those with aquatic facilities do so.

Given the varying nature of their operations and programming, it comes as no surprise that some industry segments were more likely to require certain types of certification than others. Respondents from parks were the most likely to report that they require playground safety certification (37%), pesticide application certification (23.4%), Certified Park and Recreation Professional (CPRP) certification (21.3%), turf and grounds management certification (11.9%), and security or law enforcement certification (9.1%). Ys were the most likely to require background checks (98.8%), CPR/First Aid (97.6%), lifeguard certification (86.9%), personal training or fitness certification (72.6%), aquatic management or pool operations certification (66.7%), and childcare and early childhood education certification (56%). Camp respondents were the most likely to require food service certification (61.4%) and climbing certification (31.6%). Those from schools were the most likely to require coaching (74.4%) or teaching (57%) certifications. And finally, respondents from colleges and universities were the most likely to require athletic trainer certification (31.3%).

Facilities & Construction Plans

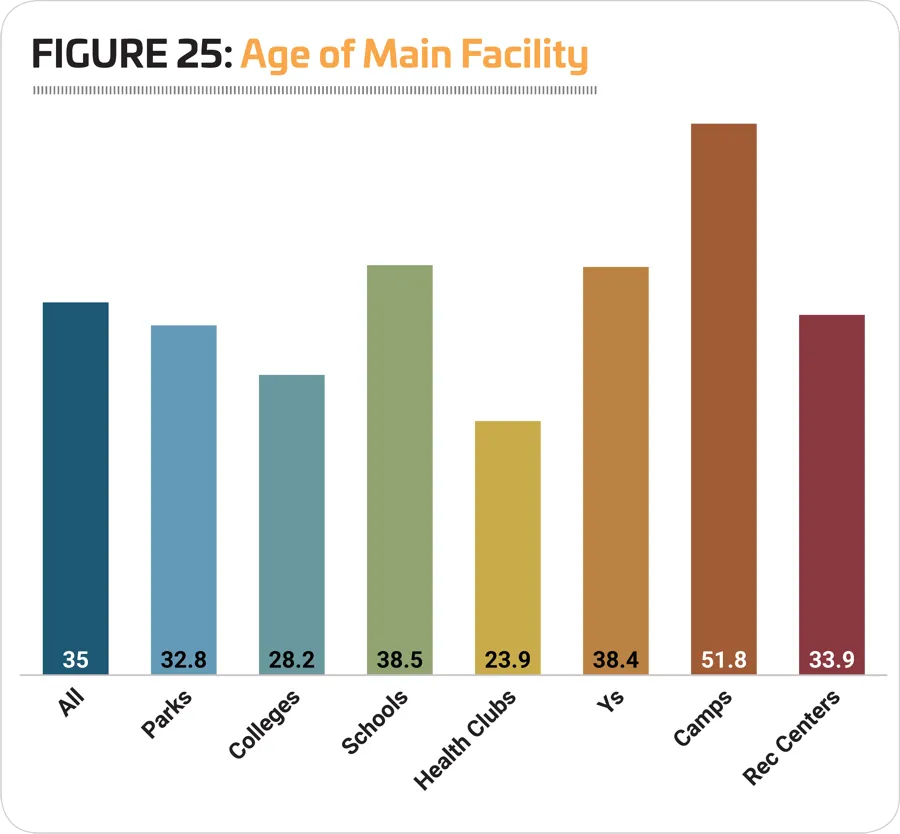

We've been asking survey participants how old their main facility is since 2013. In that time, facilities have aged from an average of 27.5 years in 2013. In 2020, respondents' facilities were, on average, 35 years old, up from 33.5 in 2019.

More than one-third (36%) of respondents said their facilities were 41 years or older, up from 33.2% in 2019. Nearly one-fifth (17.5%) of respondents have facilities that were at least 50 years old. Nearly one-quarter (24.2%) had facilities between 21 and 40 years old, while 20.8% said their facilities were between 11 and 20 years old. Just 14.6% of respondents had facilities that were 10 years old or less, with half of those having new facilities of 5 years or less.

As usual the newest facilities were found among health clubs and colleges. Respondents from health clubs have an average facility age of 23.9 years, while college facilities' average age is 28.2 years. They were followed by park facilities, at 32.8 years on average, and rec centers, with an average of 33.9 years. The oldest facilities were found among camps, where the average facility age is 51.8 years. (See Figure 25.)

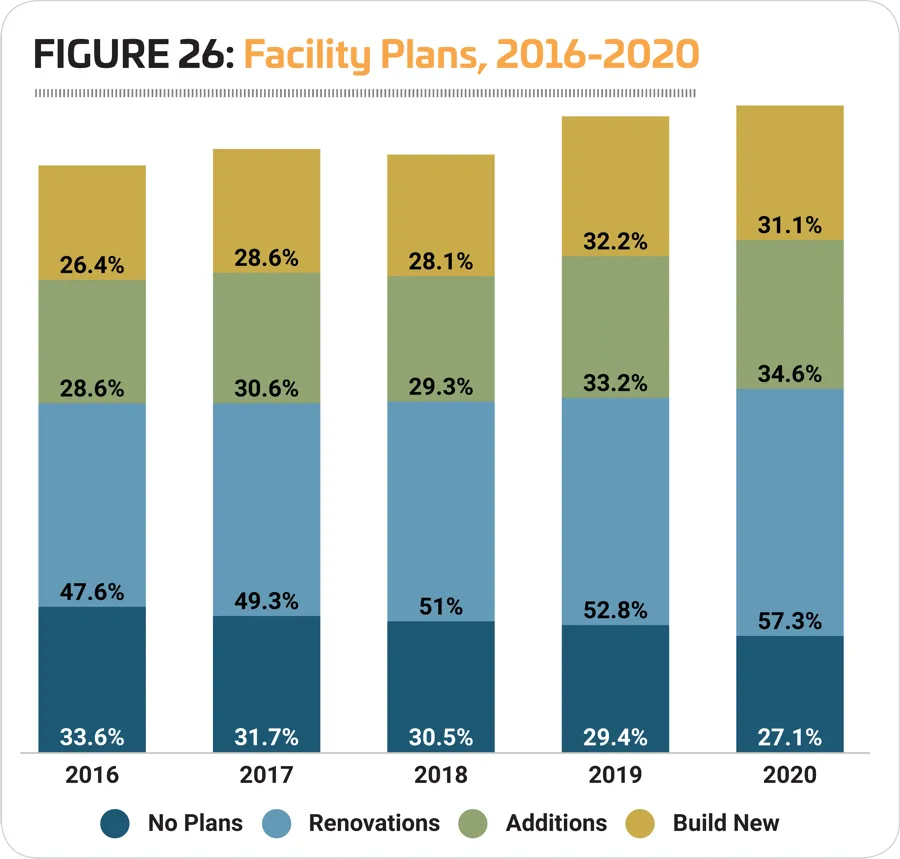

The percentage of respondents who are planning construction within the next several years has been climbing gradually, from a low of 62.7% in 2013 to 72.9% in 2020. However, the impact of COVID-19 on these construction plans is undoubtable. More than one-third (34.3%) of respondents to the Update Survey in May indicated that they were putting construction plans on hold as a result of the pandemic.

According to the original Industry Report survey, well over half (57.3%) of respondents said they were planning to renovate their existing facilities, up from 52.8% in 2019. Another 34.6% were planning to make additions to their facilities, and 31.1% were planning new construction. (See Figure 26.)

With the oldest facilities, on average, it comes as little surprise that camp respondents were the most likely to report that they had plans for construction. Some 85.3% of camp respondents said they were planning construction, up from 83.6% in 2019. They were followed by parks (80.8% of whom were planning construction), Ys (74.4%) and schools (69.3%). Respondents from colleges were the least likely to be planning construction, though more than half (52.4%) indicated they had such plans. They were followed by health clubs (59.5%) and rec centers (62.4%).

Camp respondents were the most likely to be planning either renovations or additions. Some 69.3% of camp respondents said they were planning renovations to their existing facilities, while 41.3% were planning additions.

Park respondents were the most likely to be planning new construction. Nearly four in 10 (38.7%) park respondents said they were planning to construct new facilities in the next three years.

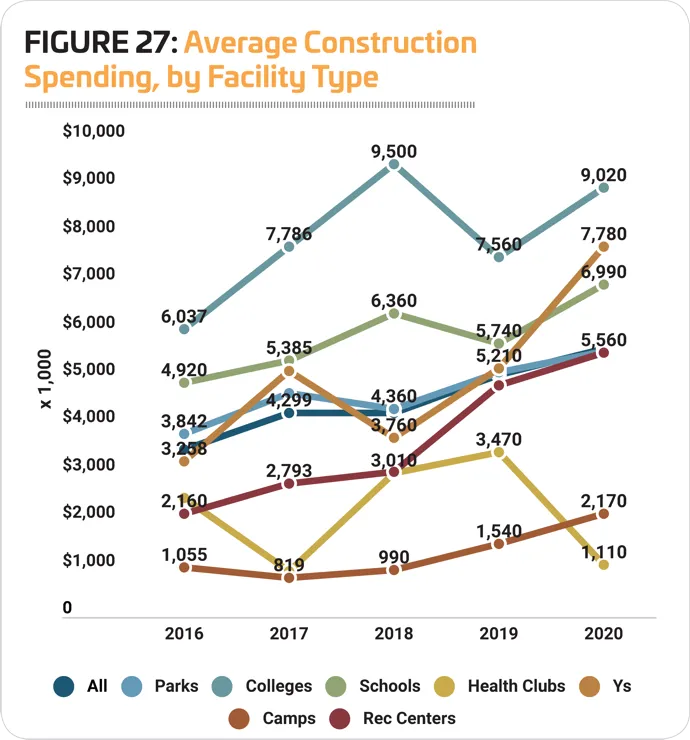

The average amount respondents were planning to spend on their construction plans was up 10.8% in 2020, after an 18.4% increase in 2019. On average, respondents to the 2020 survey were planning to spend $5,630,000 on their construction. (See Figure 27.)

From 2019 to 2020, the greatest increase to average construction budgets was reported by respondents from Ys and camps. Y respondents in 2020 were planning to spend $7,780,000, up 49.3% from 2019, and camps were planning to spend $2,170,000, up 40.9%. More modest increases were reported by schools (up 21.8% to $6,990,000), colleges (up 19.3% to $9,030,000), rec centers (up 14.6% to $5,560,000) and parks (up 8.6% to $5,570,000). Only health clubs reported that they'd be spending less on construction, with a decrease of 68% from the average in 2019, to $1,110,000.

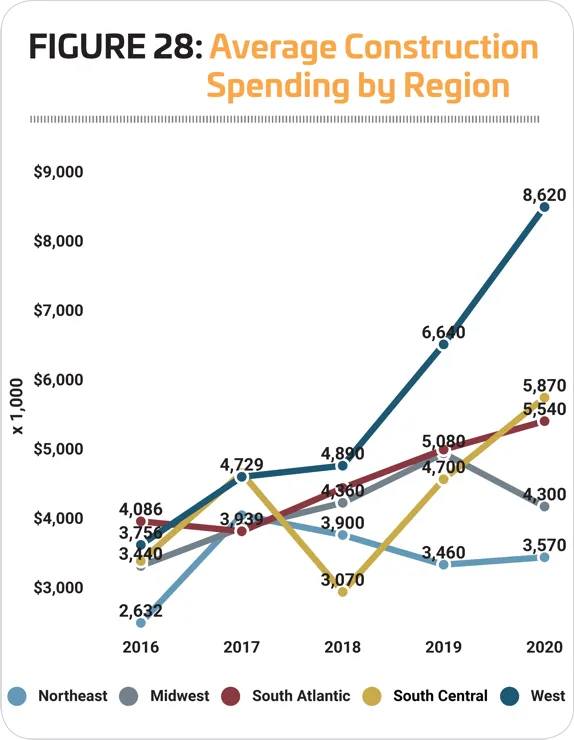

Respondents in the West and South Central regions reported the greatest overall increase from 2019 to 2020 to their average budgets for the construction they were planning. In the West, respondents' planned construction budgets grew 29.8%, to an average of $8,620,000, while in the South Central region, respondents' construction budgets increased by 24.9%, to an average of $5,870,000.

More modest increases were reported by respondents in the South Atlantic and Northeast. In the South Atlantic, respondents reported an 8.2% increase to construction budgets, to an average of $5,540,000, while Northeastern respondents saw a 3.2% increase to an average of $3,570,000.

Only Midwestern respondents reported a decrease to their average construction budget. Their planned construction spending fell 15.4%, to an average of $4,300,000. (See Figure 28.)

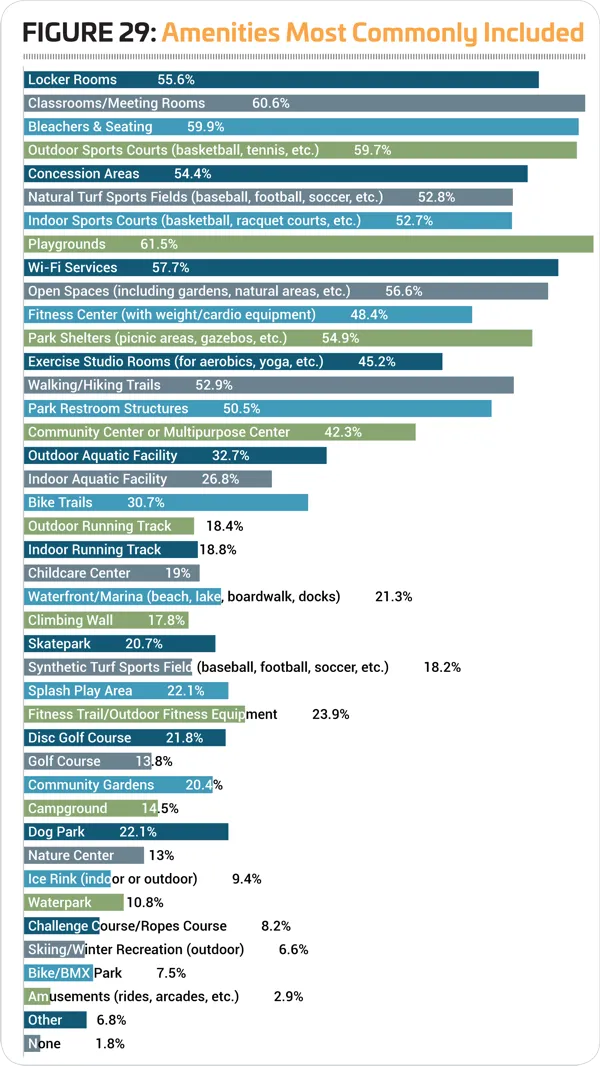

The top amenities included in respondents' facilities in 2020 include: playgrounds (61.5% of respondents include them in their facilities); classrooms and meeting rooms (60.6%); bleachers and seating (59.9%); outdoor sports courts for sports like basketball or tennis (59.7%); Wi-Fi (57.7%); open spaces such as natural areas and gardens (56.6%); locker rooms (55.6%); park shelters like gazebos (54.9%); concessions (54.4%); and walking and hiking trails (52.9%). (See Figure 29.)

As is generally the case, there was not a great deal of change in the percentage of respondents whose facilities include various sorts of amenities from 2019 to 2020. However, the following types of amenities saw an increase of two or more percentage points in the past year: open spaces (up 2.5); Wi-Fi services (up 2.4); walking and hiking trails (up 2.4); and outdoor sports courts (up 2.2).

Over the past five years, the following types of amenities have seen an increase of at least three percentage points: park restroom structures (up 8.4); dog parks (up 4.7); community centers (up 4); splash play areas (up 3.4); outdoor fitness areas (up 3.2); and indoor sports courts (up 3).

Respondents from parks were more likely than other respondents to include: park shelters (83.3% of park respondents had shelters); playgrounds (82.7%); park restroom structures (79%); open spaces (73.9%); outdoor sports courts (71.9%); bike trails (48.3%); outdoor aquatic facilities (42.1%); dog parks (40.4%); skateparks (39.9%); fitness trails and outdoor fitness equipment (34.5%); disc golf courses (33.7%); splash play areas (33.3%); community gardens (32.3%); golf courses (29.2%); bike and BMX parks (14.2%); and ice rinks (13.9%).

College respondents were more likely than others to include: indoor running/walking tracks (56.2%); and synthetic turf sports fields (42.1%).

Respondents from schools were more likely than others to include: locker rooms (88.8%); indoor sports courts (86.6%); bleachers and seating (85.8%); natural turf sports fields (80.6%); concessions (78.4%); and outdoor tracks (70.1%).

Respondents from health clubs were more likely than others to have fitness centers (89.2%).

Y respondents were more likely than others to include: Wi-Fi (84.9%); exercise studios (83.7%); classrooms and meeting rooms (81.4%); childcare areas (73.3%); indoor aquatic facilities (70.9%); and waterparks (17.4%).

Camp respondents were more likely than others to include: walking and hiking trails (78.4%); campgrounds (64.9%); waterfronts and marinas (51.4%); climbing walls (44.6%); challenge courses (40.5%); nature centers (27%); skiing and winter recreation areas (13.5%); and amusements (6.8%).

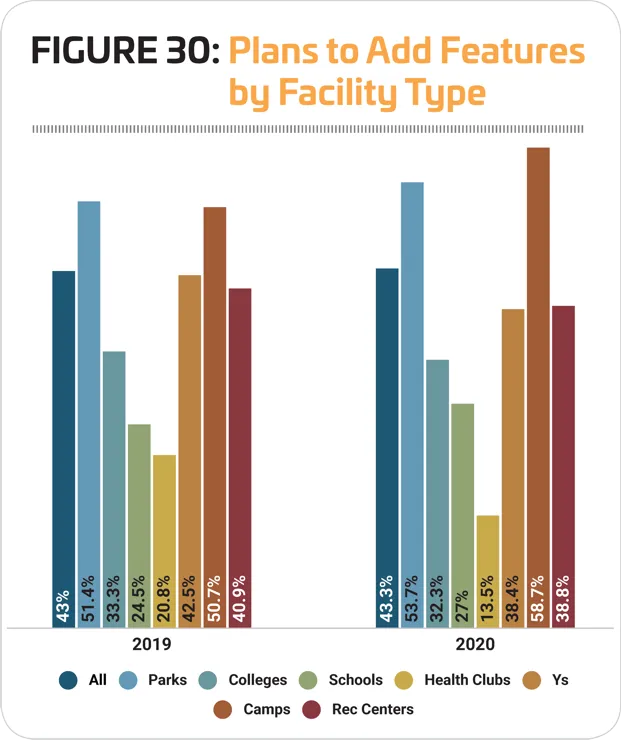

The number of respondents who said they had plans to add features at their facilities over the next several years has remained virtually unchanged for the past three years. In 2020, 43.3% of respondents said they had such plans, compared with 43% in 2019 and 43.1% in 2018. (See Figure 30.)

Respondents from camps and parks were again the most likely to report that they had plans to add features at their facilities. Nearly six in 10 (58.7%) camp respondents and 53.7% of park respondents said they were planning to add features at their facilities. They were followed by those from rec centers (38.8%), Ys (38.4%) and colleges (32.3%). Respondents from health clubs were the least likely to be planning to add features at their facilities, with 13.5% of these respondents indicating they had such plans.

The top 10 planned features for all facility types include:

- Splash play areas (25.4% of those with plans to add features were planning to add splash play)

- Playgrounds (20.3%)

- Park shelters (17.3%)

- Dog parks (17.1%)

- Park restrooms (16.1%)

- Synthetic turf sports fields (14.8%)

- Walking and hiking trails (14.8%)

- Fitness trails and outdoor fitness equipment (14.8%)

- Disc golf courses (12.9%)

- Outdoor sports courts (11.3%)

COVID-19 IMPACT: A Timeline for Reopening

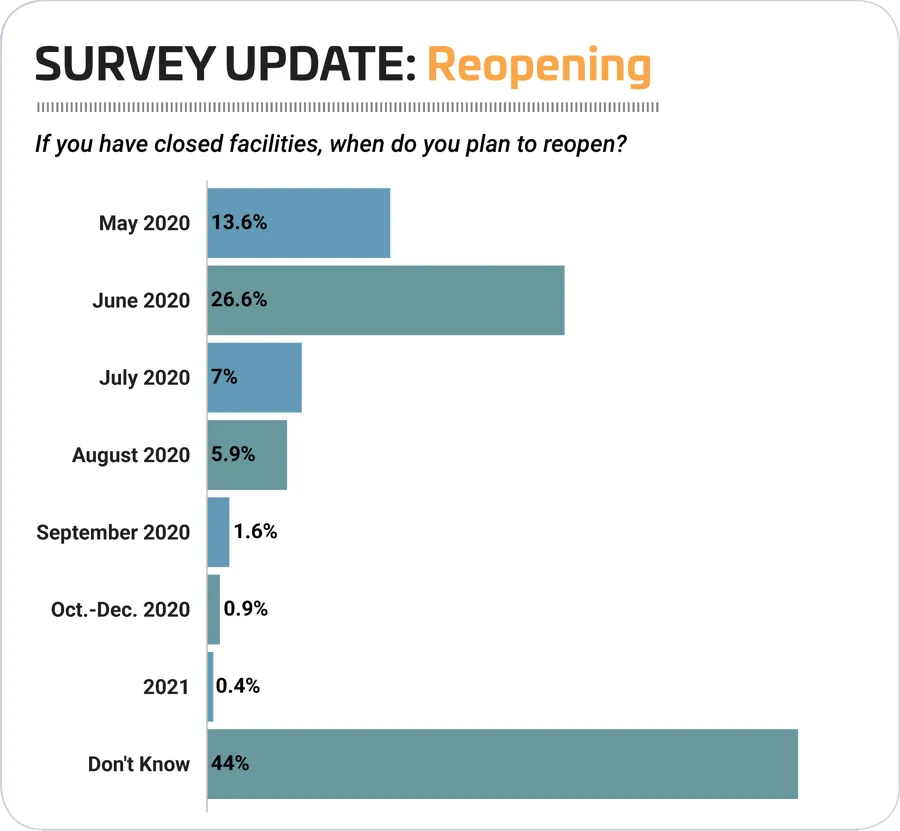

The majority of respondents to our COVID-19 Update Survey have closed all facilities temporarily (69.2%), or have temporarily closed (27.2%), or permanently closed (1.2%) facilities, due to directives aimed at slowing the spread of the virus. While some states began lifting stay-at-home orders as early as the end of April and beginning of May, nearly half (44%) of respondents to the COVID-19 Update Survey indicated that they were still not sure when their facilities would reopen. Another 40.2% said they would reopen in May or June 2020.

Here's what some of our respondents had to say about their timeline for opening:

"Facilities are closed until further notice with a tentative June opening. No programs once we reopen until the pandemic is over, with major modifications to our facility's availability to patrons, especially to enforce social distancing rules." (Parks & Recreation)

"We are a private athletic and social club of 125-plus years. We have been closed since mid-March. First time in history we have closed our doors like this. We are offering classes virtually for athletics, social, and food and beverage. We will reopen in phases, but a phase 1 opening date is undetermined at this time." (Health/Fitness/Sports Club)

"As a school district, our facilities and programs are closed. We are working hard to bring new programs to life virtually, but are having a hard time with the number of free programs offered during this time. We are hoping to get back to 'normal' programming for our fall season, but are awaiting a plan for reentry into our buildings." (School/School District)

"With our Community Center / Parks & Recreation Department closure, we have taken away a major social and recreational hub for all ages of our community. It is really hard to drive by our empty facility and playgrounds, knowing that we do not know when we get to reopen and be there to greet our members and staff. We really miss our connection with the community. We are trying to maintain this close connection through our Facebook site and a community support group, but the day-to-day interaction is severely missed." (Parks & Recreation)

Programming

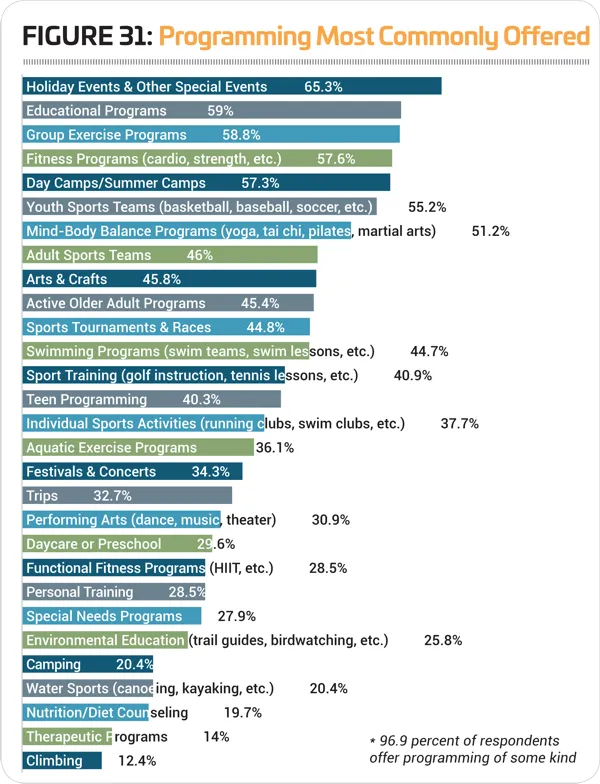

The top 10 most commonly offered programs include: holiday events and other special events (provided by 65.3% of respondents); educational programs (59%); group exercise programs (58.8%); fitness programs (57.6%); day camps and summer camps (57.3%); youth sports teams (55.2%); mind-body balance programs such as yoga and tai chi (51.2%); adult sports teams (46%); arts and crafts programs (45.8%); and programs for active older adults (45.4%). (See Figure 31.)

Most respondents—96.9%—said they offer programming of some kind. A full 100% of respondents from Ys and rec centers said they offer programming of some kind at their facilities. They were followed by parks (98.7%), health clubs (97.3%), schools (97.1%), colleges (96%) and camps (93.3%).

As is usually the case, Y respondents were the most likely to offer the most different sorts of programs. They were more likely than those from other types of facilities to offer: holidays and other special events; educational programs; day camps and summer camps; youth sports teams; mind-body balance programs like yoga; adult sports teams; arts and crafts; programs for active older adults; swimming programs; teen programming; individual sports activities like running or swim clubs; aquatic exercise programs; trips; performing arts; day care and preschool; special needs programs; and therapeutic programs.

Respondents from health clubs were more likely than others to indicate that they currently offer group exercise programs, fitness programs, functional fitness programs, personal training, and nutrition and diet counseling.

Park respondents were more likely than others to offer sport training like golf or tennis lessons, as well as festivals and concerts.

College respondents were more likely than others to offer water sports like kayaking and canoeing, and climbing programs.

Camps were more likely than others to provide environmental education programs and camping programs.

And finally, schools were more likely than others to host sports tournaments and races.

Some 35.1% of respondents in January 2020 said they were planning to add program offerings to their facilities over the next three years, up from 31.4% in 2019.

The 10 most commonly planned program additions were:

- Fitness programs (24% of those who have plans to add programs)

- Group exercise programs (22.4%)

- Teen programs (22%)

- Environmental education (21.8%)

- Day camps and summer camps (20.9%)

- Mind-body balance programs (20.5%)

- Programs for active older adults (18.1%)

- Special needs programs (17.9%)

- Holidays and other special events (17.4%)

- Arts and crafts (17%)

Respondents from rec centers were the most likely to report that they had plans to add programs at their facilities over the next few years. Nearly half (48.2%) of rec center respondents said they would be adding programs at their facilities. They were followed by parks (40.8%), Ys (39.5%), colleges (29.8%), health clubs (29.7%), and camps (25.3%). Schools were the least likely to be planning program additions, though 16.8% said they had plans for new programs at their facilities.

When asked about the various initiatives their organizations are involved in, respondents chose the following:

- Wellness initiatives (57.2%)

- Inclusion initiatives for those with physical disabilities (49.3%)

- Outreach to underserved populations (44.6%)

- Outreach to economically disadvantaged populations (44.1%)

- Inclusion initiatives for those with developmental disabilities (42.7%)

- Outreach to minority populations (39.3%)

- Initiatives to connect people with nature (33.6%)

- Resource conservation and green initiatives (32.9%)

- Initiatives to reduce hunger/improve nutrition (22%)

- Disaster recovery assistance (16.4%)

The greatest increases from 2019 were seen in: inclusion initiatives for those with physical disabilities (up 4.3 points); initiatives to reduce hunger and improve nutrition (up 3.3); disaster recovery assistance (up 3.2); outreach to minority populations (up 3.1); and outreach to economically disadvantaged populations (up 2.7).

Challenges, Then & Now

Typically, the top concern for most survey respondents is finding ways to do more with less—maximizing budgets to pay for their facilities, staff, programs and services.

This year, respondents in January said their top five concerns were: equipment and facility maintenance (58.4%, up from 55.8% in 2019); staffing issues (54.5%, up from 53.2%); marketing and increasing participation (40.1%, virtually unchanged from 40.4% in 2019); safety and risk management (34.4%, up from 31.9%); and creating new and innovative programming (29.3%, down from 32.2%).

Beyond these top five concerns, the areas of concern that saw the greatest increases were: environmental and conservation issues (up 2.2 points to 13.1%); and social equity and access issues (up 1.6 to 10%).

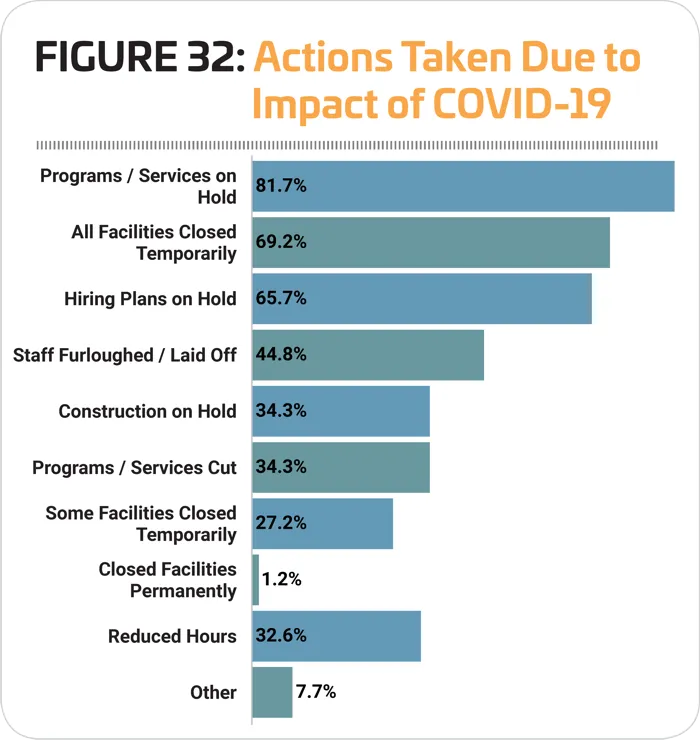

Of course, in light of the COVID-19 pandemic, a lot of respondents likely would answer differently today. In our Update Survey taken in early May, we asked respondents what actions they've taken due to the impact of COVID-19. The vast majority have closed facilities, whether that means temporarily closing all facilities (69.2%), temporarily closing some facilities (27.2%), or permanently closing facilities (1.2%). More than eight in 10 (81.7%) have put programs or services on hold, while 34.3% have cut programs or services entirely. Nearly two-thirds (65.7%) have put hiring plans on hold, while 44.8% have laid off or furloughed staff. More than one-third (34.3%) have put construction plans on hold. (See Figure 32.)

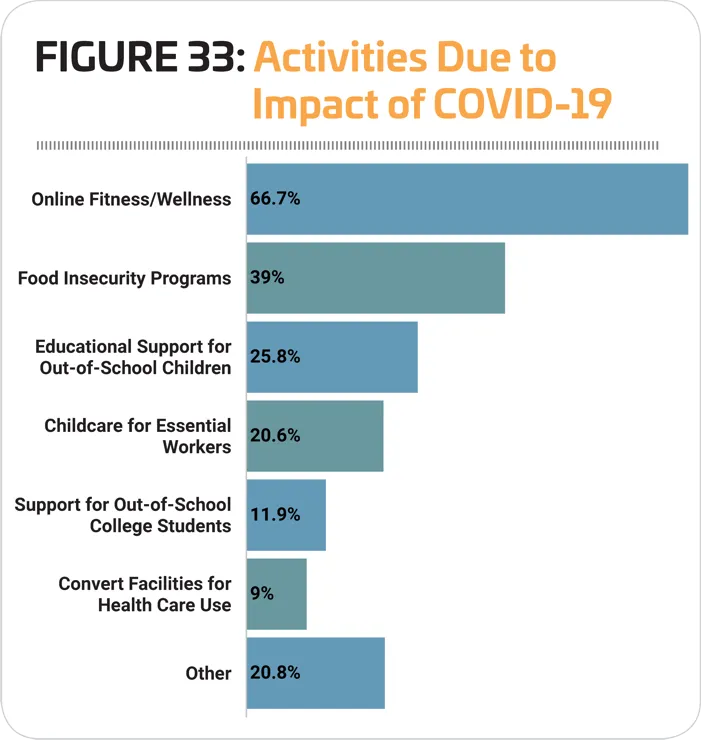

We also asked respondents to the Update Survey about the kinds of activities, programs and services they were involved in as a result of COVID-19. Two-thirds (66.7%) said they had added online fitness and wellness programming. Nearly four in 10 (39%) were involved in programs to address food insecurity. And more than one-quarter (25.8%) were involved in programs to provide educational support to out-of-school children. (See Figure 33.)

Finally, we asked respondents to summarize the impact COVID-19 is having on their facilities. Here's what some of them had to say:

"State system has informed the university that no new fee increases will be in place for FY20-21 which we had an increase scheduled for. Expected decline in enrollment due to this situation also impacts our bottom line along with lost revenue from programs and services offered, memberships and guest pass sales. The CV-19 situation has also taught us how to use technology for virtual programming compared to everything being in person, which is a big change for us." (College/University)

"Our department is losing revenue daily. We are not a nonprofit so this can be a crucial, pivotal point for parks and rec in our area. Tax collection is unknown as well, as many do not have answers. I am not sure how this will play out in the next few years." (Parks & Recreation)

"As a high school athletic director, we have had to cancel winter postseason events and all of spring sports season. Extremely disappointing and stressful for high school seniors. So many unknown variables still ahead and whether we can have summer activities and even fall sports." (School/School District)

"All our Campus Recreation facilities have been closed since mid-March. We are at a standstill to know about any summer programming or when we will open again and what that will look like. Even if we get the OK to open again, I am not sure how we will manage disinfecting and social distancing our areas." (College/University)

"Facility is only open to Emergency Child Care, Food Distribution and virtual fitness instructors. All other staff not furloughed are working from home. Call centers and virtual classes from home. Membership holds/cancellations are hovering around 60% of total base. Plans to reopen in the works for separate phases." (YMCA/YWCA/JCC/Boys & Girls Clubs)

"We have closed all of our recreation centers and park amenities such as basketball, tennis, pickleball, etc. The parks, trails and open spaces are still open for exercise and walking. We are encouraging park users to follow CDC guidelines regarding social distancing and encouraging residents to bring a trash bag so they will not leave a trace." (Parks & Recreation)

"Multiple employees are working from home, programs have been cancelled, at-home crafts and outdoor walking paths have been created for families to participate on their own, events have been rescheduled or cancelled, reopening plans for beaches have been discussed, sports programming has been reimagined." (Parks & Recreation)

"Since I'm a department of one for the town, I've been working from home and putting kits together for parents and senior citizens in town to help keep them busy! I've coordinated with local organizations to help those who can't leave their homes get groceries and food. I'm still doing the hiring process…sort of…for camp, but all plans for camp have been put on hold for the moment. Our town hall is not open to the public and our park and rec facility is closed until further notice. We are working with the Red Cross to facilitate a blood drive at our rec center if it is big enough." (Parks & Recreation)

"Maintenance backlog work is being accomplished. Maintenance crews are assigned to specifically disinfect facilities in use. Many personnel are able to work via computer at home. A shift in educational programs from physical on-site tours to web-based experiences that will accomplish our mission." (Parks & Recreation)

"We have closed our YMCA. We are still working as we are providing childcare for Essential workers in our area. Only full-time employees are working for our YMCA at the moment. We have been reaching members through Facebook Live videos, App challenges, Instagram challenges, online/virtual workouts. Leadership staff has had to step in and help out in childcare. We partnered with other like organizations in our area to create backpacks full of activities for the youth in our community. We are constantly trying to come up with plans on what reopening will look like." (YMCA)

"It has been a difficult time to try and operate for our organization. We are in a holding pattern now awaiting guidance from our elected officials on when we can resume and to what extent possible! My best wishes to you all." (Parks & Recreation) RM